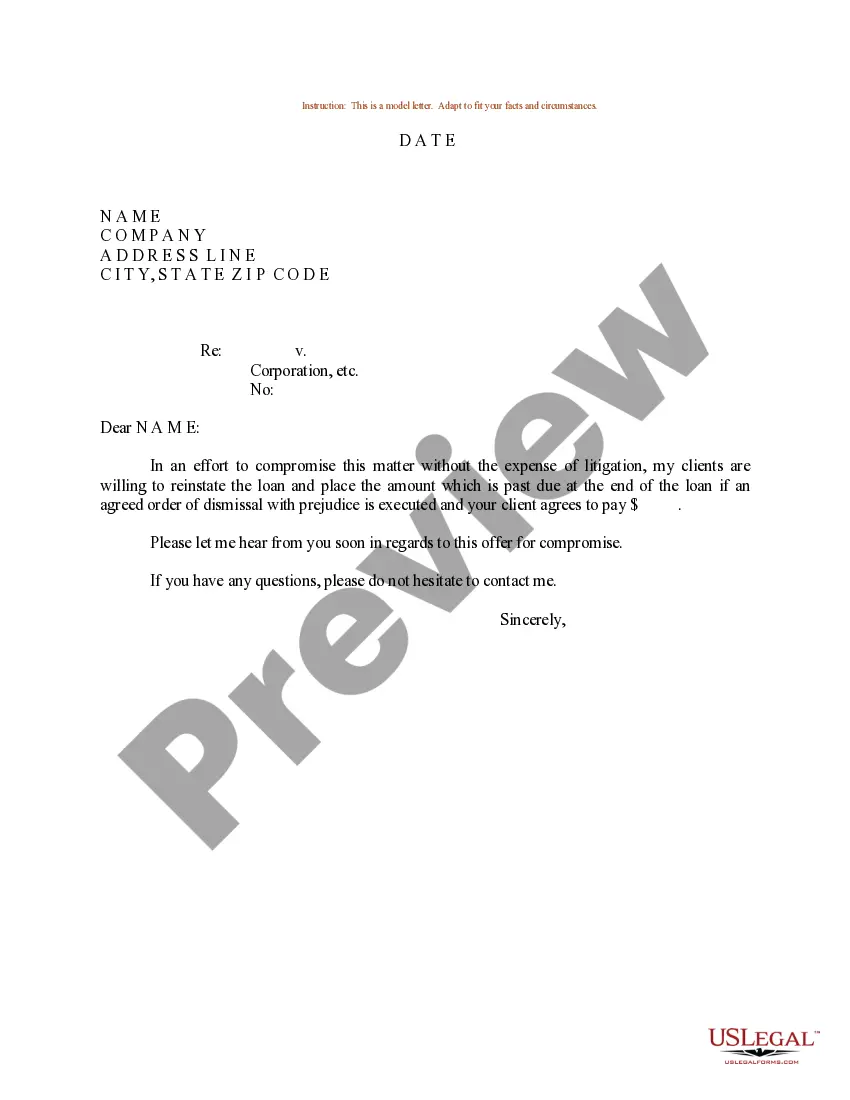

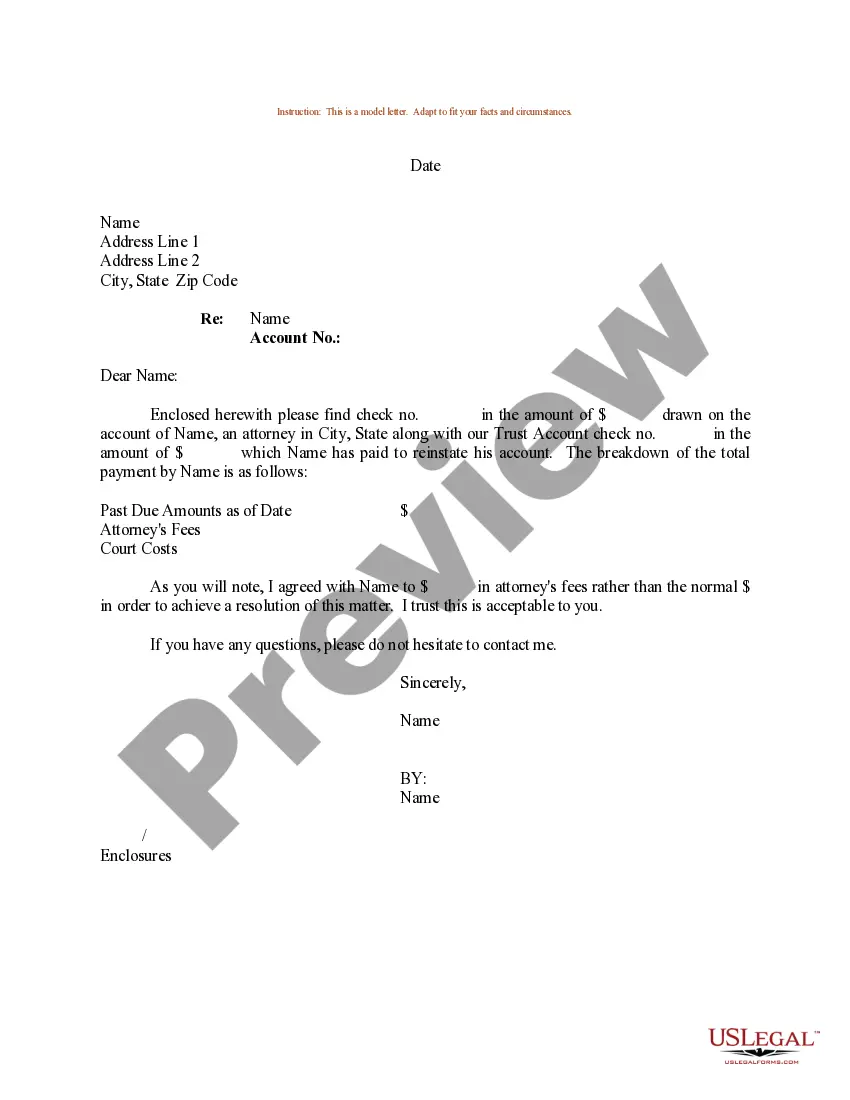

Oklahoma Sample Letter for Insufficient Amount to Reinstate Loan

Description

How to fill out Sample Letter For Insufficient Amount To Reinstate Loan?

Selecting the correct authorized document template can be challenging.

Of course, there are numerous templates accessible online, but how will you find the authorized form you require.

Utilize the US Legal Forms website. This service offers thousands of templates, including the Oklahoma Sample Letter for Insufficient Amount to Reinstate Loan, suitable for both business and personal purposes.

You can review the form using the Review button and read the form description to confirm this is the right one for you.

- All templates are reviewed by experts and comply with federal and state regulations.

- If you are currently registered, Log In to your account and click the Download button to obtain the Oklahoma Sample Letter for Insufficient Amount to Reinstate Loan.

- Use your account to search through the authorized templates you have acquired before.

- Visit the My documents tab of your account and download another copy of the document you require.

- If you are a new user of US Legal Forms, here are simple steps you can follow.

- First, ensure that you have selected the correct form for your city/county.

Form popularity

FAQ

Practicing real estate without a license in Oklahoma can lead to significant penalties, including fines that can reach up to $1,000 per violation. Additionally, individuals may face further disciplinary actions, such as the revocation of privileges. It's crucial to comply with state regulations to avoid these penalties. If you need assistance, consulting resources like an Oklahoma Sample Letter for Insufficient Amount to Reinstate Loan can be beneficial.

Writing a personal statement for reinstatement involves starting with a clear outline of your previous circumstances. Explain what led to your leave and highlight any steps you have taken to address those issues. Lastly, emphasize your commitment to a positive future and request reinstatement. For concrete examples, you might look at an Oklahoma Sample Letter for Insufficient Amount to Reinstate Loan.

In crafting a letter for reinstatement, initiate with a formal salutation and clearly express your request for reinstatement. Provide context by summarizing your situation and the reasons for your reinstatement. Be sure to close with a request for reconsideration and express gratitude for their time and attention. An Oklahoma Sample Letter for Insufficient Amount to Reinstate Loan can guide you in this process.

To write an email for reinstatement, start with a clear subject line, such as 'Request for Reinstatement'. Begin your message by immediately stating your request and briefly explain the circumstances. Be polite and express your enthusiasm about returning. You might find an Oklahoma Sample Letter for Insufficient Amount to Reinstate Loan helpful in crafting your email.

When writing a letter to reinstate an employee, begin with a formal greeting and state the purpose of the letter. Clearly outline the reasons for reinstatement and any relevant performance improvements. Conclude with a warm invitation for them to return to work. For guidance, consider referencing an Oklahoma Sample Letter for Insufficient Amount to Reinstate Loan to structure your message.

To write a letter of re-appeal, start by clearly stating your intention to appeal the decision. Include specific reasons why you believe the decision should be reconsidered, supported by relevant facts or evidence. Remember to conclude by requesting a prompt review of your appeal. Utilizing an Oklahoma Sample Letter for Insufficient Amount to Reinstate Loan can provide a helpful framework.

Begin your official letter of explanation by addressing the recipient with a proper greeting. In the body, briefly explain the purpose of your letter, highlighting relevant details. If applicable, reference the Oklahoma Sample Letter for Insufficient Amount to Reinstate Loan to illustrate your situation. Ensure the tone remains professional and respectful throughout the letter, and conclude with a clear call to action.

To write a letter explaining your financial situation, start by clearly stating your current circumstances. Include specific details about your income, expenses, and any challenges you face. Be honest and concise, and relate your situation to the use of an Oklahoma Sample Letter for Insufficient Amount to Reinstate Loan for clarity. This approach helps the recipient understand your position and the reason for your request.

When writing a denial appeal letter, begin by clearly identifying the original decision and the reasons for the denial. Reference the Oklahoma Sample Letter for Insufficient Amount to Reinstate Loan to craft a compelling argument. Include any new evidence that supports your case, and express your desire for a reevaluation of the situation. Close the letter respectfully, inviting further discussion or clarification.

To write a powerful appeal letter, start by clearly stating your purpose and including relevant details. Incorporate the Oklahoma Sample Letter for Insufficient Amount to Reinstate Loan as a guideline to establish your case effectively. Use a respectful tone, and ensure you provide all necessary documentation to support your claim. Finally, conclude with a strong closing statement that encourages a prompt response.