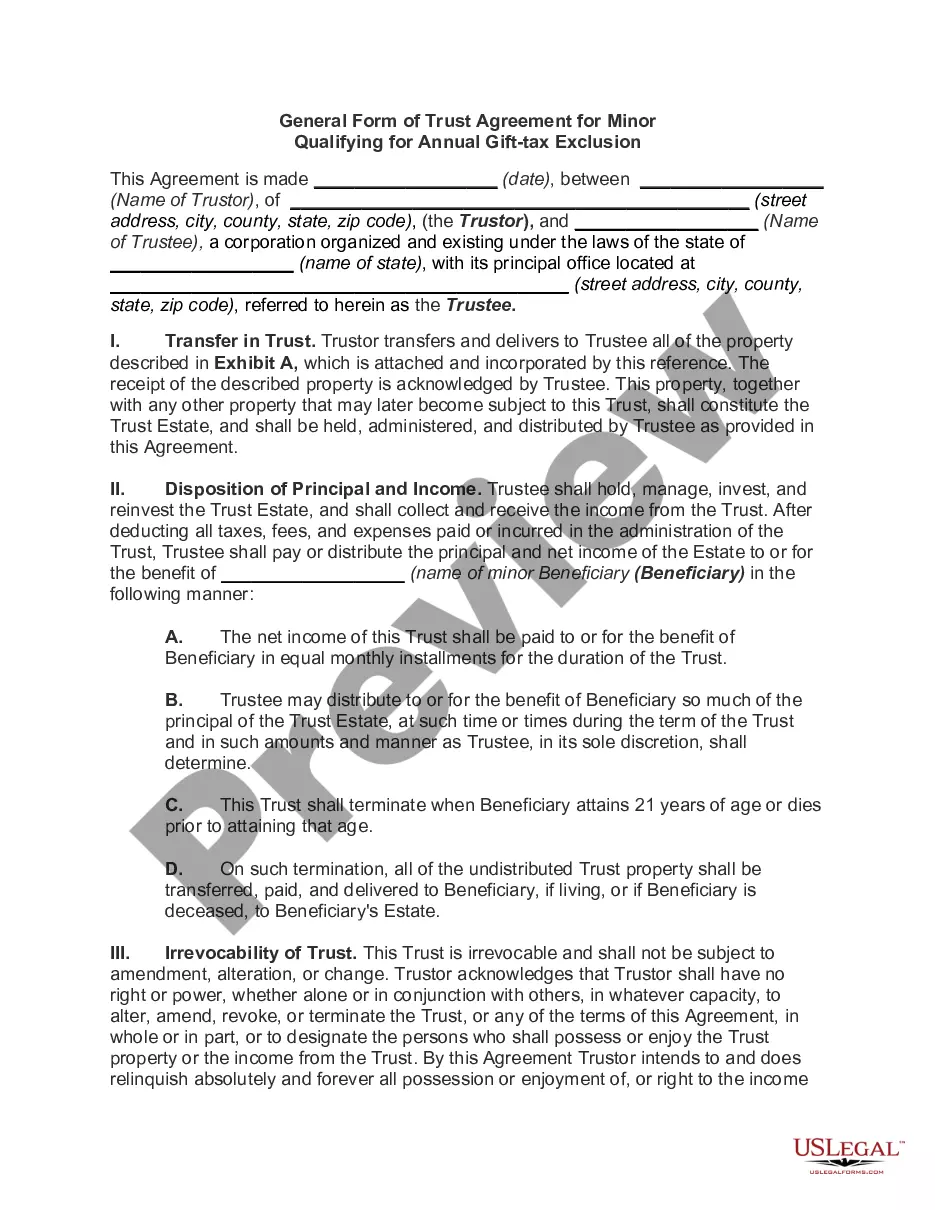

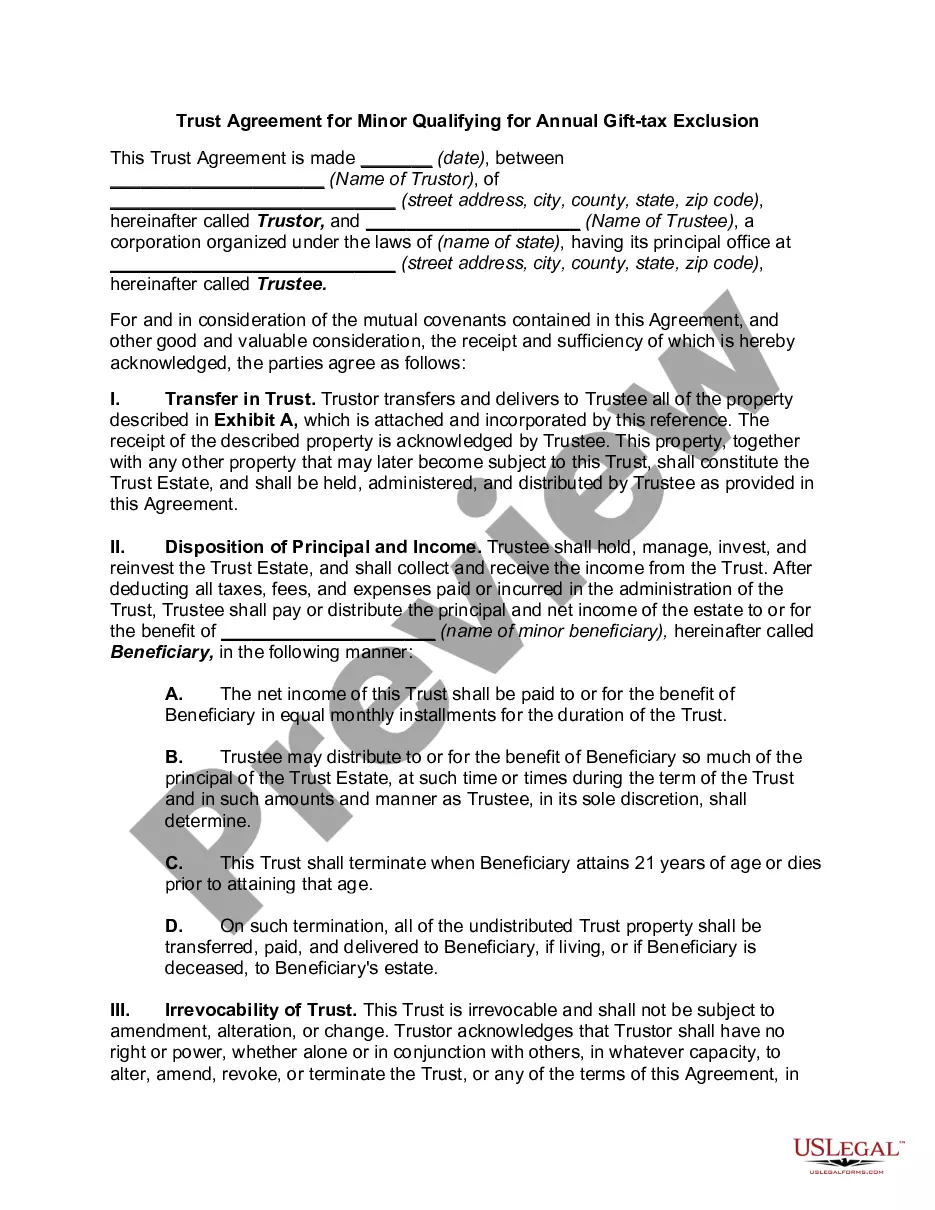

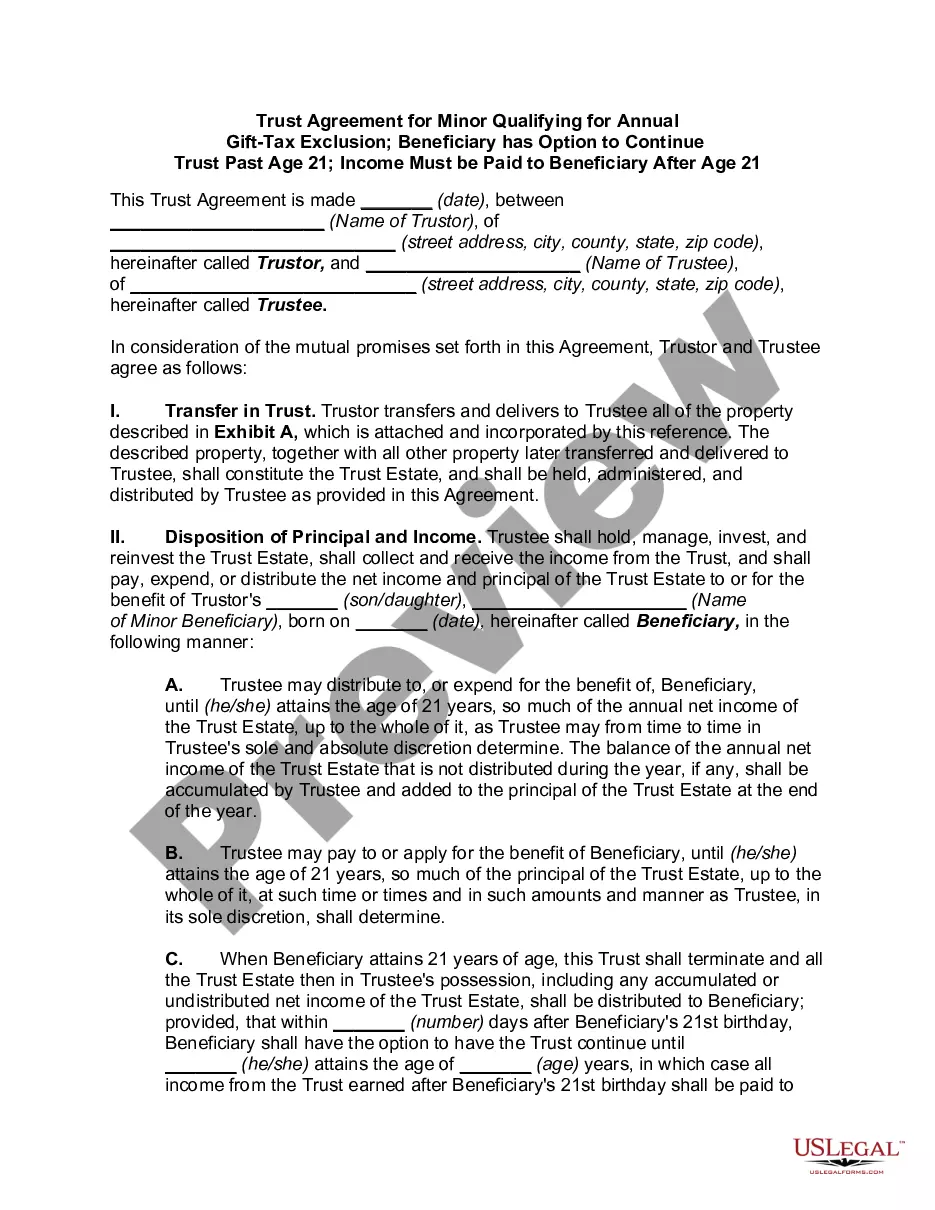

This form set up what is known as present interest trusts, with the intention of meeting the requirements of Section 2503(c) of the Internal Revenue Code.

Oregon Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children

Instant download

Description

Free preview

How to fill out Trust Agreement For Minors Qualifying For Annual Gift Tax Exclusion - Multiple Trusts For Children?

US Legal Forms - one of the largest collections of legal documents in the United States - provides a variety of legal form templates that you can download or print.

By using the website, you can access thousands of forms for business and personal purposes, organized by categories, states, or keywords. You can find the latest versions of forms like the Oregon Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children in just seconds.

If you already hold a subscription, Log In to download the Oregon Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children from the US Legal Forms catalog. The Download button appears on every form you view. You can access all previously downloaded forms under the My documents tab of your account.

Process the payment. Use a credit card or PayPal account to complete the transaction.

Select the format and download the form to your device. Make changes. Fill in, modify, print, and sign the downloaded Oregon Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children. Every template you add to your account does not expire and belongs to you forever. Therefore, if you wish to download or print another copy, simply go to the My documents section and click on the form you want. Access the Oregon Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children with US Legal Forms, the largest collection of legal document templates. Utilize thousands of professional and state-specific templates that meet your business or personal needs.

- Ensure you have selected the correct form for your city/region.

- Click on the Review button to examine the form’s content.

- Check the form description to ensure you have chosen the right form.

- If the form does not meet your requirements, use the Search field at the top of the screen to find one that does.

- If you are satisfied with the form, confirm your selection by clicking the Buy now button.

- Then, choose the payment plan you prefer and provide your details to register for an account.

Form popularity

FAQ

Choosing between a will and a trust in Oregon depends on your specific circumstances. A trust, especially an Oregon Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children, can offer benefits like avoiding probate and providing for minors directly. However, a will is easier and less expensive to set up. Evaluating your estate planning needs can help you determine the best option for your family.

Putting your car in a trust in Oregon can provide protection and simplify the transfer of ownership. This is especially relevant if you have created an Oregon Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children. By placing your vehicle in a trust, you can ensure that it is managed according to your wishes and can avoid probate complications. Make sure to consider your long-term goals before making this decision.

Gifts qualifying for the Generation-Skipping Transfer (GST) annual exclusion typically include direct gifts to grandchildren or other beneficiaries in a lower generation. Similar to the general gift tax exclusions, these must adhere to federal limits. Using an Oregon Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children can facilitate compliance and maximize the benefits of the GST exclusion.

One of the biggest mistakes parents make when setting up a trust fund is failing to clearly define the terms and conditions. Clarity is vital in ensuring that the trust meets its intended purpose, especially when it comes to an Oregon Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children. Consulting with a legal expert can help avoid these pitfalls and create a more effective trust.

Yes, gifts to certain types of trusts can qualify for the annual gift tax exclusion. Generally, the gift must be of a present interest, meaning the beneficiaries must have immediate access to the benefit. When using an Oregon Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children, ensure the terms allow for this access to maximize tax benefits.

Gifts that fall under the annual gift tax exclusion do not need to be reported on your tax return, as long as they do not exceed the annual limit set by the IRS. However, any gifts above the exclusion limit must be reported. Utilizing an Oregon Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children can help manage these limits effectively.

To avoid gift tax in Oregon, consider utilizing the annual gift tax exclusion, which allows you to gift a certain amount each year without incurring taxes. Incorporating trusts, such as an Oregon Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children, can help in strategically managing these gifts. This method not only benefits your children but also helps preserve your wealth.

In Oregon, a trust is a legal arrangement that allows a trustee to manage assets on behalf of beneficiaries. The person who creates this trust, known as the grantor, can set specific terms for distribution. Trusts can provide a structured way to ensure that assets are protected and efficiently transferred to minors, especially with an Oregon Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children.

A Crummey Trust is typically considered a grantor trust because the person who sets it up retains certain powers over the trust. This arrangement allows contributions to qualify for the annual gift tax exclusion, making it advantageous for managing an Oregon Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children. By establishing such a trust, you can effectively provide for your minors while taking advantage of tax benefits.

To execute a trust in Oregon, you begin by drafting a trust document that outlines the terms, conditions, and the trustee's role. It is essential to have the document signed and notarized to ensure its validity. Following the establishment of an Oregon Trust Agreement for Minors Qualifying for Annual Gift Tax Exclusion - Multiple Trusts for Children, transferring assets into the trust is the final step, allowing you to specify how and when your children will access the funds.