Puerto Rico Approval for Relocation Expenses and Allowances

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Approval For Relocation Expenses And Allowances?

It is feasible to dedicate time online searching for the legitimate document template that meets the federal and state requirements you need.

US Legal Forms offers numerous legal forms that have been vetted by professionals.

You can conveniently download or print the Puerto Rico Approval for Relocation Expenses and Allowances from my service.

First, ensure you have selected the right document template for your chosen county/city. Review the form description to confirm you have selected the correct form. If available, use the Review button to browse through the document template as well.

- If you already have a US Legal Forms account, you can sign in and then click the Download button.

- After that, you can complete, modify, print, or sign the Puerto Rico Approval for Relocation Expenses and Allowances.

- Every legal document template you obtain is your property forever.

- To acquire an additional copy of any purchased form, visit the My documents tab and click the appropriate button.

- If you are using the US Legal Forms website for the first time, follow the simple instructions below.

Form popularity

FAQ

In order to achieve tax savings under Act #20 and Act #22, the new residents of Puerto Rico must comply with complex Puerto Rico and Federal tax rules that apply to determine (i) whether they are bona fide residents of Puerto Rico under the Federal Internal Revenue Code; and (ii) whether they can derive income that is

Further, Resident Individuals must apply for and obtain a tax exemption decree under Act 60. To obtain access to the approved and signed tax exemption decree, a one-time fee of $5,000 must be satisfied and deposited into a special fund to promote the relocation of Resident Individuals to Puerto Rico.

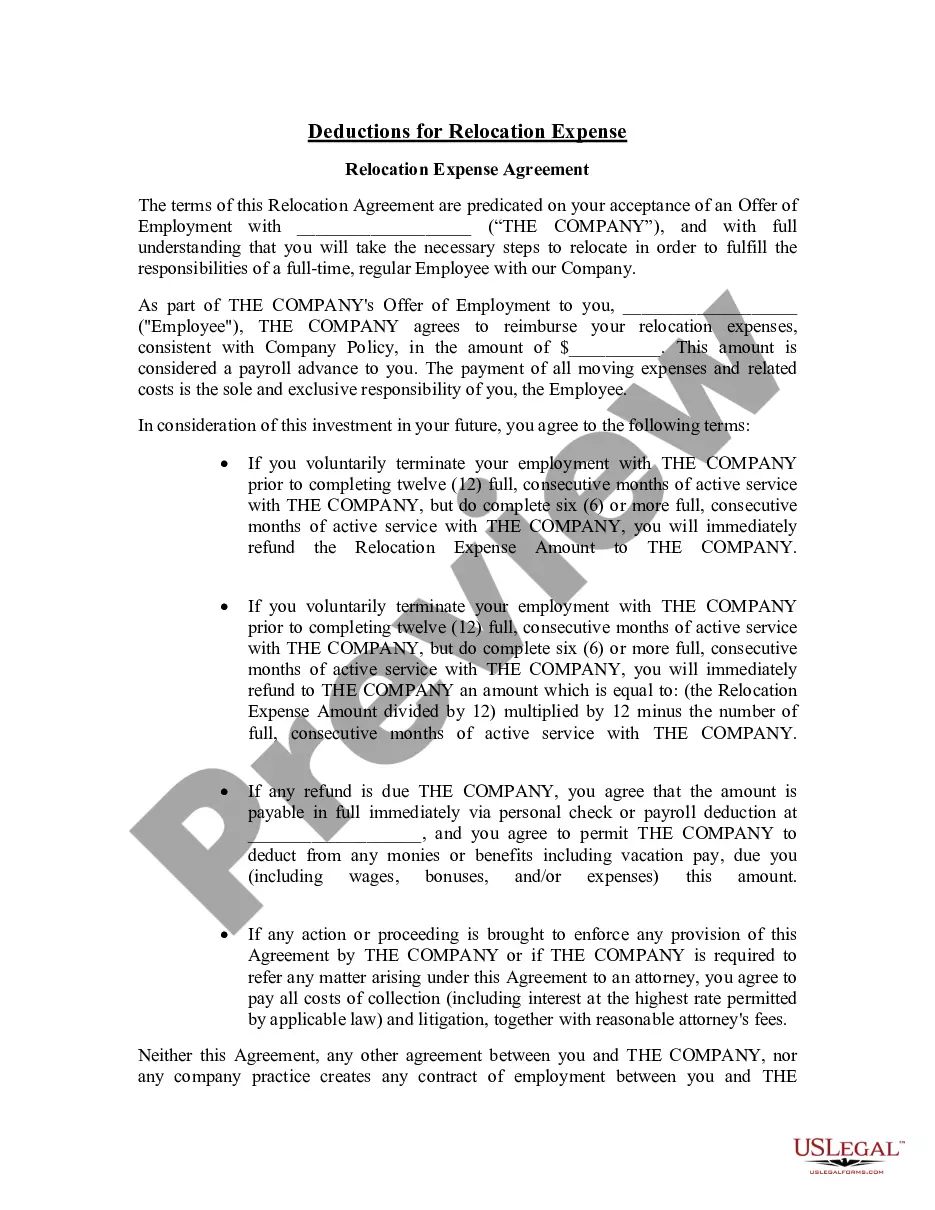

The RITA reimburses an eligible transferred employee substantially all of the additional Federal, State, and local income taxes incurred as a result of receiving taxable travel income. Travel W-2 wages/income and withholdings are reported to the IRS.

To get started, you can hire an attorney to file the paperwork for Act 22, or, you can file yourself through Puerto Rico's Single Business Portal.

To establish residence under the Act, someone must create a presumptive residence in Puerto Rico, live there for at least 183 days of the year, and cannot have a home outside Puerto Rico.

Specifically, a U.S. citizen who becomes a bona fide Puerto Rico resident and moves his or her business to Puerto Rico (thus, generating Puerto Rico sourced income) may benefit from a 4% corporate tax/fixed income tax rate, a 100% exemption on property taxes, and a 100% exemption on dividends from export services.

Further, Resident Individuals must apply for and obtain a tax exemption decree under Act 60. To obtain access to the approved and signed tax exemption decree, a one-time fee of $5,000 must be satisfied and deposited into a special fund to promote the relocation of Resident Individuals to Puerto Rico.

Relocation expenses for employees paid by an employer (aside from BVO/GBO homesale programs) are all considered taxable income to the employee by the IRS and state authorities (and by local governments that levy an income tax).

Physical Presence: the investor has to be physically present in Puerto Rico 168-183 days per year, and in the United States for less than 90 days in the year.The restrictions may have been modified to require only that the investor have spent more time in Puerto Rico than any other single place in the world.More items...

Multiplying the Combined Marginal Tax Rate (CMTR) (using the state and local tax tables most current at the time of the RITA calculation) by the total of all covered taxable relocation benefits during the applicable Year 1, and then subtracting your WTA(s), if any, from the same Year 1 from that total. That is: