Pennsylvania General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion

Description

How to fill out General Form Of Trust Agreement For Minor Qualifying For Annual Gift Tax Exclusion?

Selecting the optimal authorized document format can be a challenge. Certainly, there are numerous templates accessible online, but how can you find the legal form you require? Utilize the US Legal Forms website. The platform offers countless templates, including the Pennsylvania General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion, which you can utilize for both business and personal purposes. All forms are vetted by professionals and comply with federal and state regulations.

If you are already a member, sign in to your account and click on the Download button to locate the Pennsylvania General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion. Utilize your account to view the legal forms you may have purchased in the past. Navigate to the My documents section of your account to obtain another copy of the document you need.

For new users of US Legal Forms, here are straightforward instructions for you to follow: First, ensure you have selected the appropriate form for your city/county. You can preview the form using the Review button and read the form description to confirm it is the correct one for you. If the form does not meet your needs, use the Search field to find the right form. Once you are certain the form is appropriate, click the Purchase now button to acquire the form. Select the pricing plan you prefer and enter the necessary information. Create your account and complete your order using your PayPal account or credit card. Choose the document format and download the authorized document type to your device. Complete, modify, print, and sign the acquired Pennsylvania General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion.

- US Legal Forms is the largest repository of legal forms where you can find various document templates.

- Use the service to download professionally crafted paperwork that adhere to state requirements.

- The platform provides an extensive range of forms for different legal needs.

- Forms are regularly updated to ensure compliance with the latest regulations.

- Efficiently manage your documents through your US Legal Forms account.

Form popularity

FAQ

The Tax Court held that the withdrawal rights provided in a trust declaration were not illusory and that therefore a married couple's gifts to the trust were gifts of present interests in property that qualified for the annual exclusion.

The Annual Gift Exclusion Amount Can Be Saved Every Year in a Crummey Trust. You can use your annual exclusion amount, and provide guidance and instruction on how the funds will be used to benefit members of your family. An annual exclusion trust, also known as a crummey trust, is one way to do this.

The Annual Exclusion amount is the amount of money that one person may transfer to another as a gift without incurring a gift tax or affecting the unified credit. This annual gift exclusion can be transferred in the form of cash or other assets.

The good news regarding trusts and taxation is that gifts and inheritances are not considered income for income tax purposes. This means that gifts to trusts and distributions of principal from trusts to beneficiaries are not subject to income tax.

The IRS does not levy gift taxes on trusts, nor does it consider payments from the trust to a beneficiary as a gift (it may be taxable income to the beneficiary, however).

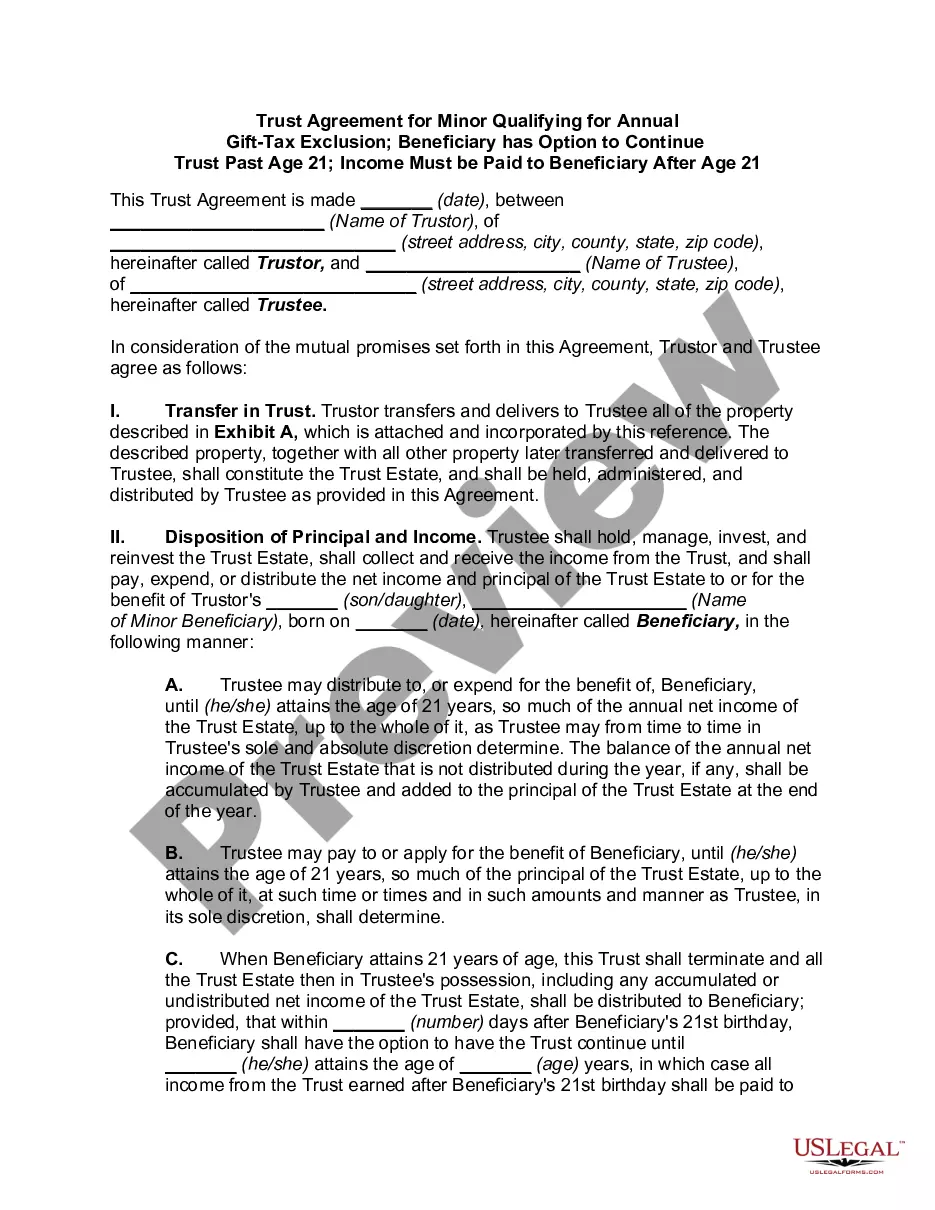

The key difference between a 2503(c) trust and a 2503(b) trust is the distribution requirement. Parents who are concerned about providing a child or other beneficiary with access to trust funds at age 21 might be better off with a 2503(b), since there is no requirement for access at age 21.

Gifts in trust do not qualify for the annual exclusion unless the trust either qualifies as a Minor's Trust under Internal Revenue Code Section 2503(c) or has certain temporary withdrawal powers called Crummey powers.

The $15,000 annual exclusion means you can give $15,000 to as many people as you want. So you can give each of your five grandchildren $15,000 apiece in a given year, for a total of $135,000. Any gifts you make to a single person over $15,000 count toward your combined estate and gift tax exclusion.

A Section 2503(c) trust allows all the principal and income to be used for the child until he reaches the age of 21, unlike the 2503(b) trust that extends beyond age 21 and requires income to be paid to the child annually. The trustee can pay the child's college expenses from the 2503(c) trust.

A gift in trust is a way to avoid taxes on gifts that exceed the annual gift tax exclusion amount. One type of gift in trust is a Crummey trust, which allows gifts to be given for a specific period, establishing the gifts as a present interest and eligible for the gift tax exclusion.