Rhode Island Partial Assignment of Life Insurance Policy as Collateral

Description

How to fill out Partial Assignment Of Life Insurance Policy As Collateral?

Choosing the best legitimate document template can be quite a struggle. Naturally, there are a variety of themes available on the net, but how do you get the legitimate kind you need? Make use of the US Legal Forms website. The services delivers a large number of themes, for example the Rhode Island Partial Assignment of Life Insurance Policy as Collateral, which you can use for organization and personal requirements. All the types are inspected by professionals and fulfill state and federal specifications.

In case you are presently registered, log in for your accounts and click on the Obtain button to find the Rhode Island Partial Assignment of Life Insurance Policy as Collateral. Utilize your accounts to look through the legitimate types you might have purchased formerly. Go to the My Forms tab of your accounts and acquire yet another copy from the document you need.

In case you are a fresh customer of US Legal Forms, listed here are simple instructions that you should comply with:

- Initially, be sure you have chosen the right kind to your town/county. You can look over the shape while using Preview button and browse the shape description to make sure it will be the right one for you.

- If the kind will not fulfill your requirements, make use of the Seach field to get the right kind.

- When you are sure that the shape is suitable, click the Acquire now button to find the kind.

- Choose the rates prepare you desire and enter the essential information. Build your accounts and buy the order with your PayPal accounts or bank card.

- Choose the data file formatting and download the legitimate document template for your system.

- Total, revise and print and indication the acquired Rhode Island Partial Assignment of Life Insurance Policy as Collateral.

US Legal Forms may be the largest catalogue of legitimate types where you will find different document themes. Make use of the service to download expertly-manufactured documents that comply with state specifications.

Form popularity

FAQ

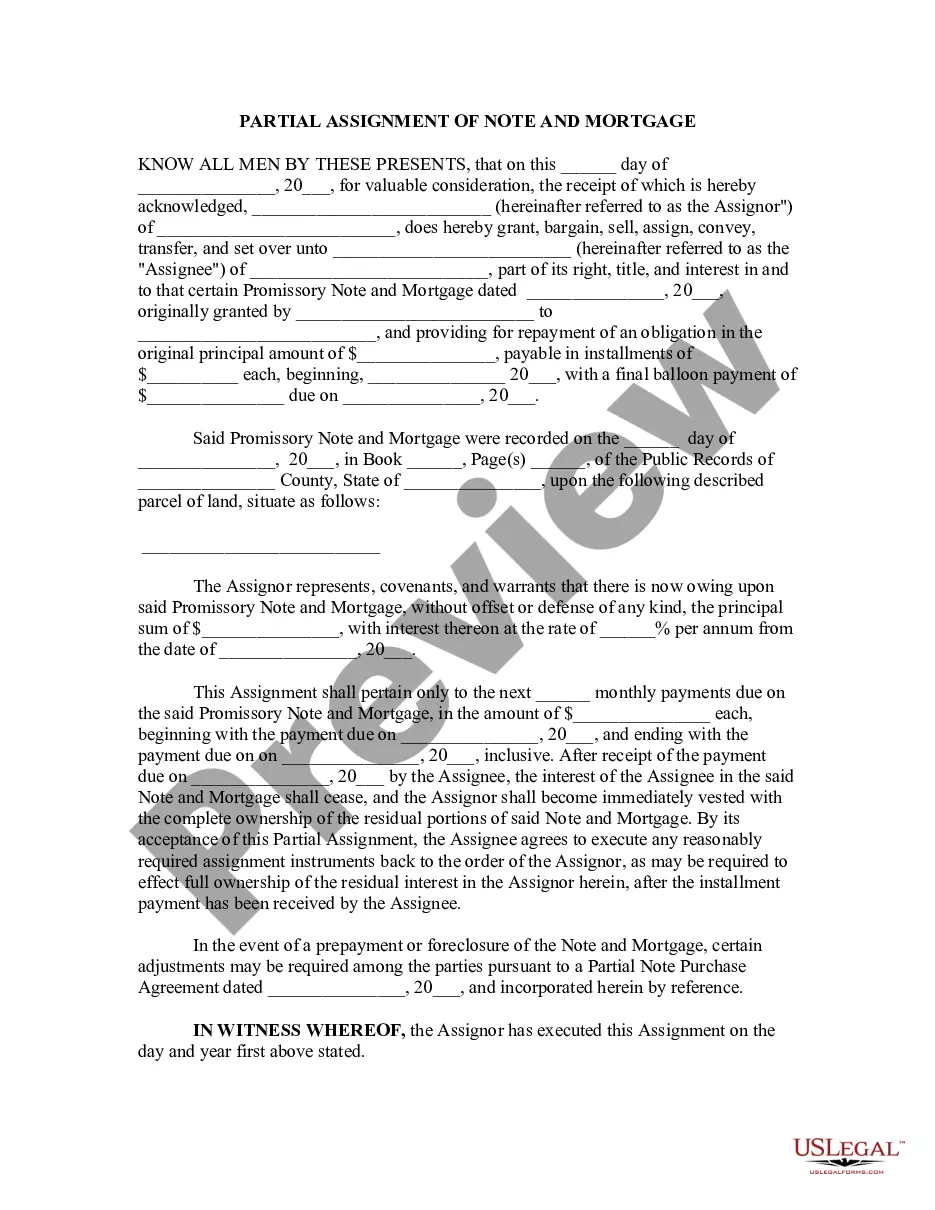

Collateral assignment of life insurance is a method of providing a lender with collateral when you apply for a loan. In this case, the collateral is your life insurance policy's face value, which could be used to pay back the amount you owe in case you die while in debt.

A life insurance policy can be assigned when rights of one person are transferred to another. The rights to your insurance policy can be transferred to someone else for various reasons. The process is known as assignment.

Which of these actions is taken when a policyowner uses a Life Insurance policy as collateral for a bank loan? Collateral assignment" A policyowner using the Life Insurance policy as collateral for a bank loan normally would make a collateral assignment.

A collateral assignment pledges a permanent life insurance policy's cash value and death benefits to another party and is most commonly used to secure a loan taken out by the policyowner. A collateral assignment primarily serves to protect the repayment interest of the lender.

If you have a life insurance policy, you're in luck, because most businesses typically accept life insurance as collateral as they can guarantee funds if the borrower dies or defaults.

A collateral assignment of life insurance is a conditional assignment appointing a lender as an assignee of a policy. Essentially, the lender has a claim to some or all of the death benefit until the loan is repaid. The death benefit is used as collateral for a loan.

Collateral assignment, on the other hand, is a temporary and often revocable arrangement. The policyholder retains ownership and control over the policy but agrees that the lender has a claim to a part of the death benefit if the loan is not repaid.

Under partial assignment, only the designated amount is paid to the assignee. Rest of the proceeds are paid to the nominee. If your expected insurance proceeds are more than the loan amount, you should opt for partial assignment.