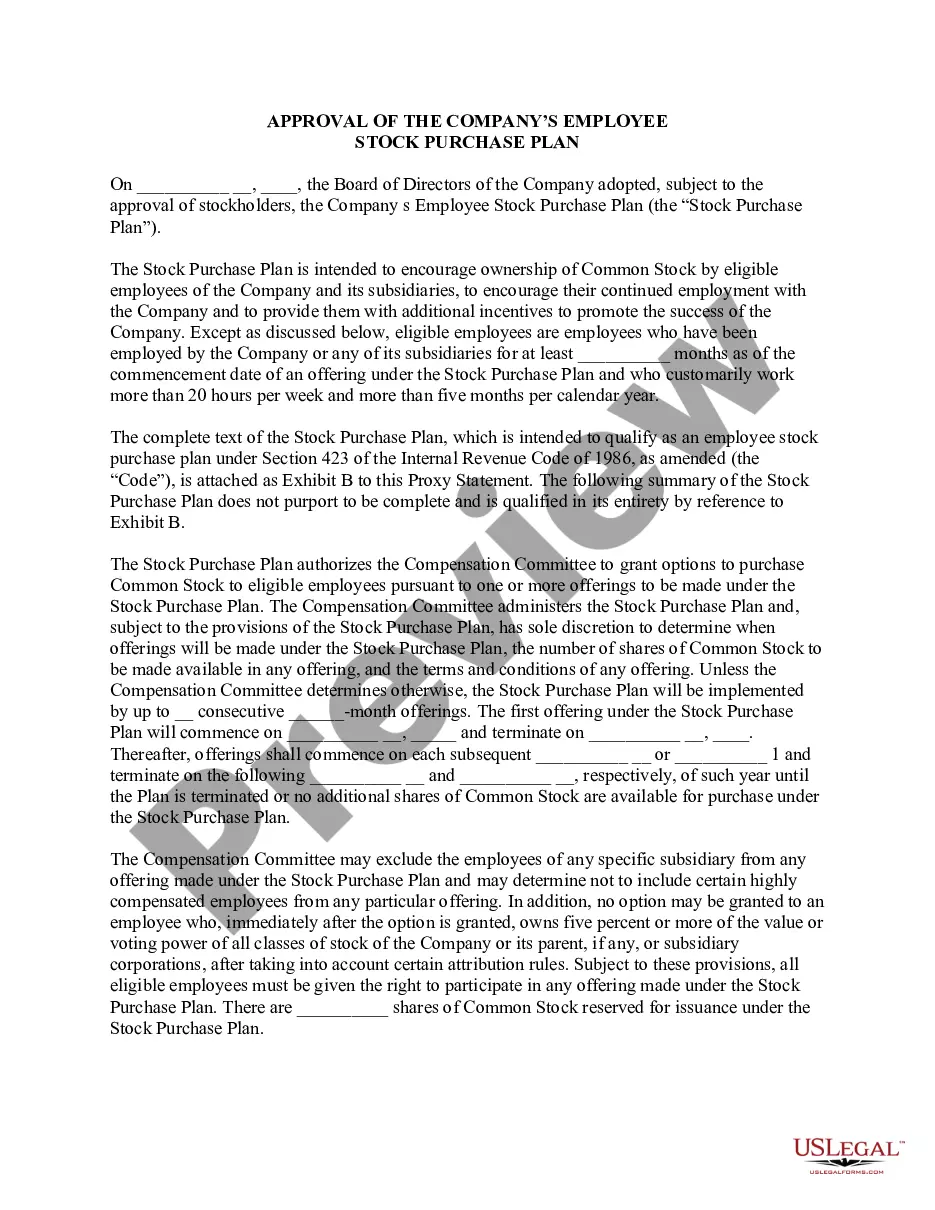

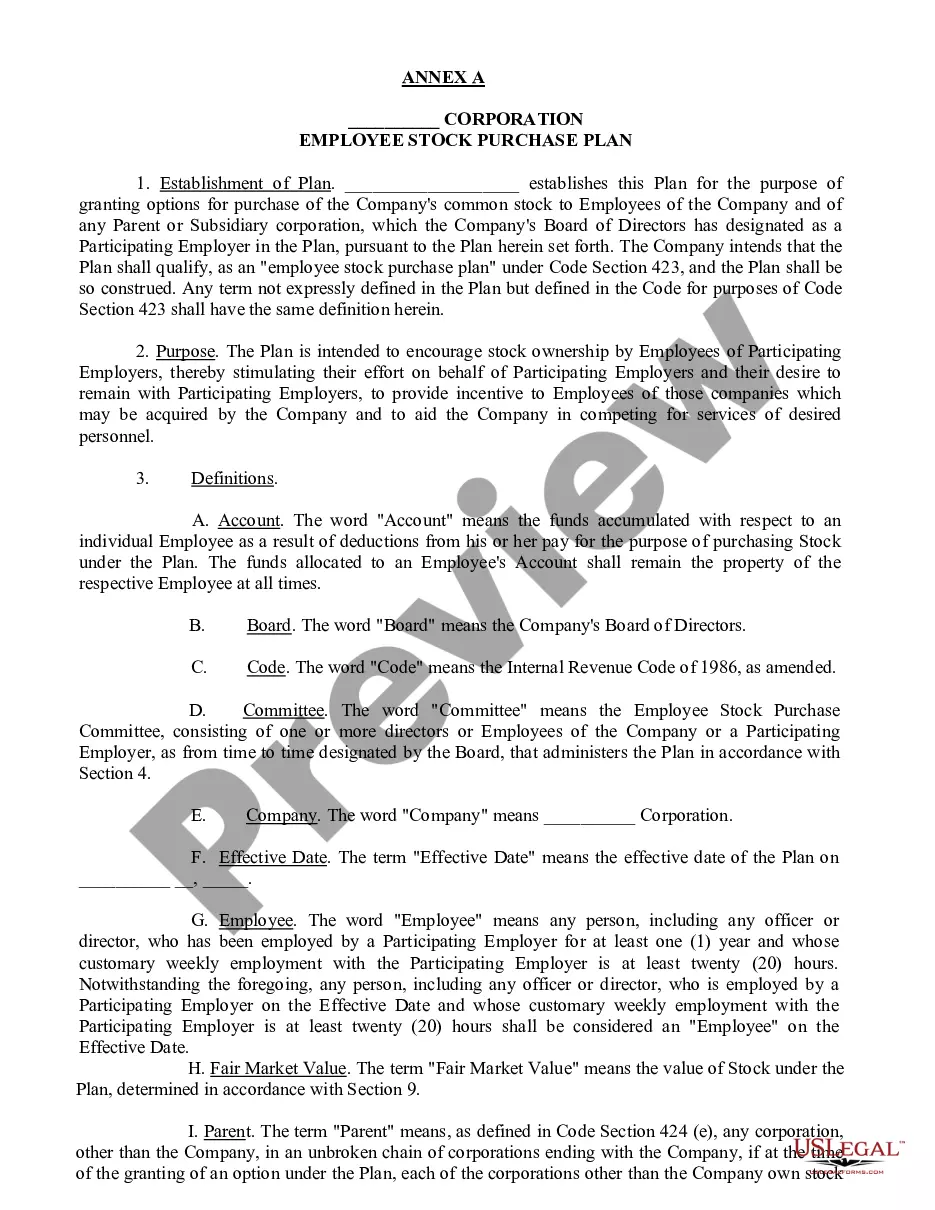

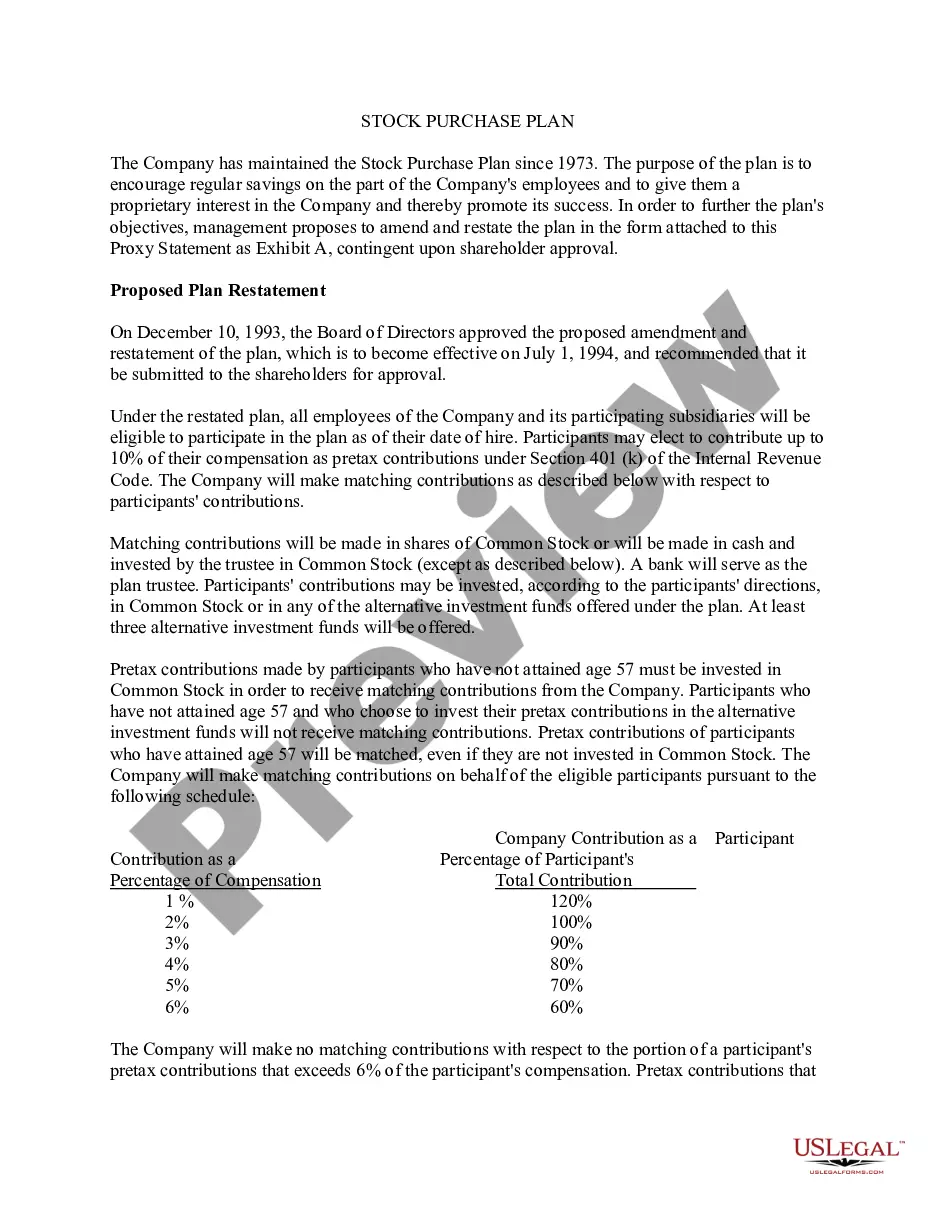

19-179 19-179 . . . Employee Stock Purchase Plan under which each employee of corporation and its wholly-owned direct or indirect, domestic and foreign subsidiaries that have authorized participation in Plan (Participating Company) can contribute up to 15% of earnings through payroll deductions and Participating Company contributes a cash amount equal to 5% of participant's payroll deductions for first year of participation, additional 7% for second year, additional 10% for third year, additional 13% for fourth year and additional 15% for fifth year. Custodian of plan purchases shares of common stock on open market or from corporation at current market prices, using payroll deductions and applicable matching Company contributions

Oklahoma Amended and Restated Employee Stock Purchase Plan

Category:

State:

Multi-State

Control #:

US-CC-19-179

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Amended And Restated Employee Stock Purchase Plan?

You may devote hrs online attempting to find the legal record design that fits the state and federal specifications you require. US Legal Forms offers 1000s of legal types that are evaluated by experts. It is possible to download or produce the Oklahoma Amended and Restated Employee Stock Purchase Plan from your services.

If you already have a US Legal Forms bank account, you are able to log in and then click the Download button. Afterward, you are able to complete, edit, produce, or indication the Oklahoma Amended and Restated Employee Stock Purchase Plan. Each and every legal record design you acquire is your own forever. To acquire one more version associated with a bought type, check out the My Forms tab and then click the corresponding button.

If you use the US Legal Forms website for the first time, stick to the easy instructions beneath:

- Initial, make sure that you have selected the best record design for the area/city that you pick. Browse the type description to make sure you have selected the right type. If readily available, make use of the Review button to search with the record design also.

- In order to find one more version from the type, make use of the Search field to get the design that fits your needs and specifications.

- Upon having located the design you would like, just click Acquire now to continue.

- Find the pricing strategy you would like, type in your credentials, and sign up for your account on US Legal Forms.

- Comprehensive the transaction. You should use your charge card or PayPal bank account to fund the legal type.

- Find the structure from the record and download it for your gadget.

- Make modifications for your record if required. You may complete, edit and indication and produce Oklahoma Amended and Restated Employee Stock Purchase Plan.

Download and produce 1000s of record layouts while using US Legal Forms web site, that provides the greatest selection of legal types. Use skilled and status-particular layouts to handle your business or personal demands.

Form popularity

FAQ

If your company offers a tax-qualified ESPP and you decide to participate, the IRS will only allow you to purchase a maximum of $25,000 worth of stock in a calendar year. Any contributions that exceed this amount are refunded back to you by your company.

ESPP lookback allows you to buy shares at a lower price point. An ESPP lookback allows you to purchase the share price of either A: the enrollment date (1 Jan) or B: the purchase date (30 Jun), whichever is lower.

ESPP Eligibility Cannot participate in an ESPP if an employee owns more than 5% of the company's stock. Must be employed with the company for a specific period of time. (e.g., 1 to 2 years). ESPPs are a benefit.

Taxes on your ESPP transaction will depend on whether the sale is a qualifying disposition or not. The sale will be considered a qualifying disposition if it meets both of these criteria: You held the stocks for at least one year from the PURCHASE date. You held the stocks for at least two years from the OFFERING date.

If your company offers a tax-qualified ESPP and you decide to participate, the IRS will only allow you to purchase a maximum of $25,000 worth of stock in a calendar year. Any contributions that exceed this amount are refunded back to you by your company.

You may withdraw from the ESPP by notifying Fidelity and completing a withdrawal election. When you withdraw, all of the contributions accumulated in your account will be returned to you as soon as administratively possible and you will not be able to make any further contributions during that offering period.

You will continue to own stock purchased for you during your employment, but your eligibility for participation in the plan ends. Any funds withheld from your salary but not used to purchase shares before the end of your employment will be returned to you, normally without interest, within a reasonable period.

In this situation, you sell your ESPP shares more than one year after purchasing them, but less than two years after the offering date. This is a disqualifying disposition because you sold the stock less than two years after the offering (grant) date.