Ohio Grantor Retained Annuity Trust

Description

How to fill out Grantor Retained Annuity Trust?

Locating the appropriate valid document design can be a challenge.

Of course, there are numerous templates accessible on the web, but how can you find the valid version you require.

Utilize the US Legal Forms platform. The service provides thousands of templates, such as the Ohio Grantor Retained Annuity Trust, suitable for business and personal needs.

You can review the form using the Review button and examine the form description to confirm it is indeed suitable for your needs.

- All documents are reviewed by experts and comply with state and federal regulations.

- If you are already a member, Log In to your account and then click the Download button to acquire the Ohio Grantor Retained Annuity Trust.

- Use your account to browse the legitimate documents you have previously ordered.

- Visit the My documents section of your account and download another copy of the document you require.

- If you are a new user of US Legal Forms, here are simple steps you should follow.

- First, ensure you have selected the correct form for your locality.

Form popularity

FAQ

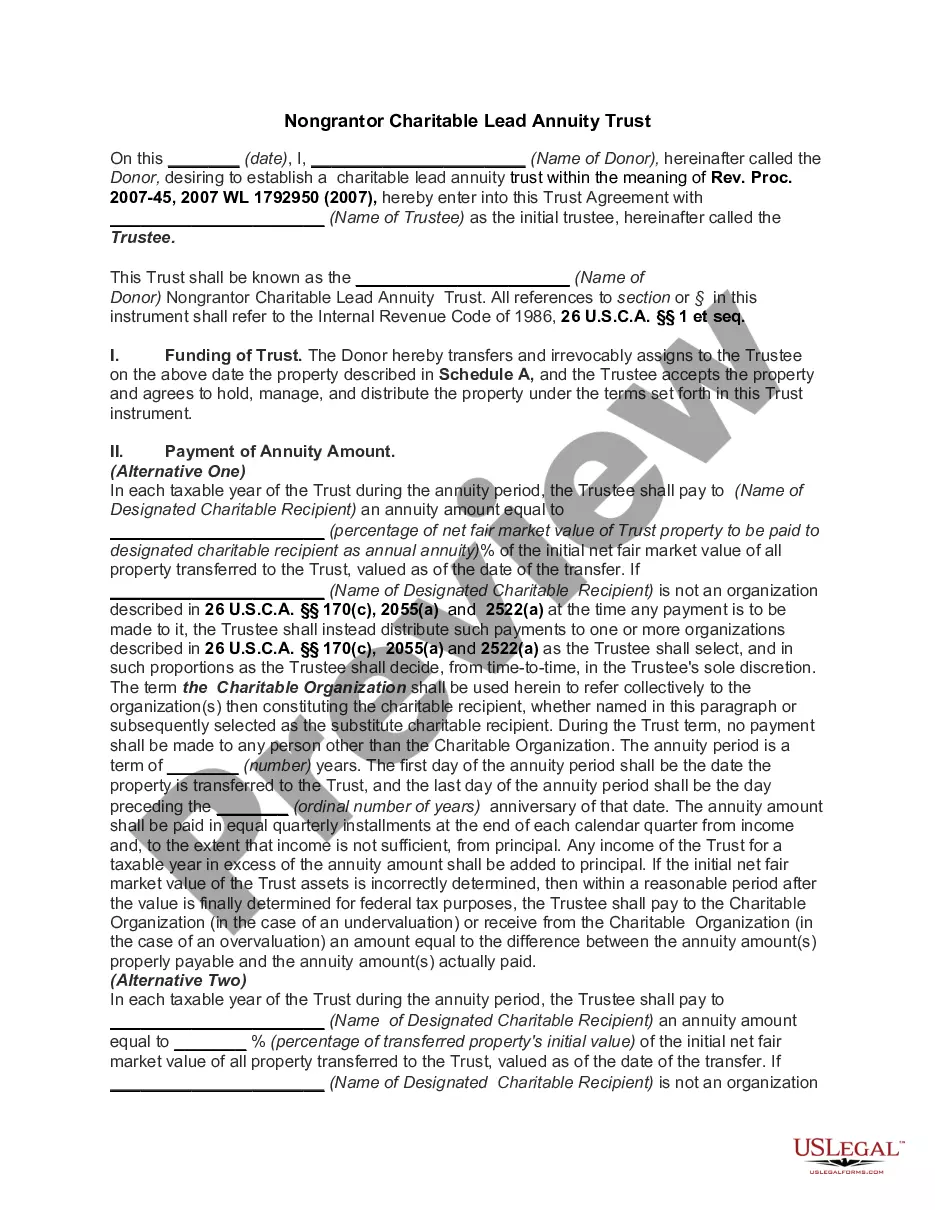

Grantor Retained Income Trust, Definition A grantor retained income trust allows the person who creates the trust to transfer assets to it while still being able to receive net income from trust assets. The grantor maintains this right for a fixed number of years.

Grantor retained annuity trusts (GRAT) are estate planning instruments in which a grantor locks assets in a trust from which they earn annual income. Upon expiry, the beneficiary receives the assets with minimal or no gift tax liability. GRATS are used by wealthy individuals to minimize tax liabilities.

A GRAT is an irrevocable trust, and when you transfer property to the GRAT, you are making a taxable gift to your beneficiaries.

GRATs are taxed in two ways: Any income you earn from the appreciation of your assets in the trust is subject to regular income tax, and any remaining funds/assets that transfer to a beneficiary are subject to gift taxes.

Like a GRAT, an IDGT is an irrevocable trust. Unlike a GRAT, the grantor typically sells assets to the trust rather than gifting them, in order to avoid triggering gift tax. Assets sold to an IDGT are not considered to give rise to a capital gain, which means that no capital gains tax is owed.

With respect to income taxes, the grantor is treated as the owner of the assets during the GRAT term and reports all income earned by the GRAT on his individual income tax return. To avoid having to file its own fiduciary income tax return, the GRAT should not apply for a separate taxpayer identification number.

To implement this strategy, you zero out the grantor retained annuity trust by accepting combined payments that are equal to the entire value of the trust, including the anticipated appreciation. In theory, there would be nothing left for the beneficiary if the trust is really zeroed out.

Since a GRAT is a grantor trust for income tax purposes, you will report the trust's taxable income and deductions on your personal income tax return as if you still owned the trust assets directly. A grantor trust is disregarded for income tax purposes and will not pay taxes.

Beneficiaries of a trust typically pay taxes on the distributions they receive from the trust's income, rather than the trust itself paying the tax. However, such beneficiaries are not subject to taxes on distributions from the trust's principal.

Tax Implications of the GRAT During the term of the GRAT, the Donor will be taxed on all of the income and capital gains earned by the trust, without regard to the amount of the annuity paid to the Donor.