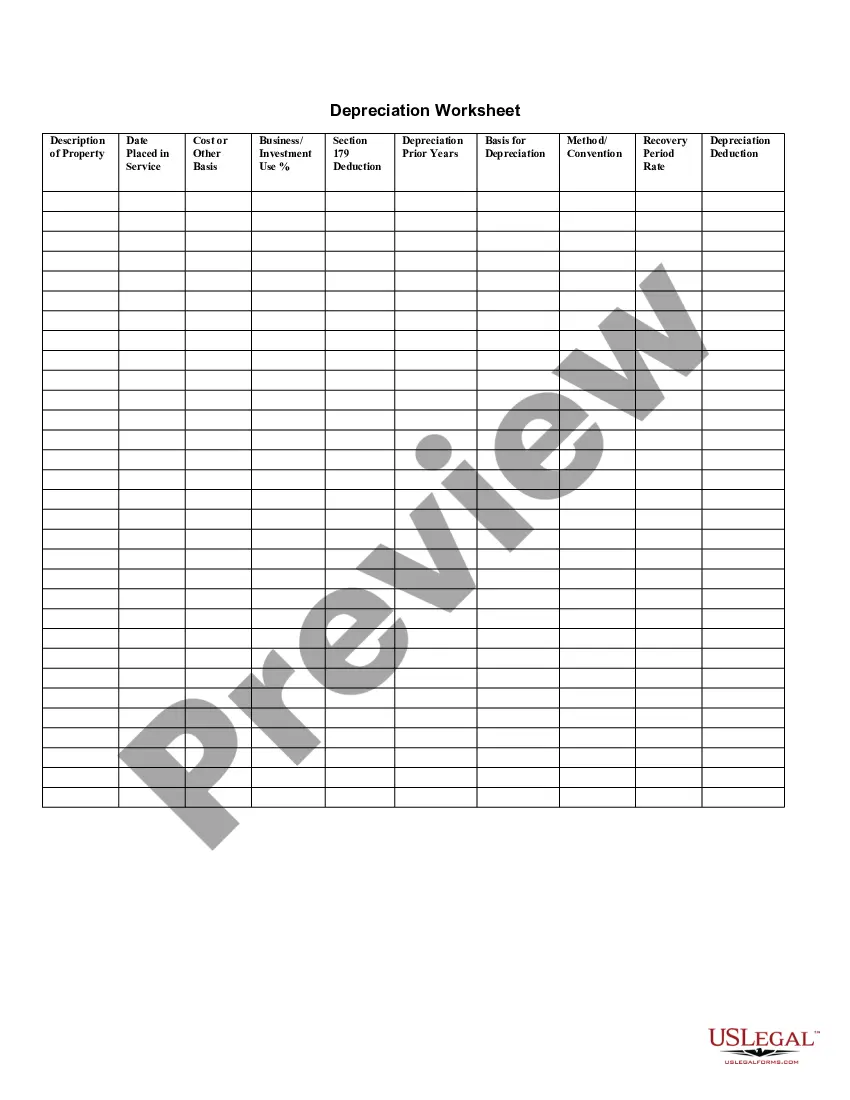

Ohio Depreciation Schedule

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Depreciation Schedule?

Selecting the appropriate authorized document template can be a challenge.

Of course, there are numerous layouts accessible online, but how can you locate the legal form you need.

Utilize the US Legal Forms website. The platform offers thousands of layouts, including the Ohio Depreciation Schedule, suitable for business and personal requirements.

If the form does not meet your requirements, use the Search field to find the correct form. Once you are confident the form is appropriate, click the Get now button to acquire the form. Choose the pricing plan you wish and provide the necessary information. Create your account and place an order using your PayPal account or Visa/Mastercard. Select the file format and download the authorized document template to your device. Complete, edit, print, and sign the acquired Ohio Depreciation Schedule. US Legal Forms is the largest collection of legal forms where you can find numerous document layouts. Take advantage of the service to download professionally crafted documents that meet state regulations.

- All forms are validated by experts and comply with federal and state regulations.

- If you are already registered, Log In to your account and click the Acquire button to obtain the Ohio Depreciation Schedule.

- Use your account to review all the legal forms you have purchased previously.

- Navigate to the My documents section of your account and get another copy of the document you desire.

- If you are a new user of US Legal Forms, here are simple instructions to follow.

- First, ensure you have selected the correct form for your locality/region. You can preview the form using the Preview button and read the form description to verify it is suitable for you.

Form popularity

FAQ

§179 and A§168(k) depreciation expenses, Ohio requires taxpayers to add back certain amounts of accelerated depreciation expense in the year they are allowed by I.R.C. A§179 and A§168(k). Ohio then allows the taxpayer to deduct those amounts more gradually over a period of years.

The portion of the business standard mileage rate that is treated as depreciation will be 27 cents per mile for 2020, 1 cent more than 2019, one of the few amounts that is increasing.

Ohio law still prohibits a taxpayer from taking a bonus depreciation deduction for a taxable year if the taxpayer's FAGI for that year was a net operating loss or if the taxpayer's FAGI was reduced by an NOL carryforward or carryback.

5/6 of their depreciation expense in a given tax year should deduct 1/5 of the amount added back in the subsequent five years; 2/3 of their depreciation expense in a given tax year (because of a 10% increase in Ohio employer withholding) should deduct 1/2 of the amount added back in the subsequent two years; OR.

Equipment is considered a capital asset. You can deduct the cost of a capital asset, but not all at once. The general rule is that you depreciate the asset by deducting a portion of the cost on your tax return over several years. See Question 15 for an exception to this general rule.

You generally can't deduct in one year the entire cost of property you acquired, produced, or improved and placed in service for use either in your trade or business or income-producing activity if the property is a capital expenditure. Instead, you generally must depreciate such property.

Generally, Ohio's income tax begins with federal adjusted gross income. However, in order to smooth the revenue impact of accelerated I.R.C. §179 and A§168(k) depreciation expenses, Ohio requires taxpayers to add back certain amounts of accelerated depreciation expense in the year they are allowed by I.R.C.

The states listed as conforming to the TCJA bonus depreciation rules allow for the 100% deduction of qualified property....States that have adopted the new bonus depreciation rules:Alabama.Alaska.Colorado.Delaware.Illinois.Kansas.Louisiana.Michigan.More items...

For tax years 2015 through 2017, first-year bonus depreciation was set at 50%. It was scheduled to go down to 40% in 2018 and 30% in 2019, and then not be available in 2020 and beyond. The Tax Cuts and Jobs Act, enacted at the end of 2018, increases first-year bonus depreciation to 100%.

Depreciation is calculated each year for tax purposes. The most common depreciation is called straight-line depreciation, taking the same amount of depreciation in each year of the asset's useful life.