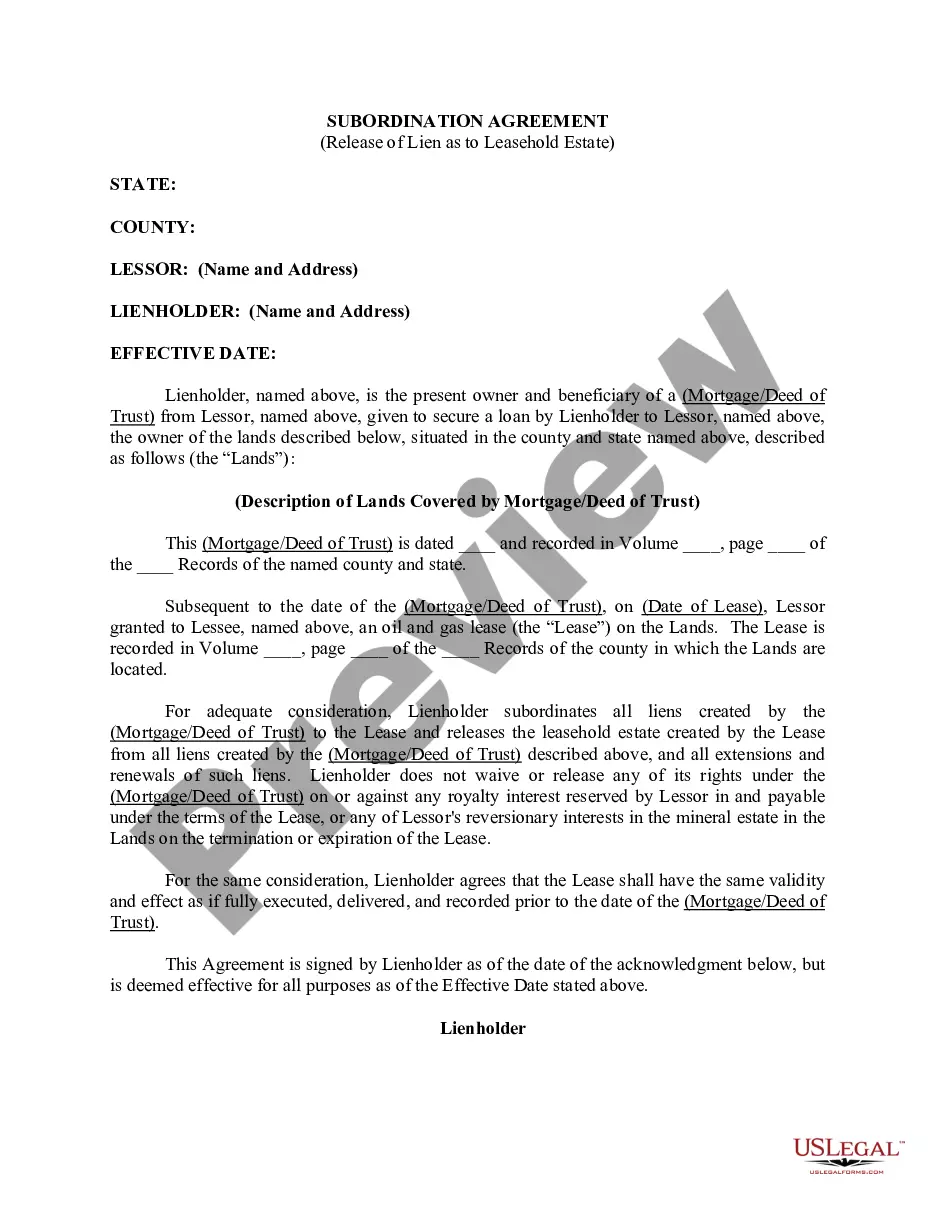

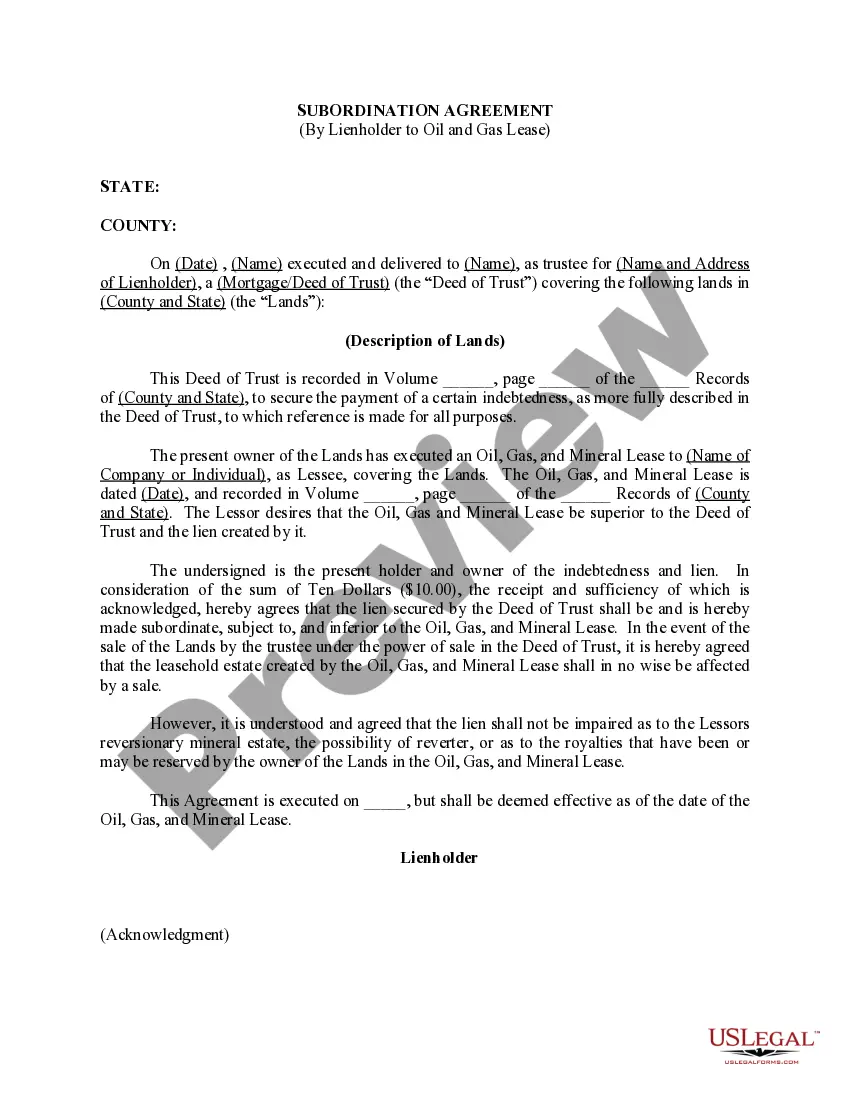

Oklahoma Subordination Agreement with no Reservation by Lienholder

Description

How to fill out Subordination Agreement With No Reservation By Lienholder?

It is possible to spend hours online trying to find the authorized file design which fits the federal and state needs you require. US Legal Forms offers a huge number of authorized types which can be evaluated by professionals. You can easily download or printing the Oklahoma Subordination Agreement with no Reservation by Lienholder from our services.

If you have a US Legal Forms profile, you are able to log in and then click the Download key. After that, you are able to complete, revise, printing, or signal the Oklahoma Subordination Agreement with no Reservation by Lienholder. Each authorized file design you purchase is yours permanently. To acquire yet another backup of the purchased develop, check out the My Forms tab and then click the corresponding key.

If you work with the US Legal Forms website the first time, adhere to the simple guidelines under:

- Initial, make sure that you have selected the proper file design for the county/metropolis of your choice. See the develop information to ensure you have selected the right develop. If offered, make use of the Review key to appear with the file design as well.

- If you would like locate yet another model of the develop, make use of the Look for area to discover the design that suits you and needs.

- After you have identified the design you would like, just click Purchase now to proceed.

- Pick the pricing prepare you would like, key in your credentials, and sign up for a free account on US Legal Forms.

- Full the purchase. You should use your bank card or PayPal profile to cover the authorized develop.

- Pick the formatting of the file and download it in your product.

- Make alterations in your file if needed. It is possible to complete, revise and signal and printing Oklahoma Subordination Agreement with no Reservation by Lienholder.

Download and printing a huge number of file layouts making use of the US Legal Forms web site, that provides the biggest selection of authorized types. Use specialist and state-distinct layouts to tackle your business or person requirements.

Form popularity

FAQ

The new lender prepares the subordination agreement in conjunction with the subordinating lienholder. Then, the parties typically sign the agreement. But in some cases, just the subordinating lender will need to sign the paperwork.

When you get a mortgage loan, the lender will likely include a subordination clause essentially stating that their lien will take precedence over any other liens placed on the house. A subordination clause serves to protect the lender if a homeowner defaults.

A subordination agreement must be signed and acknowledged by a notary and recorded in the official records of the county to be enforceable.

The creditor usually will require the debtor to sign a subordination agreement which ensures they get paid before other creditors, ensuring they are not taking on high risks.

Key Learning Points. Lien subordination takes place when two or more senior tranches of debt each have a lien on the collateral, but one tranche has first priority while the second has a residual claim. These are referred to as first lien and second lien.

A Subordination Agreement is a legal document that establishes the priority of liens or claims against a specific asset.

To adjust their priority, subordinate lienholders must sign subordination agreements, making their loans lower in priority than the new lender. A subordination agreement puts the new lender into first position and reassigns an existing mortgage to second position or third position, and so on.

Example of a Subordination Agreement A standard subordination agreement covers property owners that take a second mortgage against a property. One loan becomes the subordinated debt, and the other becomes (or remains) the senior debt. Senior debt has higher claim priority than junior debt.