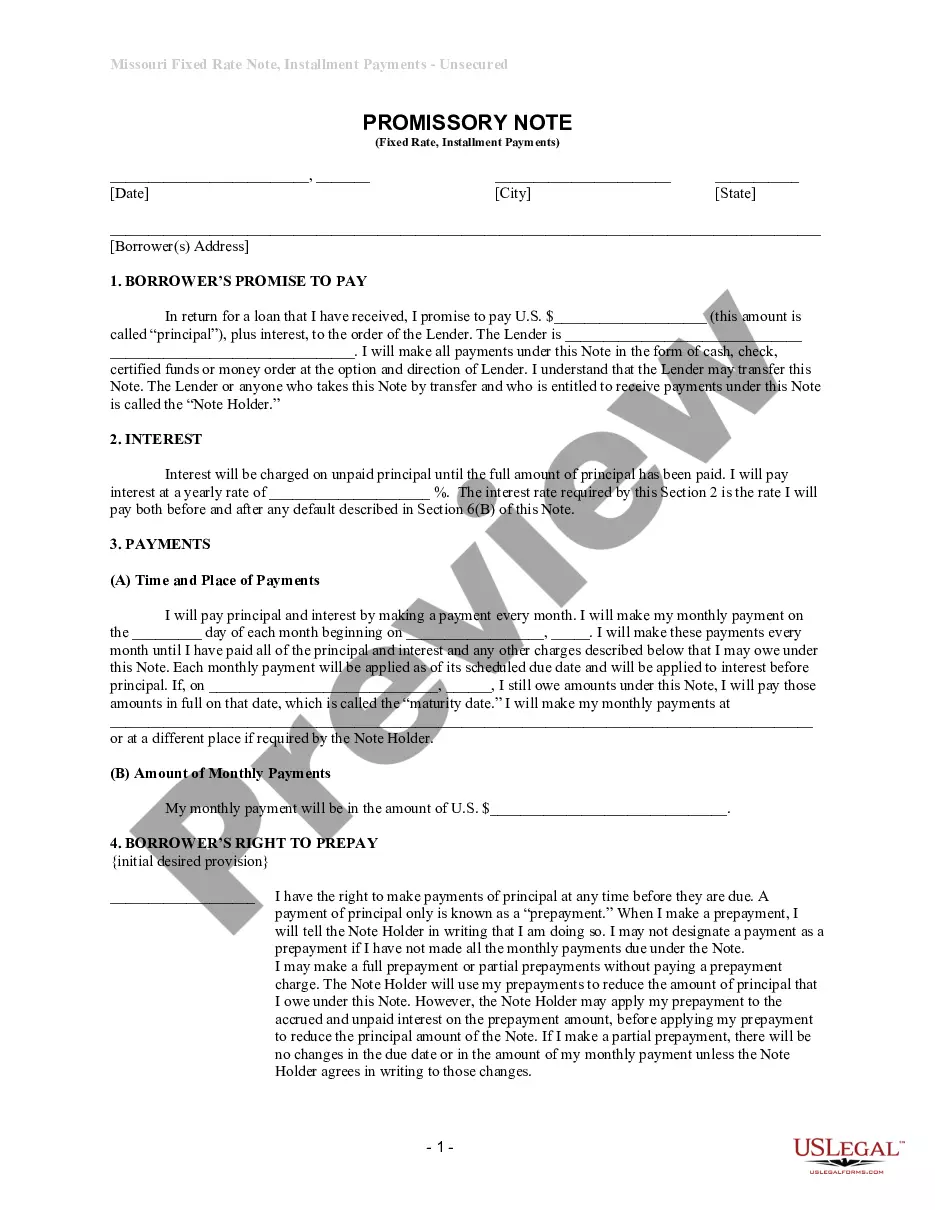

South Carolina Installments Fixed Rate Promissory Note Secured by Personal Property

About this form

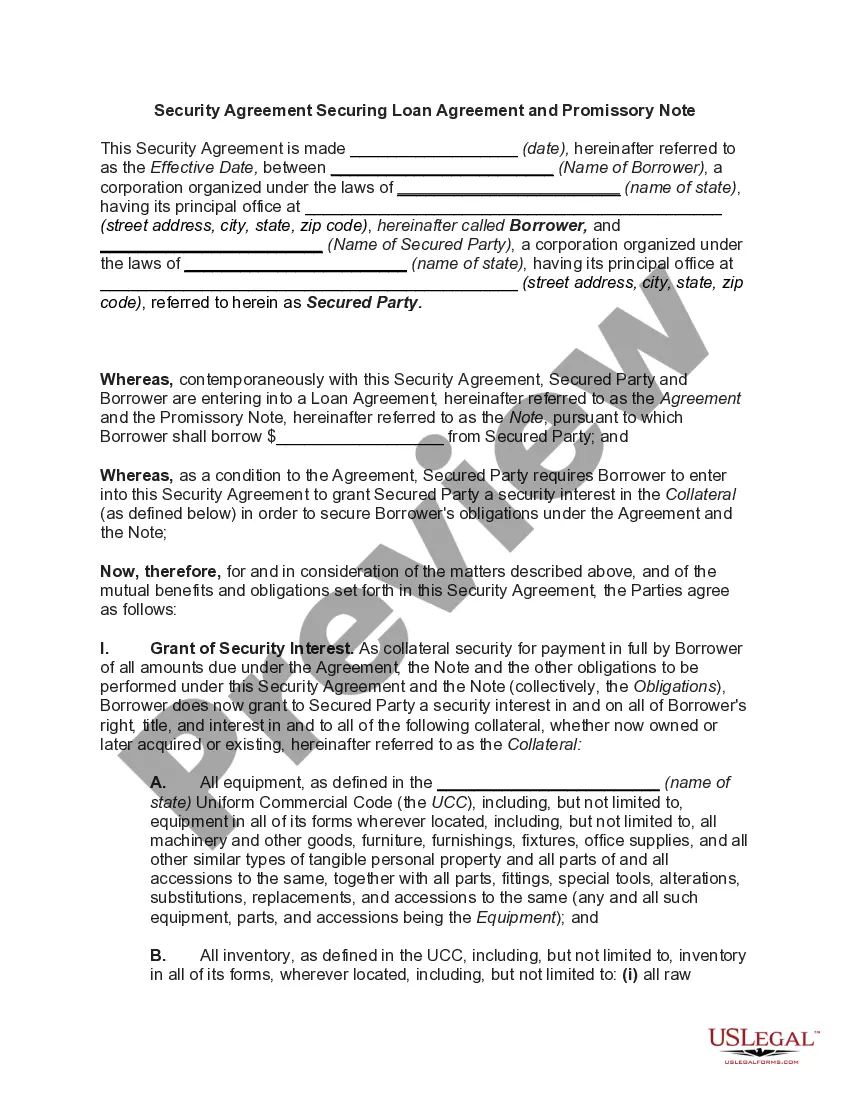

The South Carolina Installments Fixed Rate Promissory Note Secured by Personal Property is a legal document outlining a loan agreement where personal property is used as collateral. This promissory note specifies the terms of repayment, including the principal amount, interest rates, and repayment schedule. It is distinct from other loan documents because it requires a separate security agreement for the personal property securing the loan.

Main sections of this form

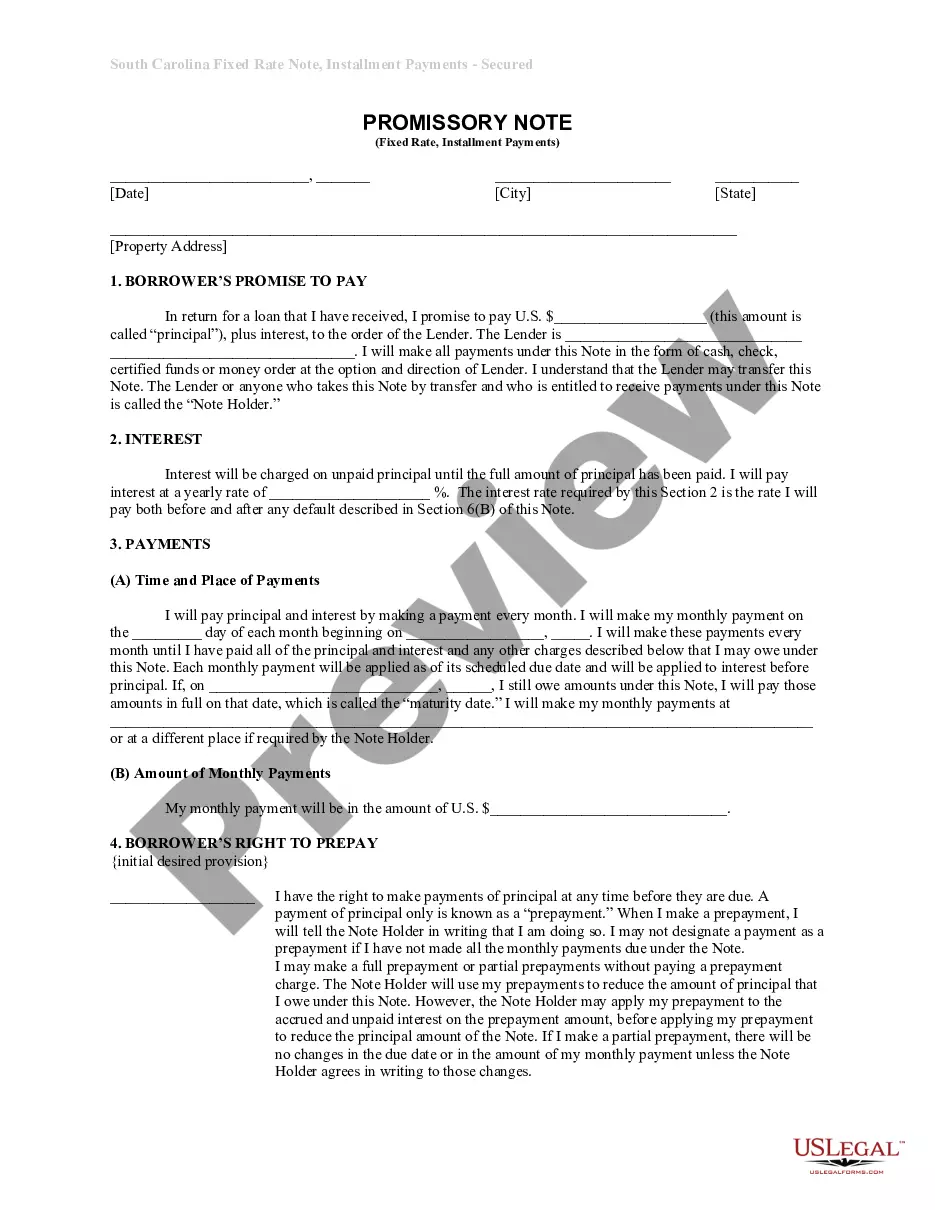

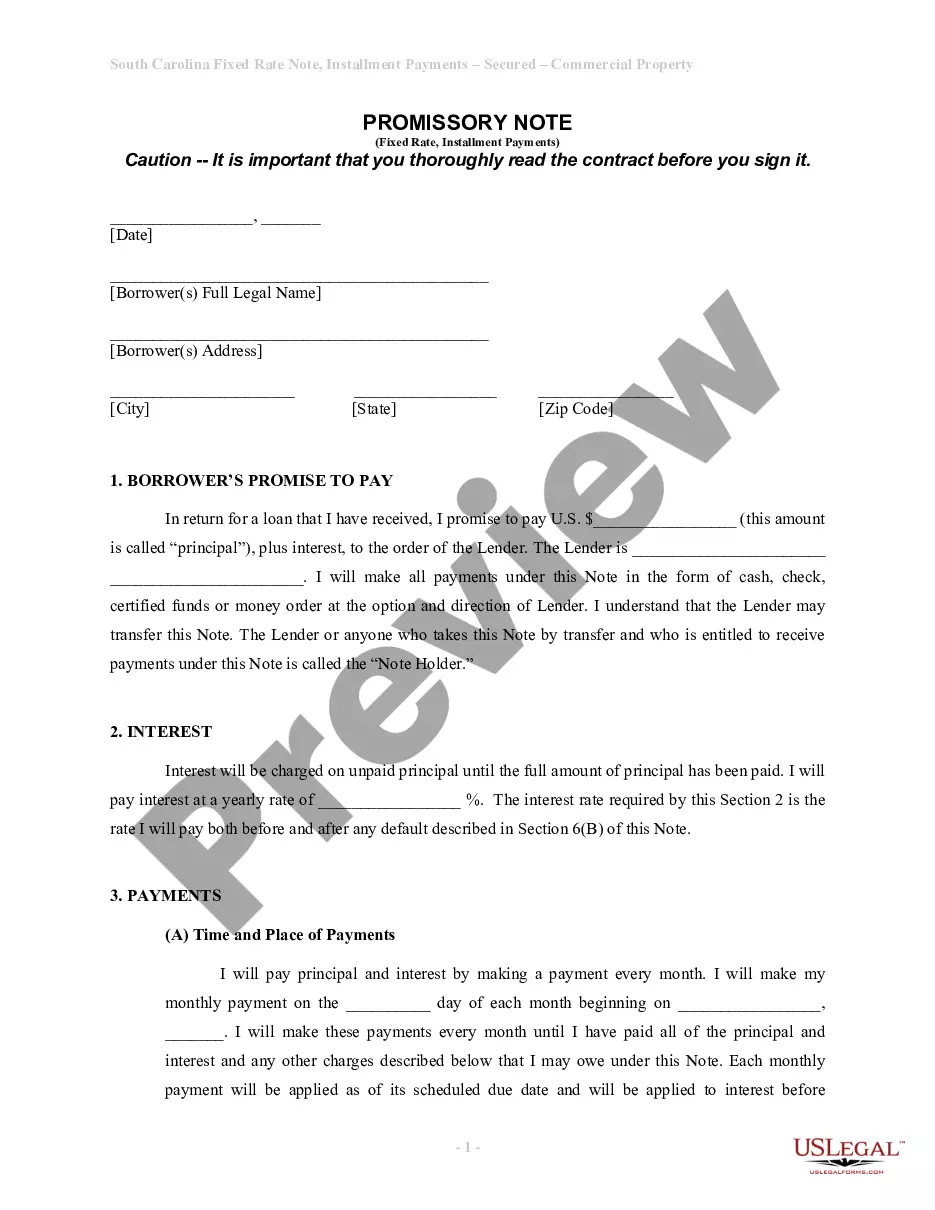

- Promise to Pay: Details the borrower's commitment to repay the lender the principal plus interest.

- Interest Rate: States the applicable annual interest rate on the unpaid principal.

- Payment Schedule: Outlines the frequency and due date of monthly payments.

- Prepayment Terms: Clarifies the borrower's right to make early payments and any associated penalties.

- Loan Charges: Addresses the management of any fees or charges related to the loan.

- Default Parameters: Defines what constitutes default and the lenderâs rights in such cases.

When to use this document

This form is ideal for individuals or businesses borrowing money with personal property as collateral. It is used when the borrower needs financial support and is willing to secure the loan with personal assets. Whether for buying a vehicle, home improvements, or consolidating debt, this promissory note is essential for formalizing the agreement.

Intended users of this form

- Individuals seeking to borrow funds using personal property as collateral.

- Small business owners who require a loan secured by assets.

- Entities needing a structured repayment plan for financial stability.

How to complete this form

- Identify the parties involved, including the borrower and lender.

- Specify the principal amount being borrowed.

- Enter the interest rate and payment schedule details.

- Provide the description of the personal property being used as collateral.

- Obtain the necessary signatures from all parties involved.

Notarization guidance

This form does not typically require notarization unless specified by local law. Always check to ensure compliance with state regulations before submitting.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes to avoid

- Failing to clearly describe the personal property used as collateral.

- Not specifying the interest rate correctly.

- Leaving out the payment schedule or due dates.

- Not obtaining all required signatures from parties involved.

Why complete this form online

- Convenience of accessing and downloading the form at any time.

- Ability to edit and customize the document to meet specific needs.

- Reliable templates drafted by licensed attorneys, ensuring legal compliance.

- Secure storage of your completed forms for future reference.

Quick recap

- The South Carolina Installments Fixed Rate Promissory Note is ideal for loans secured by personal property.

- Clearly outline the loan amount, interest rate, and monthly payment schedule to avoid disputes.

- The form helps both borrowers and lenders understand their rights and responsibilities, reducing potential issues.

Looking for another form?

Form popularity

FAQ

Promissory notes are ideal for individuals who do not qualify for traditional mortgages because they allow them to purchase a home by using the seller as the source of the loan and the purchased home as the source of the collateral.

Secured or unsecured? Generally, promissory notes are unsecured which means it is more like a formal IOU. However, lenders can request some security for the loan. For personal secured promissory notes, a house or car is often used as collateral.

You can use a template or create a promissory note online. But before you begin, you'll need to gather some information and make decisions about the way the loan will be structured. First, you'll need the names and addresses of both the lender (or "payee") and the borrower.

It includes land and buildings, for example. Personal property typically includes furniture, fixtures, tools, vehicles, and machinery and equipment. All of these items can be moved.

Examples of tangible personal property are your household goods and motor vehicles.Examples of intangible personal property are stocks, bonds, mutual funds, and securities. In addition, if a person owes you money, you may have a promissory note which describes the loan and amount of money the individual owes you.

These terms all mean the same thing. A mortgage is a loan secured by property that is used as collateral, which the lender can seize if the borrower defaults on the loan. The promissory note is exactly what it sounds like the borrower's written, signed promise to repay the loan.

Unlike a mortgage or deed of trust, the promissory note isn't recorded in the county land records. The lender holds the promissory note while the loan is outstanding. When the loan is paid off, the note is marked as "paid in full" and returned to the borrower.

Promissory notes are a valuable legal tool that any individual can use to legally bind another individual to an agreement for purchasing goods or borrowing money. A well-executed promissory note has the full effect of law behind it and is legally binding on both parties.

To secure a promissory note means that you identify some specific property and attach it to the note. Then, if the borrower defaults on the loan, you will be able to repossess the collateral as compensation for the loan.