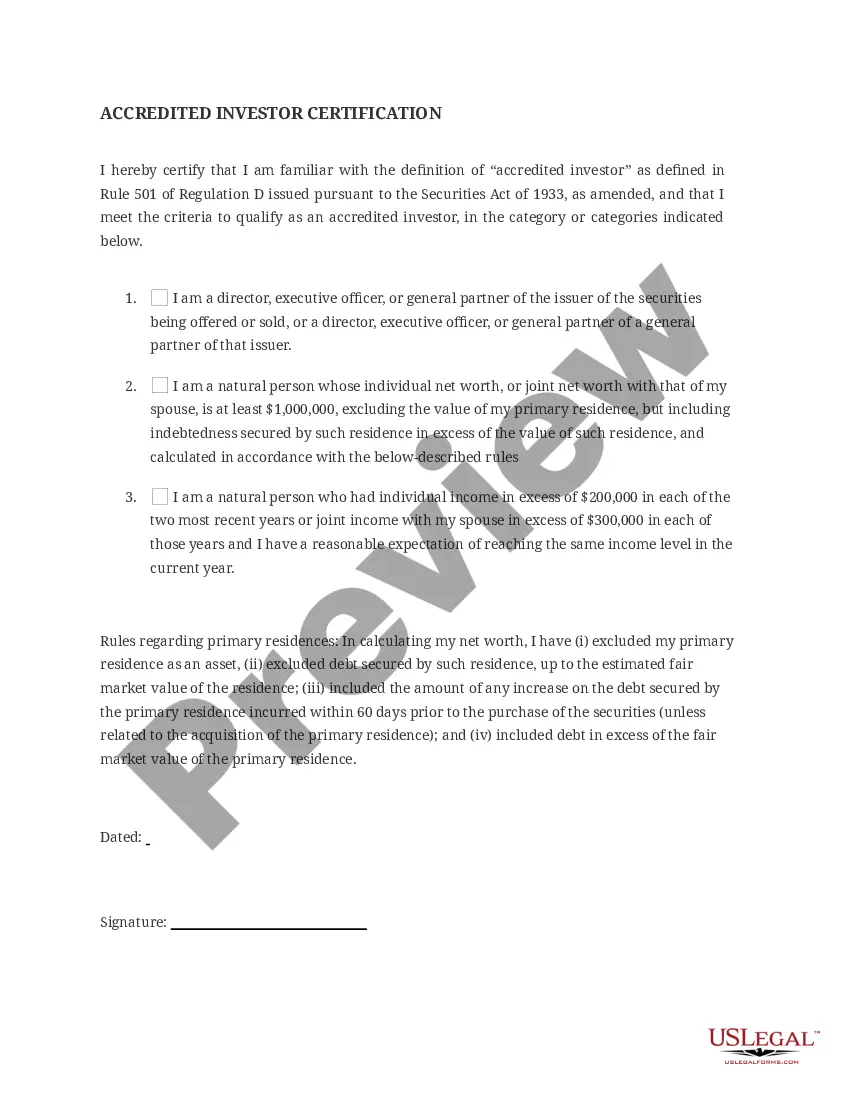

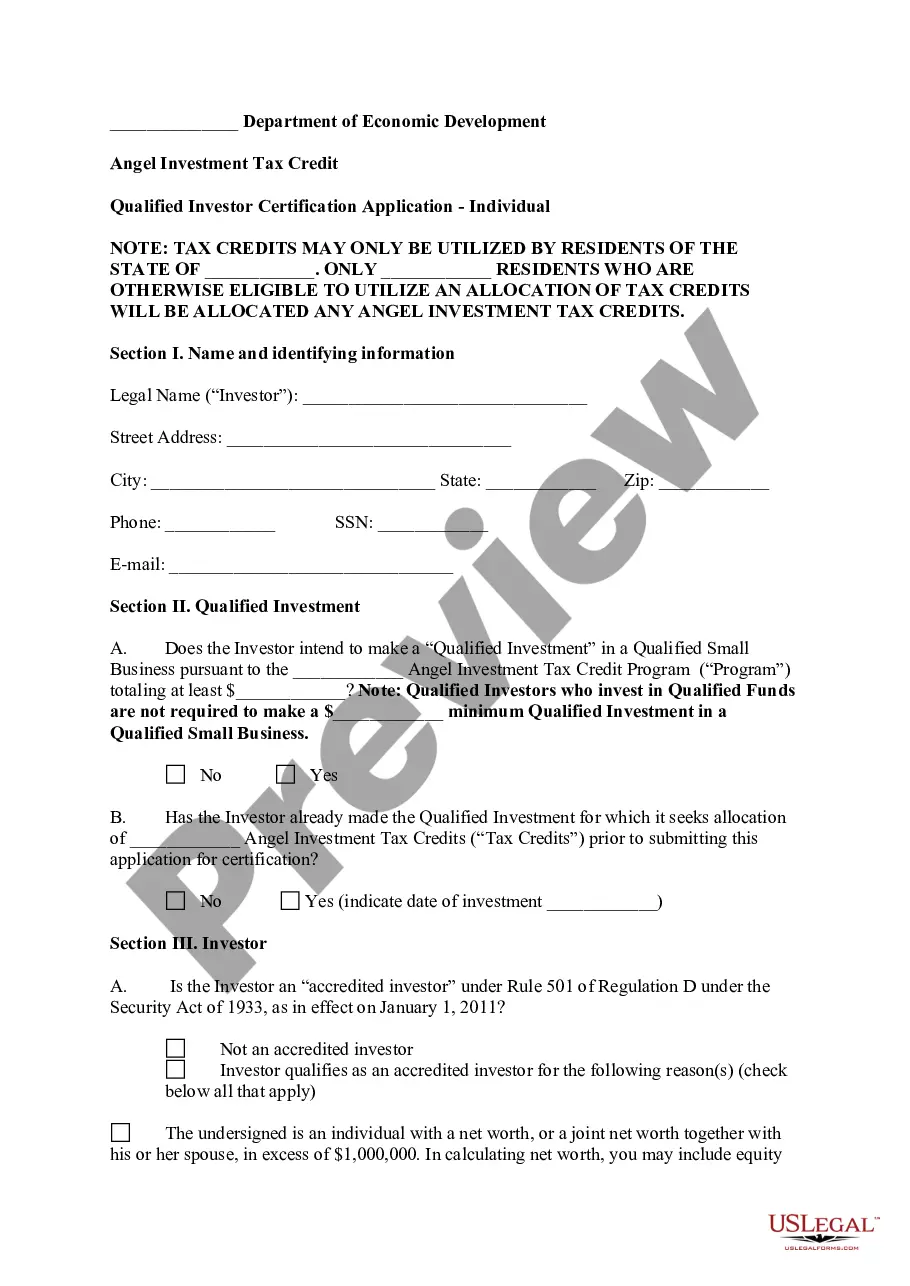

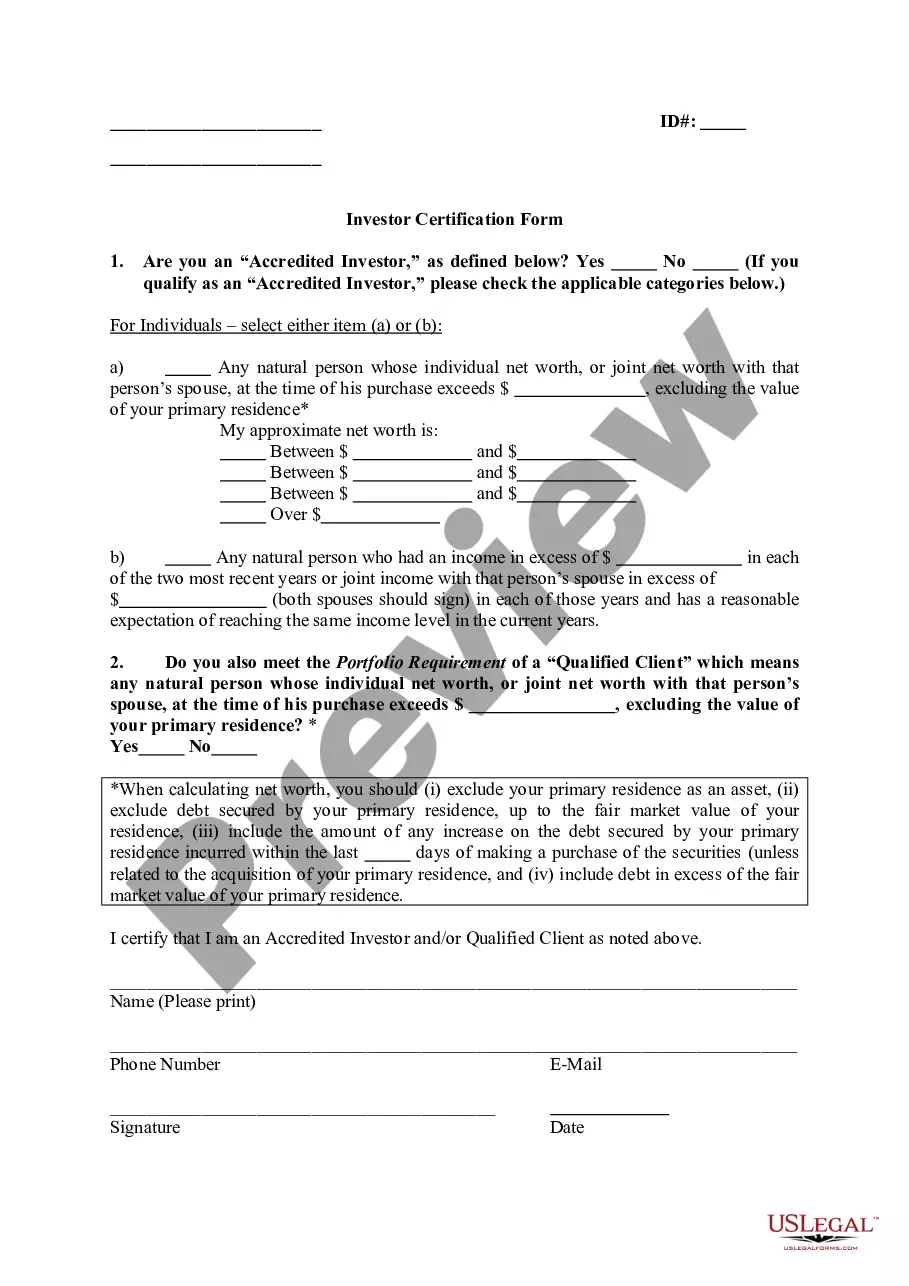

Under SEC law, a company that offers its own securities must register these investments with the SEC before it can sell them unless it meets an exception. One of those exceptions is selling unregistered investments to accredited investors.

To become an accredited investor the (SEC) requires certain wealth, income or knowledge requirements. The investor must fall into one of three categories. Firms selling unregistered securities must put investors through their own screening process to determine if investors can be considered an accredited investor.

The Verifying Individual or Entity should take reasonable steps to verify and determined that an Investor is an "accredited investor" as such term is defined in Rule 501 of the Securities Act, and hereby provides written confirmation. This letter serves to help the Entity determine status, take Investor statements regarding information, and waiver of claims.

Ohio Qualified Investor Certification and Waiver of Claims

State:

Multi-State

Control #:

US-ENTREP-0012-1

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Qualified Investor Certification And Waiver Of Claims?

If you wish to full, obtain, or print out lawful record themes, use US Legal Forms, the largest variety of lawful varieties, which can be found on the Internet. Utilize the site`s simple and hassle-free search to find the files you need. Various themes for business and personal functions are sorted by categories and claims, or search phrases. Use US Legal Forms to find the Ohio Qualified Investor Certification and Waiver of Claims in a couple of clicks.

When you are presently a US Legal Forms consumer, log in to your profile and click the Obtain button to get the Ohio Qualified Investor Certification and Waiver of Claims. Also you can gain access to varieties you earlier acquired from the My Forms tab of your profile.

Should you use US Legal Forms the very first time, follow the instructions listed below:

- Step 1. Ensure you have chosen the shape for the appropriate town/land.

- Step 2. Utilize the Review option to look over the form`s content. Do not forget to learn the description.

- Step 3. When you are not happy with the develop, utilize the Lookup industry near the top of the display screen to find other models in the lawful develop web template.

- Step 4. After you have identified the shape you need, go through the Acquire now button. Pick the pricing strategy you like and put your credentials to sign up for the profile.

- Step 5. Method the purchase. You can utilize your credit card or PayPal profile to complete the purchase.

- Step 6. Find the structure in the lawful develop and obtain it in your system.

- Step 7. Total, revise and print out or signal the Ohio Qualified Investor Certification and Waiver of Claims.

Every lawful record web template you purchase is the one you have forever. You have acces to every single develop you acquired in your acccount. Click the My Forms section and choose a develop to print out or obtain once again.

Be competitive and obtain, and print out the Ohio Qualified Investor Certification and Waiver of Claims with US Legal Forms. There are thousands of professional and condition-distinct varieties you can use for your business or personal needs.

Form popularity

FAQ

PTE tax allows an entity taxed as a partnership or S Corporation to make a tax payment on behalf of its partners. The business pays an elective tax of 9.3% of qualified net income to the Franchise Tax Board.

A qualifying pass-through entity (PTE) that is not a disregarded entity may make the election by filing the IT 4738 or by completing the Electing Pass-Through Entity Election Form on or before the filing deadline. An election made by one PTE is not binding on any other PTE. Each PTE must make its own election.

The Ohio refundable credit available to owners of electing pass-through entities for the proportionate share of tax levied on the IT 4738 is only available to a ?taxpayer,? which does not include a C corp. Therefore, a C corp cannot file a PTE return to claim this credit.

Who Should file the IT 1140? A qualifying PTE is required to file an IT 1140 when it is subject to withholding or entity tax on distributive shares of income issued to qualifying investors.

Electing PTEs are required to file estimated tax returns and make the following quarterly estimated tax payments: 1st-quarter payment of 22.5% of the PTE's estimated tax liability for the tax year. 2nd-quarter payment of 45% of the PTE's estimated tax liability for the tax year.

Payments may be remitted by EFT (ACH credit) via the Ohio Treasurer of State (TOS). Any questions about the EFT payment process should be directed to the Ohio Treasurer of State by calling (877)338-6446.

In Ohio, individuals must add back the PTE tax as being paid. On the Ohio Individual Income Tax Form, you are required to add back any Ohio state entity taxes you took as a deduction at the federal level. The taxpayer will receive a dollar-for-dollar pro-rata tax credit for taxes paid by the entity.

Individual income tax Allows an Ohio resident a tax credit for pass-through entity (PTE) taxes paid to other states. Taxpayers have to add back PTE taxes paid to other states and deducted from an individual's federal adjusted gross income in determining the taxpayer's Ohio adjusted gross income.