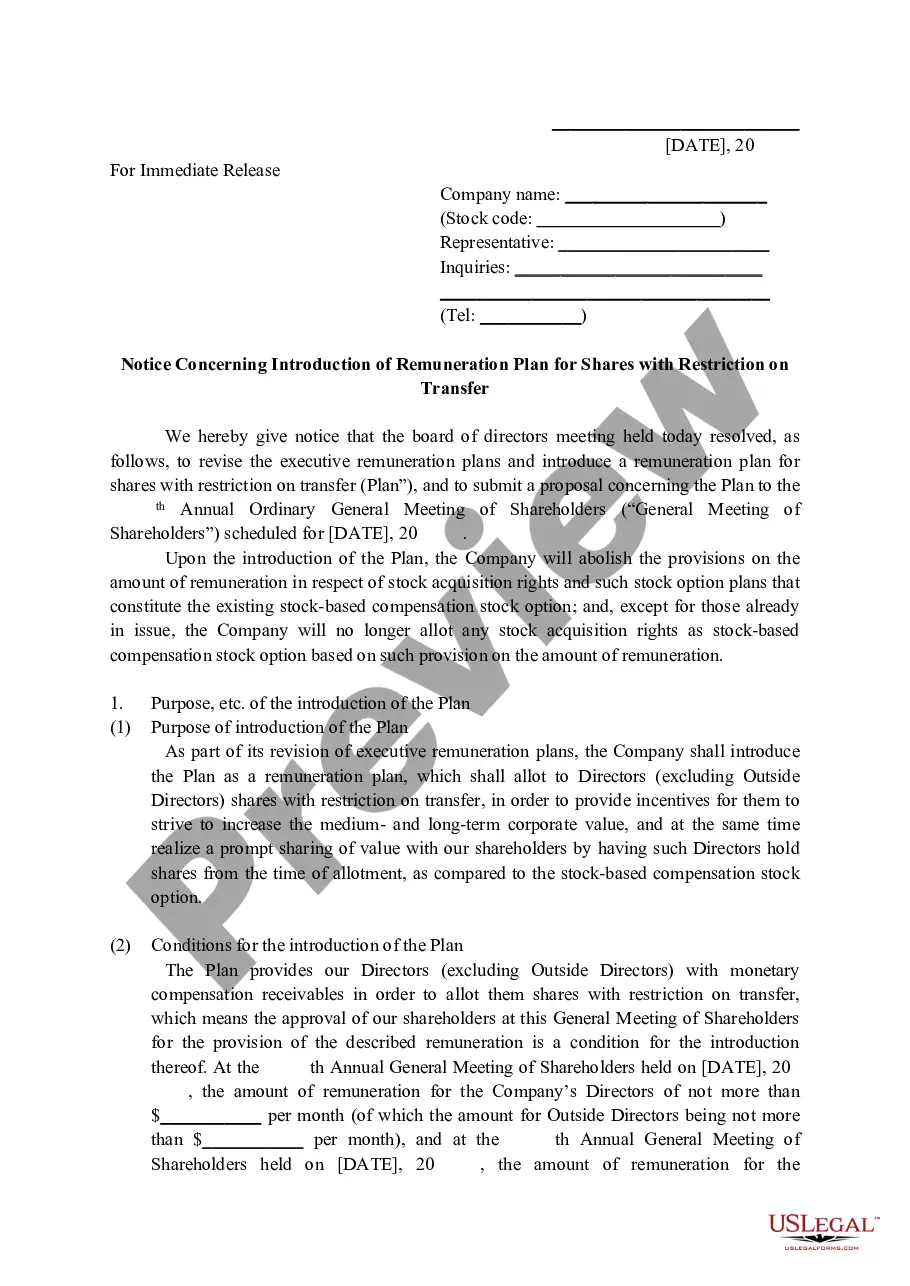

Tennessee Notice Regarding Introduction of Restricted Share-Based Remuneration Plan

Description

How to fill out Notice Regarding Introduction Of Restricted Share-Based Remuneration Plan?

Finding the right lawful papers format can be a struggle. Naturally, there are a variety of layouts available on the net, but how do you find the lawful type you will need? Utilize the US Legal Forms web site. The service offers 1000s of layouts, like the Tennessee Notice Regarding Introduction of Restricted Share-Based Remuneration Plan, which can be used for business and personal demands. Each of the forms are inspected by specialists and meet up with state and federal requirements.

If you are presently authorized, log in in your account and click on the Down load key to obtain the Tennessee Notice Regarding Introduction of Restricted Share-Based Remuneration Plan. Make use of account to search through the lawful forms you may have purchased formerly. Check out the My Forms tab of the account and get yet another backup from the papers you will need.

If you are a whole new consumer of US Legal Forms, listed here are basic instructions for you to follow:

- Very first, be sure you have selected the appropriate type for the town/region. You can look over the form while using Review key and read the form information to make sure this is basically the best for you.

- In case the type fails to meet up with your needs, take advantage of the Seach area to find the appropriate type.

- When you are positive that the form is proper, go through the Buy now key to obtain the type.

- Choose the prices program you need and type in the required info. Build your account and purchase the order with your PayPal account or credit card.

- Pick the submit formatting and down load the lawful papers format in your device.

- Full, modify and produce and indication the received Tennessee Notice Regarding Introduction of Restricted Share-Based Remuneration Plan.

US Legal Forms will be the largest library of lawful forms for which you will find various papers layouts. Utilize the company to down load professionally-produced files that follow condition requirements.

Form popularity

FAQ

T.C.A., Section 8-36-805 permits a retired TCRS member to accept temporary employment with an employer participating in TCRS without suspension of retirement benefits provided the retired member has been retired 60 days and does not accrue additional retirement credit as a result of such employment.

120-day Conversion to Hours Additionally, days can be converted to hours. If a retiree worked 7.5 hours pre-retirement and takes a position post-retirement working 4 hours per day, he can work a maximum of 900 hours ? the equivalent of 120 full days of work - during the 12-month temporary employment period.

Retired teachers and state employees who have been on the TCRS retired payroll for at least 12 consecutive months as of July 1, 2023 will receive a 3% cost-of-living adjustment, the highest increase available under laws governing TCRS.

Hybrid Plan members are immediately vested in the 401(k). Unlike the TCRS defined benefit plan, the amount available at retirement in a 401(k) account is the accumulated account balance that includes employer and member contributions and investment earnings.

After a five-year vesting period, an employee becomes eligible to receive a monthly benefit at retirement once the age requirement is met. The benefit is calculated by the employee's years of service and salary. The benefit provided by TCRS is a solid foundation for building a retirement future.

A: With low tax rates, affordable housing, a low cost of living, natural beauty, and so many fun things to do, Tennessee is a great place to consider retirement.

In this example, TCRS early retirement benefits replace 30% of the member's AFC after 25 years of service. A member with 25 years of service may retire prior to age 55; however, the benefit will be further reduced to the actuarial equivalent of the benefit payable at age 55.

On June 26, PBI confirmed to TCRS that files containing the personal information of 171,836 retired members and their beneficiaries was accessed as part of this breach. This information included name, social security number, date of birth, and mailing address.