Oregon Bankruptcy Guide and Forms Package for Chapters 7 or 13

About this form

The Oregon Bankruptcy Guide and Forms Package for Chapters 7 or 13 provides essential legal documents and guidance specifically tailored for individuals seeking to file for bankruptcy in Oregon. This package distinguishes itself by offering comprehensive instructions and resources to help you navigate either Chapter 7, which focuses on liquidation, or Chapter 13, which allows for a repayment plan. By utilizing these forms, you can effectively understand your rights and responsibilities under bankruptcy law.

Key parts of this document

- Chapter 7 Bankruptcy Overview: Details about the liquidation process and eligibility requirements.

- Chapter 13 Bankruptcy Overview: Information on repayment plans and filing procedures.

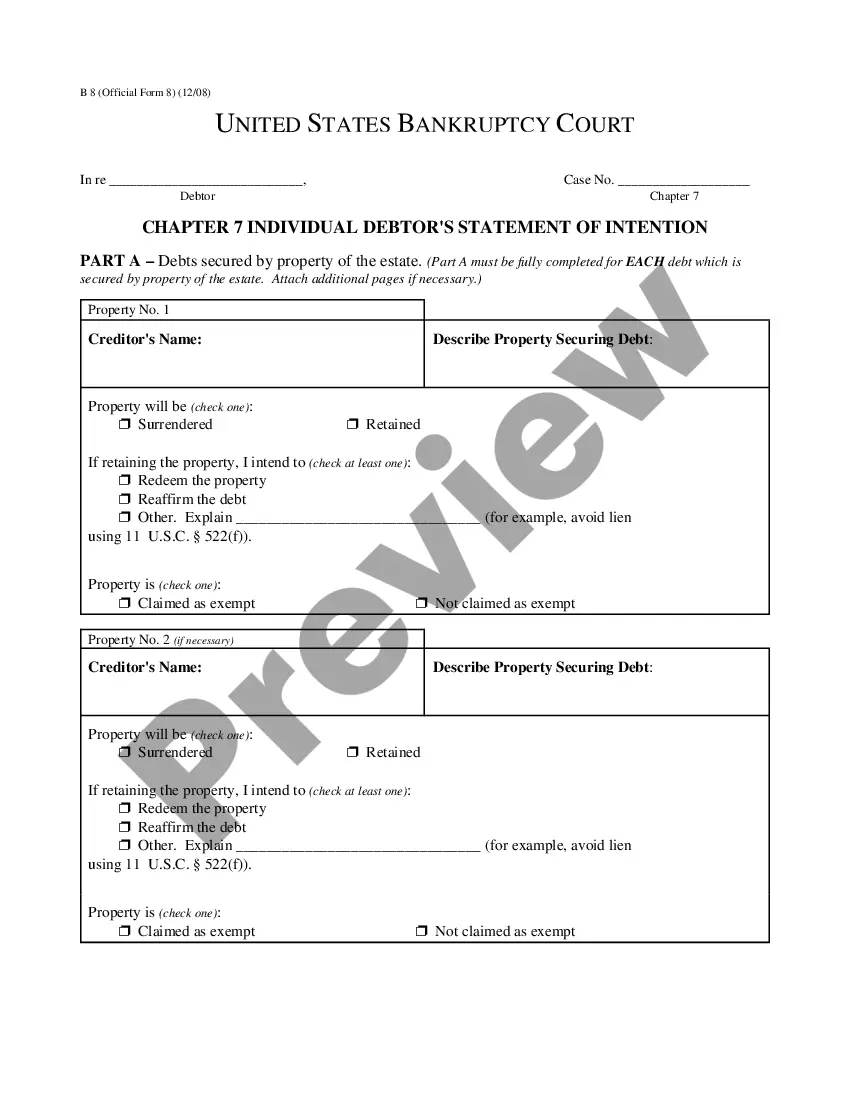

- Current Monthly Income Statement (Official Form 122A-1): Used to determine if you qualify for Chapter 7.

- Chapter 7 Means Test Calculation (Official Form 122A-2): A form to assess financial eligibility for Chapter 7.

- Exemption Schedule (Schedule C - Official Form 106C): To declare property that you wish to exempt from the bankruptcy process.

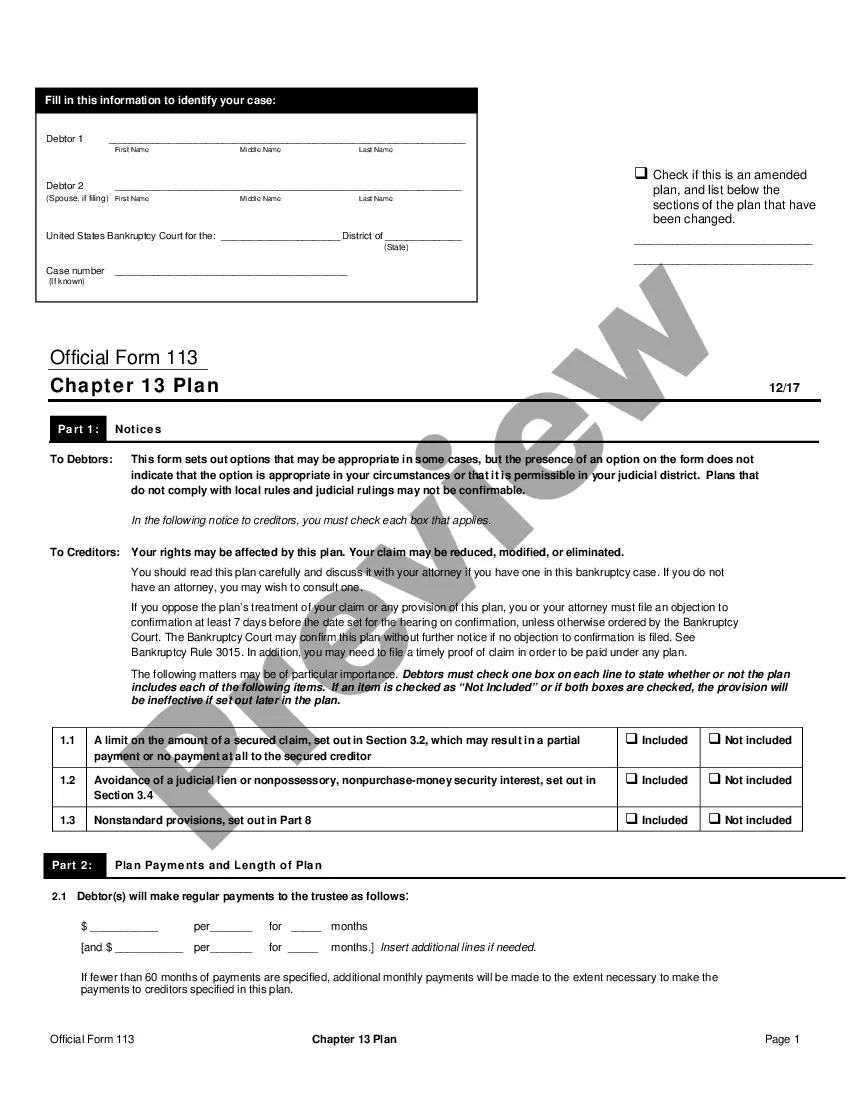

- Chapter 13 Repayment Plan: Detailed guidance on creating a feasible repayment plan for creditors.

When to use this document

This package is necessary when you are considering filing for bankruptcy under Chapters 7 or 13 in Oregon. It is useful for individuals facing overwhelming debt, it helps you determine the most suitable chapter to file under based on your financial situation. Use this guide if you are struggling to repay debts and need a structured way to either liquidate assets or establish a repayment plan based on your income.

Intended users of this form

- Individuals who are overwhelmed by debt and considering filing for bankruptcy.

- Married couples filing jointly for bankruptcy under either Chapter 7 or Chapter 13.

- Sole proprietors seeking relief from personal and business debts.

- Any individual needing clear guidance and forms to navigate the bankruptcy process in Oregon.

How to prepare this document

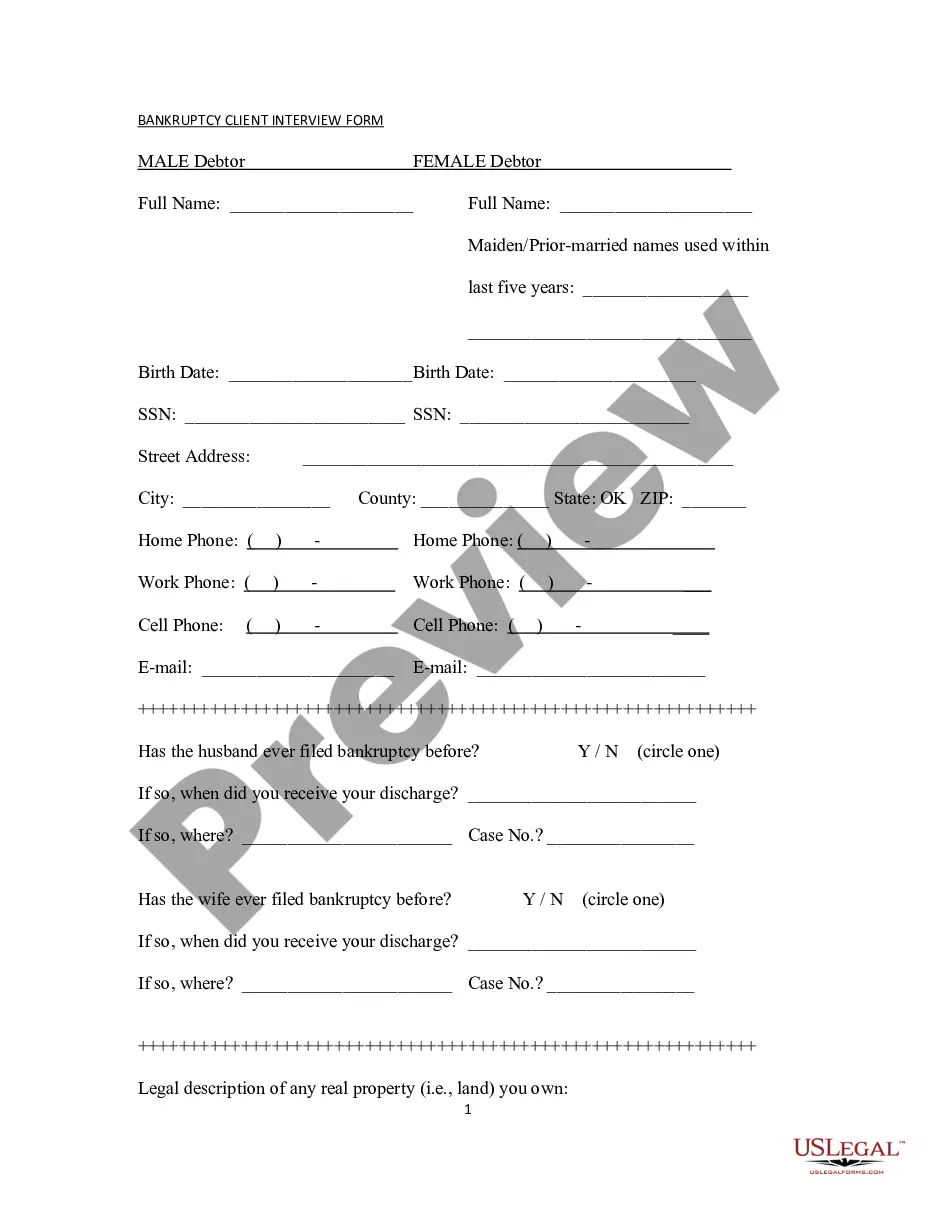

- Gather all financial documentation that reflects your income, debts, and assets.

- Determine which chapter of bankruptcy to file based on your financial situation and goals.

- Complete the Current Monthly Income Statement and Chapter 7 Means Test Calculation forms if filing under Chapter 7.

- Prepare the Chapter 13 repayment plan if filing under Chapter 13, ensuring that it meets all legal requirements.

- Review the Exemption Schedule to list any property you wish to protect from bankruptcy proceedings.

- File the completed forms with the appropriate bankruptcy court in Oregon.

Is notarization required?

This form does not typically require notarization to be legally valid. However, some jurisdictions or document types may still require it. US Legal Forms provides secure online notarization powered by Notarize, available 24/7 for added convenience.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Common mistakes

- Failing to accurately report all income and assets, which can affect discharge eligibility.

- Neglecting to complete all required forms, leading to delays or dismissals in the bankruptcy process.

- Choosing the wrong chapter without fully understanding the implications for your financial situation.

- Forgetting to claim exemptions, resulting in losing property that could otherwise be protected.

Advantages of online completion

- Convenience of downloading forms anytime, which saves time compared to traditional filing.

- Editable forms that allow you to enter your information easily and accurately.

- Access to up-to-date legal resources and instructions to ensure compliance with current laws.

- Your information is securely stored, providing peace of mind during the filing process.

Looking for another form?

Form popularity

FAQ

In many cases, Chapter 7 bankruptcy is a better fit than Chapter 13 bankruptcy. For instance, Chapter 7 is quicker, many filers can keep all or most of their property, and filers don't pay creditors through a three- to five-year Chapter 13 repayment plan.

A Chapter 13 bankruptcy involves repaying some or all of your debt over a three- to- five-year period, while a Chapter 7 bankruptcy involves wiping out most of your debts without paying them back.In that way, a Chapter 13 may be better for your credit than a Chapter 7.

Chapter 11 bankruptcy works well for businesses and individuals whose debt exceeds the Chapter 13 bankruptcy limits. In most cases, Chapter 13 is the better choice for qualifying individuals and sole proprietors.

With Chapter 7, those types of debts are wiped out with your filing's court approval, which can take a few months. Under Chapter 13, you need to continue making payments on those balances throughout your court-instructed repayment plan; afterwards, the unsecured debts may be discharged.

Chapter 13 Is Likely to Worsen Your Finances When your Chapter 13 case is dismissed, you are often in a far worse financial position. That's because the interest on your unpaid debts has continued to mount as you've struggled to make payments. And once you're out of bankruptcy protection, you have more debt than ever.

How soon can you file for Chapter 13 after Chapter 7 bankruptcy? In order to get debts discharged through Chapter 13, you must wait four years after filing a Chapter 7 bankruptcy.

How soon can you file for Chapter 13 after Chapter 7 bankruptcy?You can file for a Chapter 13 before four years if no debts were discharged in the Chapter 7 filing, but if you had debts discharged in Chapter 7 and want to have debts discharged in Chapter 13, you must wait four years.

A chapter 13 bankruptcy is also called a wage earner's plan. It enables individuals with regular income to develop a plan to repay all or part of their debts. Under this chapter, debtors propose a repayment plan to make installments to creditors over three to five years.

Key Takeaways. Chapter 7 bankruptcy doesn't require a repayment plan but does require you to liquidate or sell nonexempt assets to pay back creditors.Chapter 13 bankruptcy eliminates qualified debt through a repayment plan over a three- or five-year period.