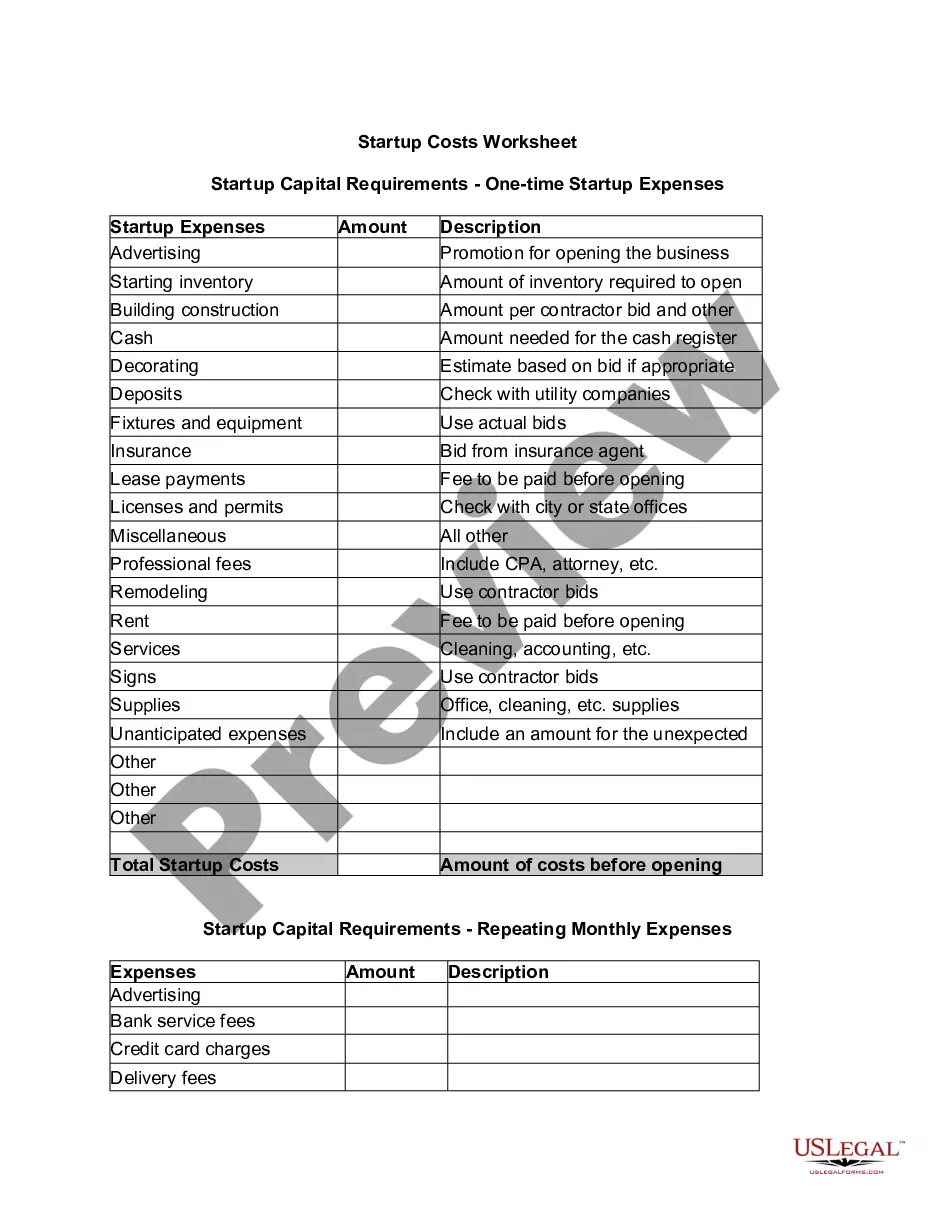

Pennsylvania Startup Costs Worksheet

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Startup Costs Worksheet?

Are you currently in a position where you frequently require documents for both business or personal purposes almost every day.

There are numerous legal document templates available online, but finding reliable ones isn't easy.

US Legal Forms offers thousands of form templates, such as the Pennsylvania Startup Costs Worksheet, which are designed to meet federal and state regulations.

Once you find the appropriate form, click on Buy now.

Choose the pricing plan you prefer, fill in the required details to create your account, and pay for your order using PayPal or credit card. Select a convenient document format and download your copy. You can find all the document templates you have purchased in the My documents menu. You can obtain an additional copy of the Pennsylvania Startup Costs Worksheet at any time if necessary. Just click the needed form to download or print the document template. Use US Legal Forms, the most extensive collection of legal forms, to save time and avoid mistakes. The service provides professionally created legal document templates that can be used for a variety of purposes. Create an account on US Legal Forms and start making your life easier.

- If you are already acquainted with the US Legal Forms website and have an account, simply Log In.

- Then, you can download the Pennsylvania Startup Costs Worksheet template.

- If you do not have an account and wish to start using US Legal Forms, follow these steps.

- Find the form you need and ensure it is for the correct state/region.

- Use the Review option to examine the form.

- Check the information to ensure you have selected the correct form.

- If the form isn't what you're looking for, utilize the Search field to find the form that suits your needs.

Form popularity

FAQ

You report start-up costs on your tax return using IRS Form 4562. This form allows you to summarize your start-up expenses and indicate what you plan to write off. By organizing your records with a Pennsylvania Startup Costs Worksheet, you will find reporting your start-up costs straightforward and efficient.

What are examples of startup costs? Examples of startup costs include licensing and permits, insurance, office supplies, payroll, marketing costs, research expenses, and utilities.

What are examples of startup costs? Examples of startup costs include licensing and permits, insurance, office supplies, payroll, marketing costs, research expenses, and utilities.

Under GAAP, you report organizational or startup costs as an expense when you incur them. If you spend $5,000 on employee training prior to opening, you'd record $5,000 as a startup expense and reduce your cash account by $5,000. When you make out your taxes, the accounting for startup costs is more complicated.

It's a cost a business could deduct if they paid or incurred it to operate an existing active trade or business, in the same field as the one the business entered into. It's a cost a business pays or incurs before the day their active trade or business begins.

The IRS allows you to deduct $5,000 in business startup costs and $5,000 in organizational costs, but only if your total startup costs are $50,000 or less. If your startup costs in either area exceed $50,000, the amount of your allowable deduction will be reduced by the overage.

In other words, the money you spend for advertising, training employees, legal and accounting expenses and other pre-opening costs are accumulated into one lump-sum "startup costs" and recorded as an asset on your balance sheet.

Essentially, the accounting for startup activities is to expense them as incurred. While the guidance is simple enough, the key issue is not to assume that other costs similar to start-up costs should be treated in the same way.

Under Generally Accepted Accounting Principles, you report startup costs as expenses incurred at the time you spend the money. Some of your initial expenses, such as buying equipment, are not classified as startup costs under GAAP and have to be capitalized, not expensed.

Start-up expenses are the costs of getting your business up and running. These include buying or leasing space, marketing costs, equipment, licenses, salaries, and the cost of servicing loans. Start-up assets are items of value, such as cash on hand, equipment, land, buildings, inventory, etc.