Tennessee Designation of Successor Custodian by Donor Pursuant to the Uniform Transfers to Minors Act

Description

Form popularity

FAQ

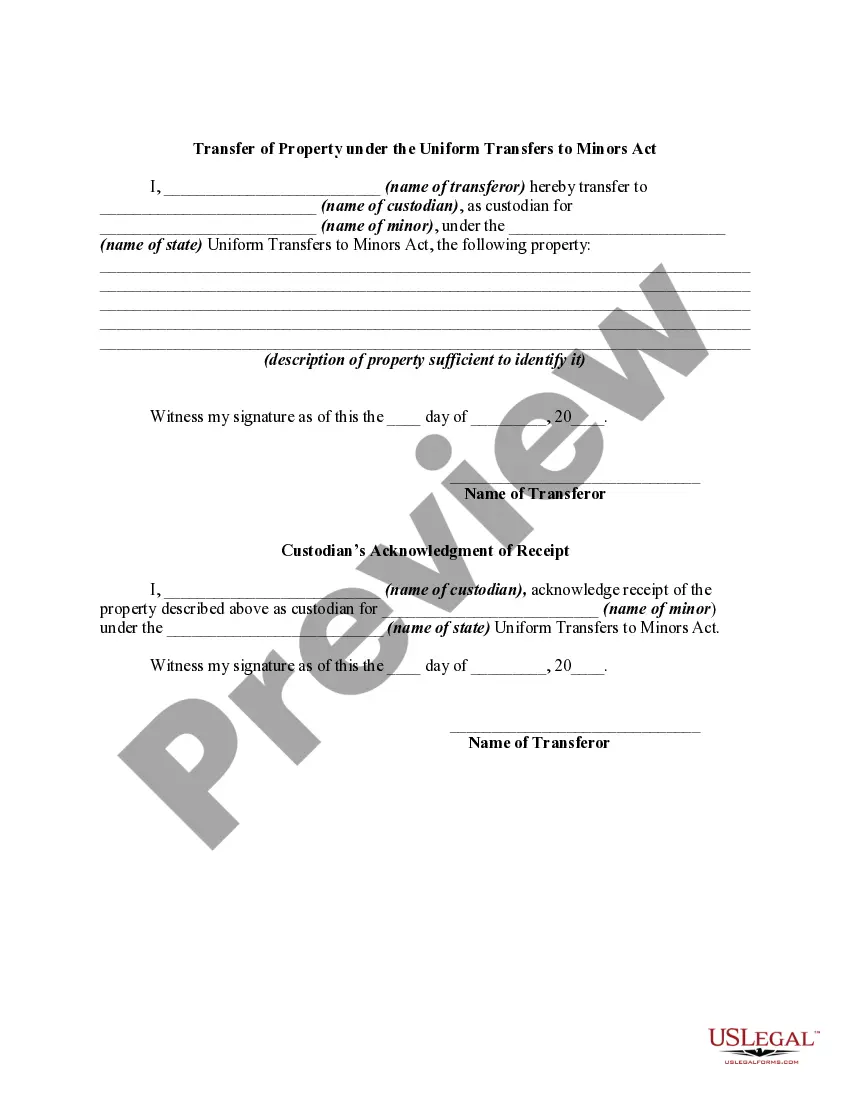

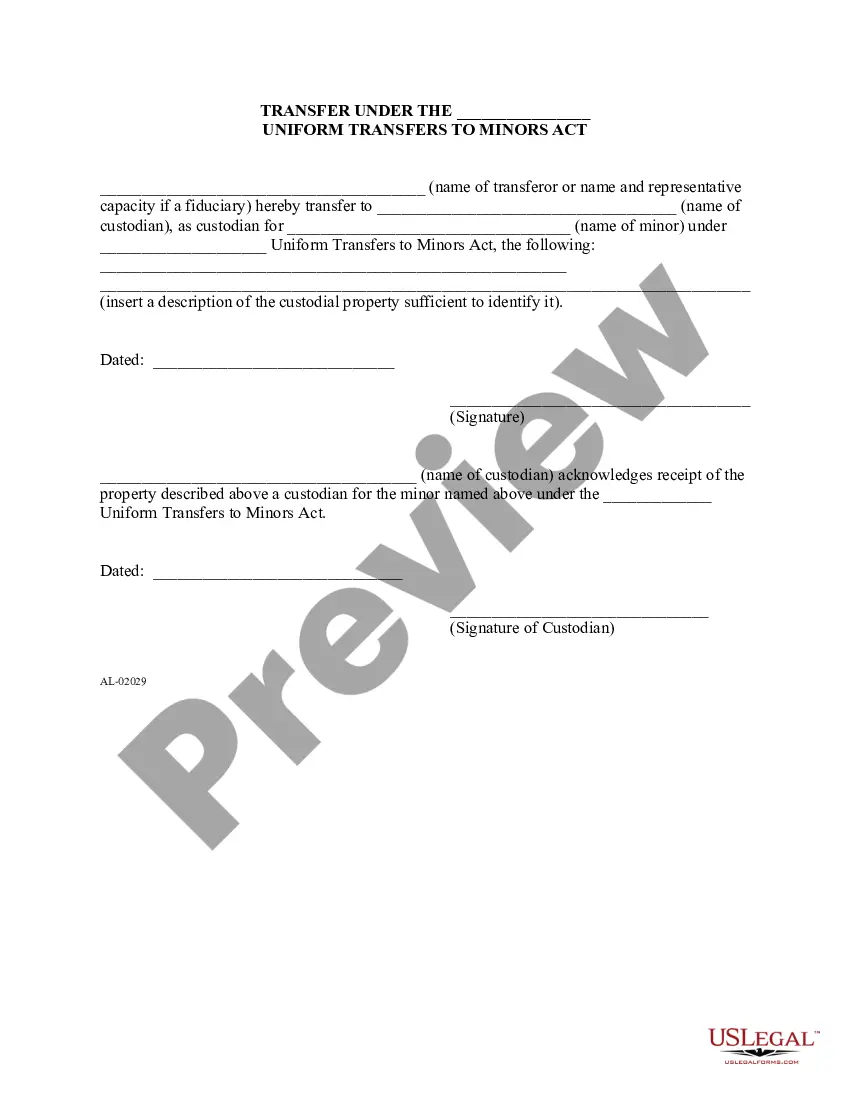

The UTMA allows the donor to name a custodian, who has the fiduciary duty to manage and invest the property on behalf of the minor until that minor becomes of legal age. The property belongs to the minor from the time the property is gifted.

Form used to designate a successor custodian for either an UGMA or UTMA account in the event that the original custodian resigns, dies, is incapacitated or is removed as custodian.

SUCCESSOR CUSTODIAN means upon the death of the Custodian the individual designated as the successor custodian on a signature card related to an IUTMA account.

Generally, the UTMA account transfers to the beneficiary when they become a legal adult, which is usually age 18 or 21, but it can be later. The age of adulthood may be defined differently for custodial accounts, like UTMAs or 529 plans, depending on your state.

If a donor acting as the custodian dies before the account terminates, the account value will be included in the donor's estate for estate tax purposes. If a minor dies before the age of majority, a custodial account is considered part of the minor's estate and is distributed ing to state law.

A custodian must open the account and manage the assets on behalf of the minor, but the assets in the account are the property of the minor. Custodians are typically parents, but technically can be anyone. Only one custodian and minor are allowed per custodial account.

Once the minor on a UGMA/UTMA account reaches the applicable state's age of termination, the custodian or the former minor may transfer the shares in the account(s) to the former minor's sole name. Instructions are acceptable from either the custodian or the former minor.

Form used to designate a successor custodian for either an UGMA or UTMA account in the event that the original custodian resigns, dies, is incapacitated or is removed as custodian.