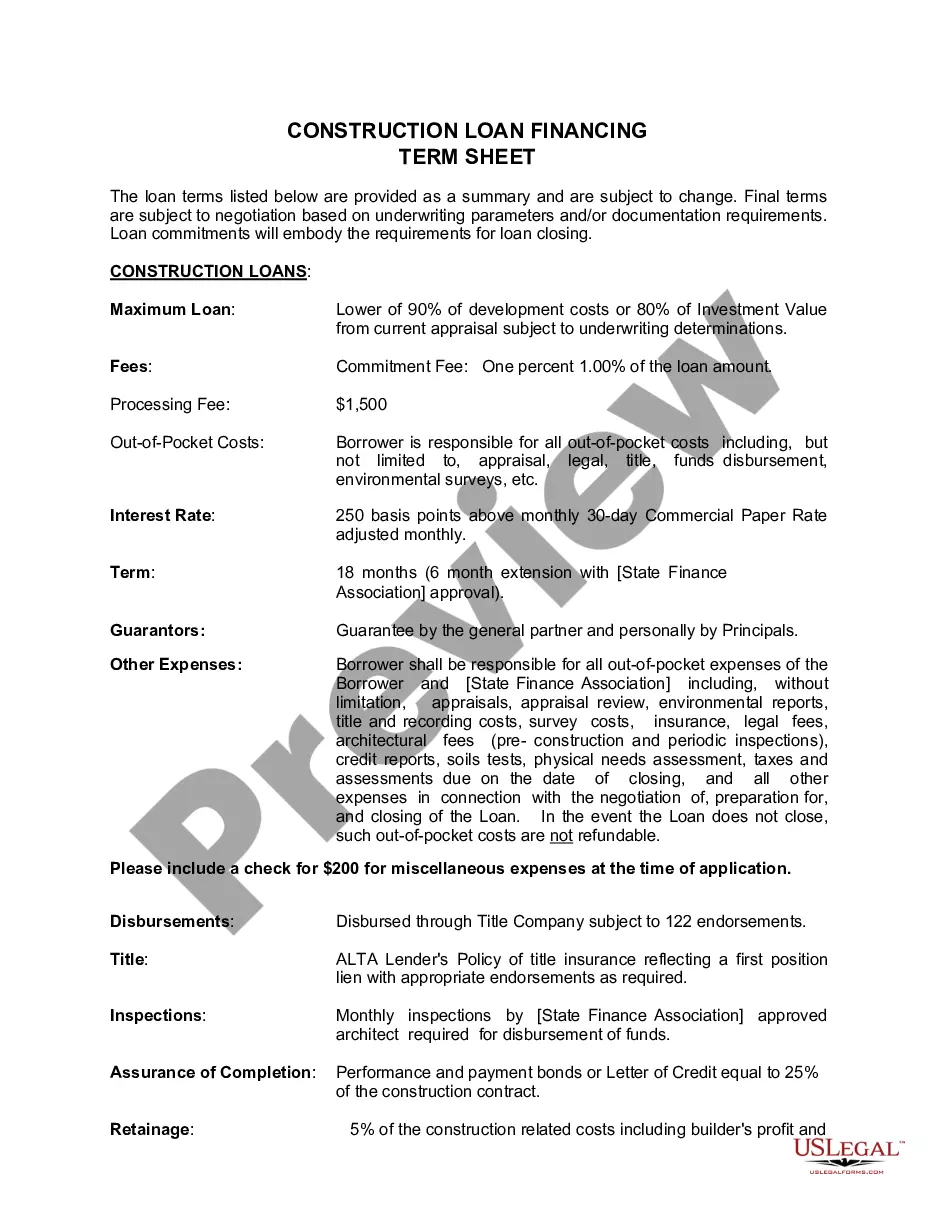

Oregon Construction Loan Financing Term Sheet

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Construction Loan Financing Term Sheet?

You are able to devote time on-line trying to find the legal file design which fits the state and federal requirements you need. US Legal Forms supplies a huge number of legal varieties that happen to be analyzed by pros. It is simple to download or print out the Oregon Construction Loan Financing Term Sheet from our assistance.

If you already have a US Legal Forms bank account, it is possible to log in and click the Obtain option. After that, it is possible to complete, change, print out, or indicator the Oregon Construction Loan Financing Term Sheet. Every single legal file design you buy is yours permanently. To obtain yet another version of the purchased type, proceed to the My Forms tab and click the related option.

If you work with the US Legal Forms internet site for the first time, adhere to the straightforward recommendations below:

- Initially, be sure that you have selected the proper file design to the state/city that you pick. See the type information to make sure you have selected the correct type. If readily available, utilize the Review option to search throughout the file design as well.

- If you want to locate yet another variation of the type, utilize the Search area to obtain the design that meets your requirements and requirements.

- After you have located the design you would like, just click Buy now to carry on.

- Choose the pricing prepare you would like, enter your accreditations, and register for a free account on US Legal Forms.

- Comprehensive the purchase. You can utilize your bank card or PayPal bank account to cover the legal type.

- Choose the format of the file and download it to your gadget.

- Make modifications to your file if possible. You are able to complete, change and indicator and print out Oregon Construction Loan Financing Term Sheet.

Obtain and print out a huge number of file layouts making use of the US Legal Forms web site, that offers the most important variety of legal varieties. Use professional and express-distinct layouts to handle your organization or specific requirements.

Form popularity

FAQ

If the loan is a revolving line of credit or similar arrangement with no scheduled payments, loan costs generally should be amortized using the straight-line method over the period the line is active.

Concepts Statement 6 further states that debt issuance costs cannot be an asset because they provide no future economic benefit.

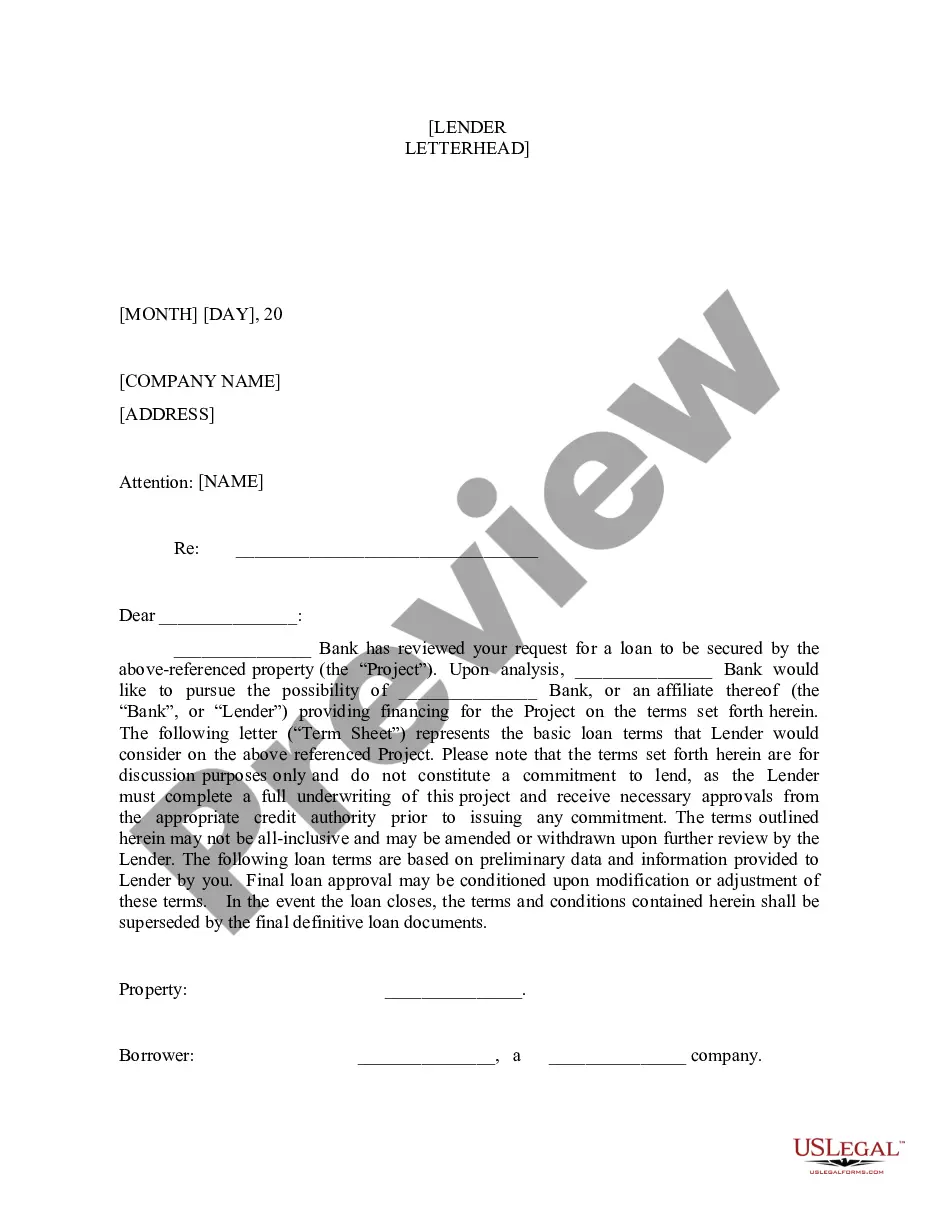

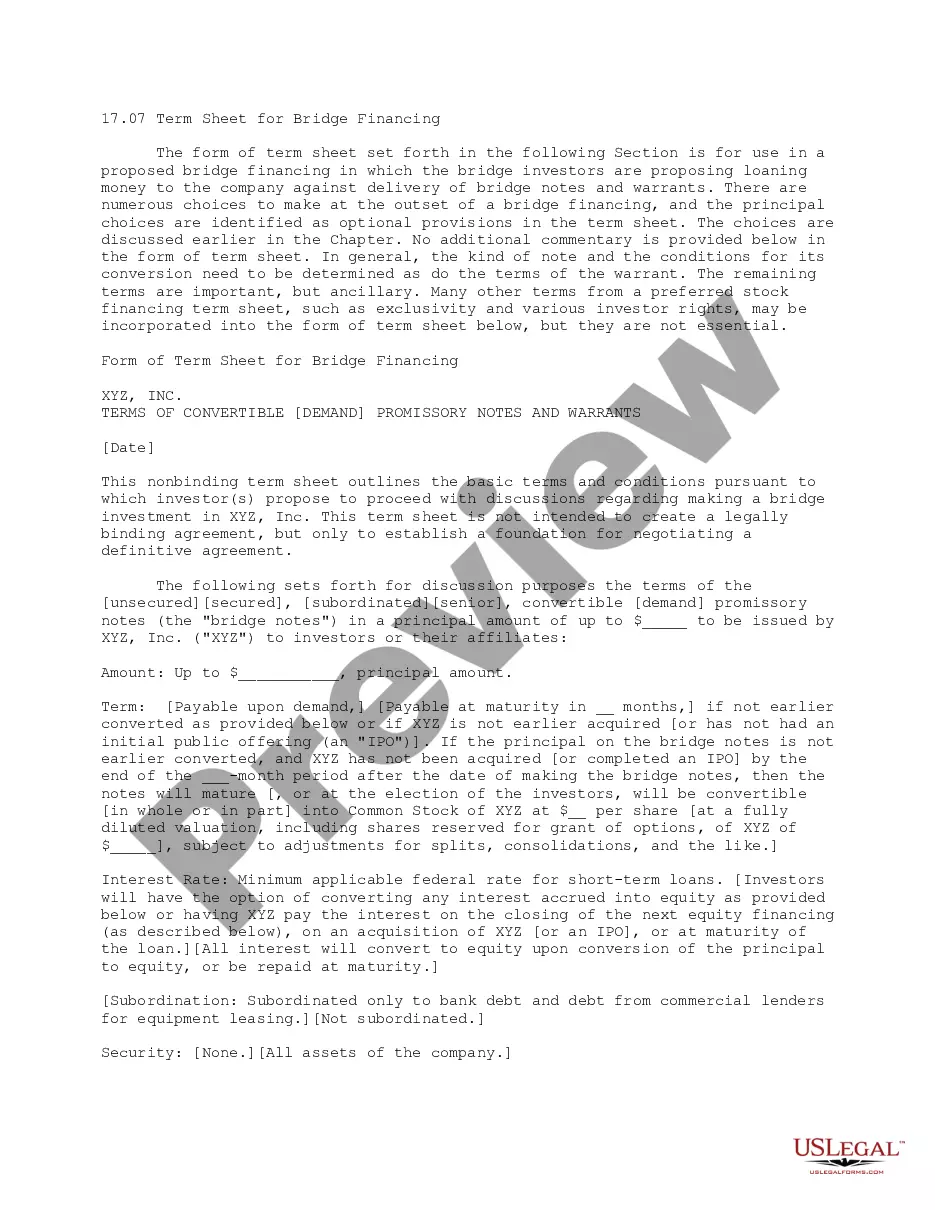

A term sheet is designed to help the parties to the loan to set out clearly and in advance, the terms on which the loan will be made. It serves as a non-binding letter of intent which summarises all the important financial and legal terms as well as quantifying the amount of the loan and its repayment.

During the construction of a building, the cost of interest on a construction loan should be capitalized. Companies should capitalize all avoidable interest costs it incurs during the construction phase of property, plant, and equipment, but not interest incurred after the asset has been put to use.

As mentioned, construction loans are short-term loans, usually no longer than a year in length. On the other hand, traditional mortgages are long-term loans, with terms typically ranging from 15 ? 30 years. With a mortgage, the borrower receives the money in one lump sum.

Typically, interest paid on a loan is immediately expensed and is tax deductible but that isn't always the case. For example, construction interest expense that is incurred during the period up until the time the asset begins to produce revenue is capitalized by adding it to the cost basis of the asset.

The overarching accounting theory when accounting for these debt issuance costs is the utilization of the matching principle. This means that to properly match these costs with the new loan, the costs should be capitalized and amortized over the term of the loan.

Calculating the monthly interest payment is as simple as applying the loan's interest rate to that $20,000. If your interest rate is 6.5%, you can expect your monthly interest payment (for that month) to be $1,300.