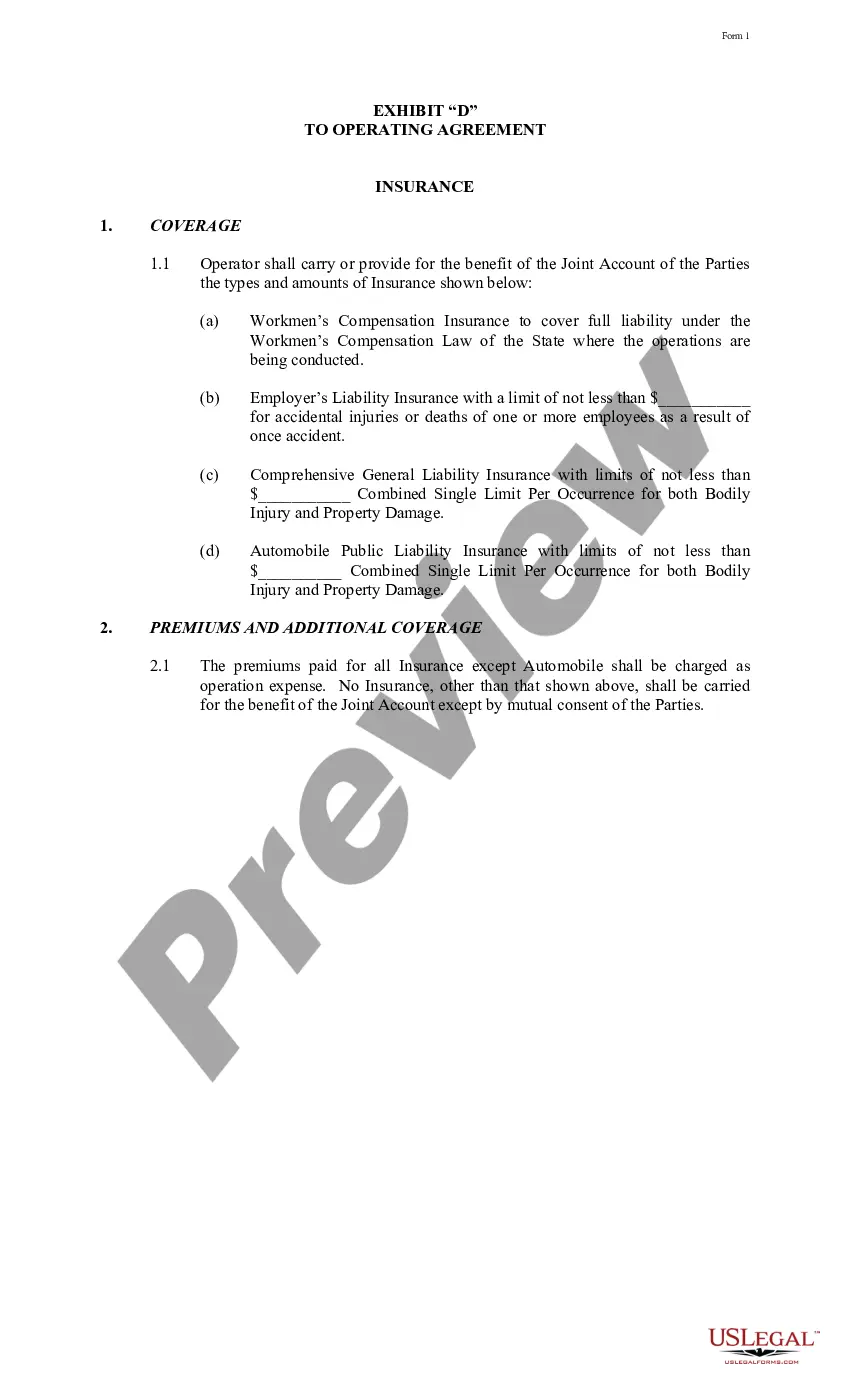

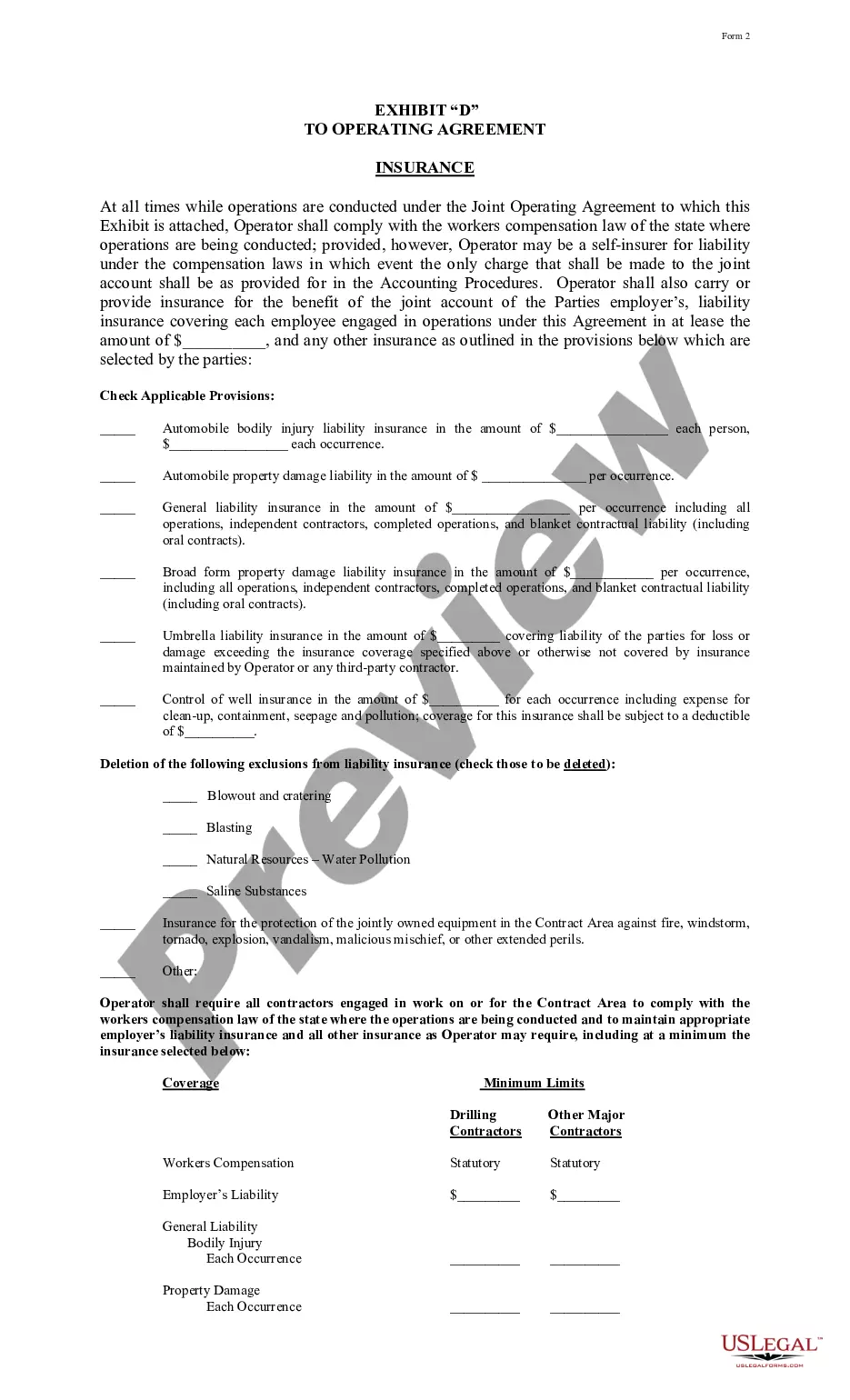

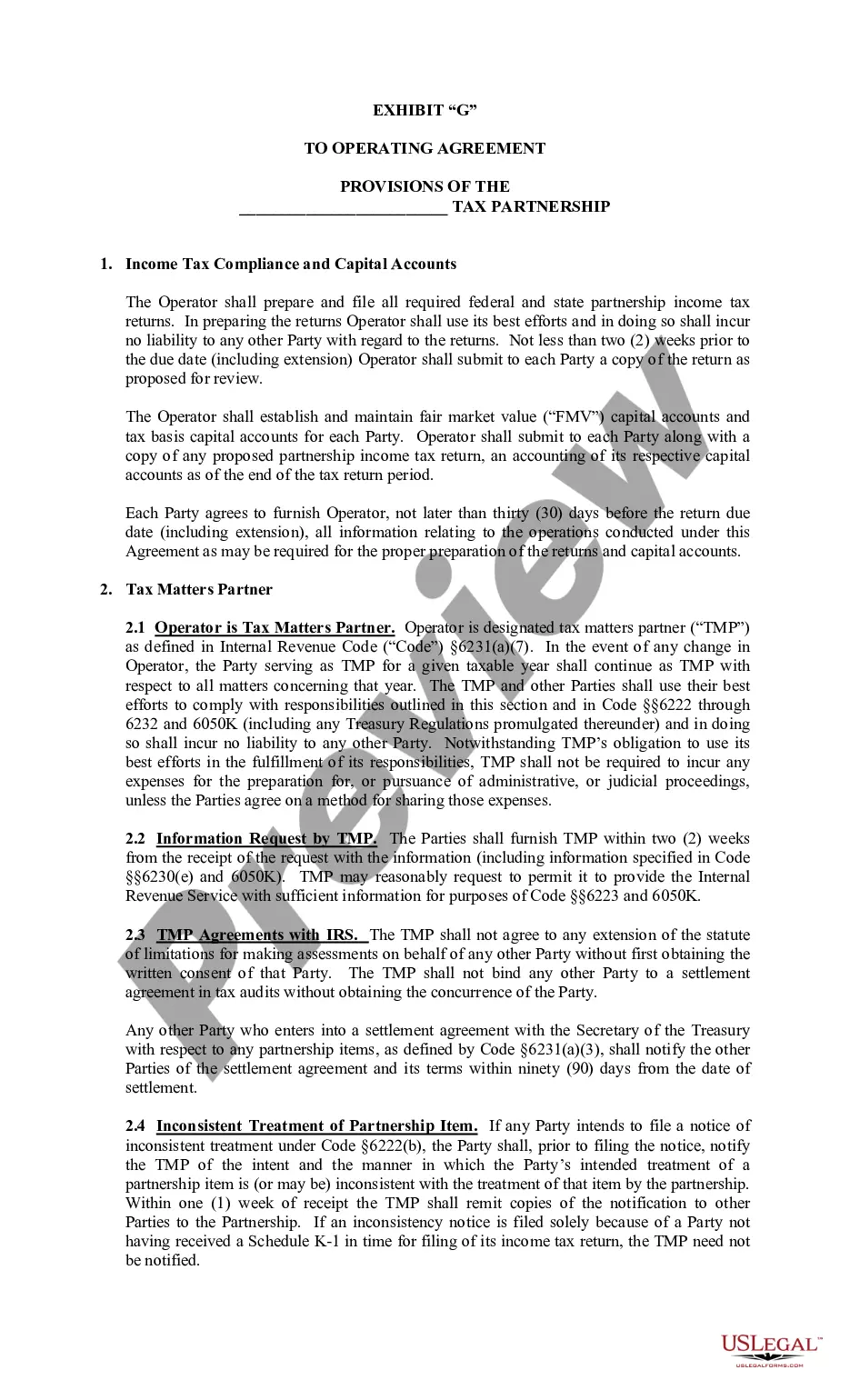

Oklahoma Exhibit C Accounting Procedure Joint Operations

Description

How to fill out Exhibit C Accounting Procedure Joint Operations?

If you have to total, down load, or printing legal document layouts, use US Legal Forms, the greatest variety of legal types, which can be found on the web. Make use of the site`s easy and practical lookup to obtain the papers you require. Various layouts for business and specific reasons are categorized by categories and states, or keywords. Use US Legal Forms to obtain the Oklahoma Exhibit C Accounting Procedure Joint Operations in a few clicks.

Should you be already a US Legal Forms customer, log in to the profile and click the Down load button to find the Oklahoma Exhibit C Accounting Procedure Joint Operations. You can also accessibility types you in the past downloaded within the My Forms tab of your respective profile.

Should you use US Legal Forms the first time, follow the instructions below:

- Step 1. Make sure you have chosen the shape to the proper metropolis/nation.

- Step 2. Make use of the Review method to check out the form`s information. Never forget to read through the outline.

- Step 3. Should you be unhappy with all the develop, use the Research area on top of the display to get other versions from the legal develop web template.

- Step 4. Upon having discovered the shape you require, click on the Buy now button. Pick the prices plan you like and add your credentials to sign up on an profile.

- Step 5. Process the transaction. You can use your charge card or PayPal profile to complete the transaction.

- Step 6. Select the structure from the legal develop and down load it on the gadget.

- Step 7. Complete, revise and printing or indication the Oklahoma Exhibit C Accounting Procedure Joint Operations.

Every single legal document web template you acquire is your own eternally. You may have acces to each develop you downloaded with your acccount. Go through the My Forms portion and choose a develop to printing or down load once again.

Compete and down load, and printing the Oklahoma Exhibit C Accounting Procedure Joint Operations with US Legal Forms. There are millions of professional and state-specific types you can utilize for the business or specific requires.

Form popularity

FAQ

The Joint Operating Agreement (JOA) in oil and gas industry is an underlying contractual framework of a Joint Venture (JV). The JOA is a contract where two or more parties agree to undertake a common task to explore and exploit an area for hydrocarbons.

The Relationship Under a Joint Operating Agreement The standard Form 610 establishes a contractual basis for these multiple leasehold cotenants to operate the properties, jointly share costs and liabilities, and own equipment and production in proportion to their respective percentage of ownership and burdens. Introduction to Joint Operating Agreements - Oil and Gas Law Digest oilandgaslawdigest.com ? primers-insights ? intro... oilandgaslawdigest.com ? primers-insights ? intro...

A joint operating agreement is a legal document that outlines the relationship between two or more businesses who jointly operate a business. When one company partners with another, they are typically signing this type of contract to ensure their business interests are protected.

The operating agreement should include the following: Basic information about the business, such as official name, location, statement of purpose, and registered agent. Tax treatment preference. Member information. Management structure. Operating procedures. Liability statement. Additional provisions.

Example - Shared service centre as a joint operation Company C is structured through a separate vehicle in which Companies A and B each hold a 50% interest. Company C was classified as a joint operation because its activities are primarily designed to serve Companies A and B. Accounting for joint arrangements croneri.co.uk ? cch_uk ? niffs ? ifs24-3-4 croneri.co.uk ? cch_uk ? niffs ? ifs24-3-4

Joint operating agreements are contractual agreements between one party identified as the operator and at least one other party known as a non-operator which requires the operator to drill the initial obligatory well, and the non-operator to pay its proportionate share of the operating expenses.