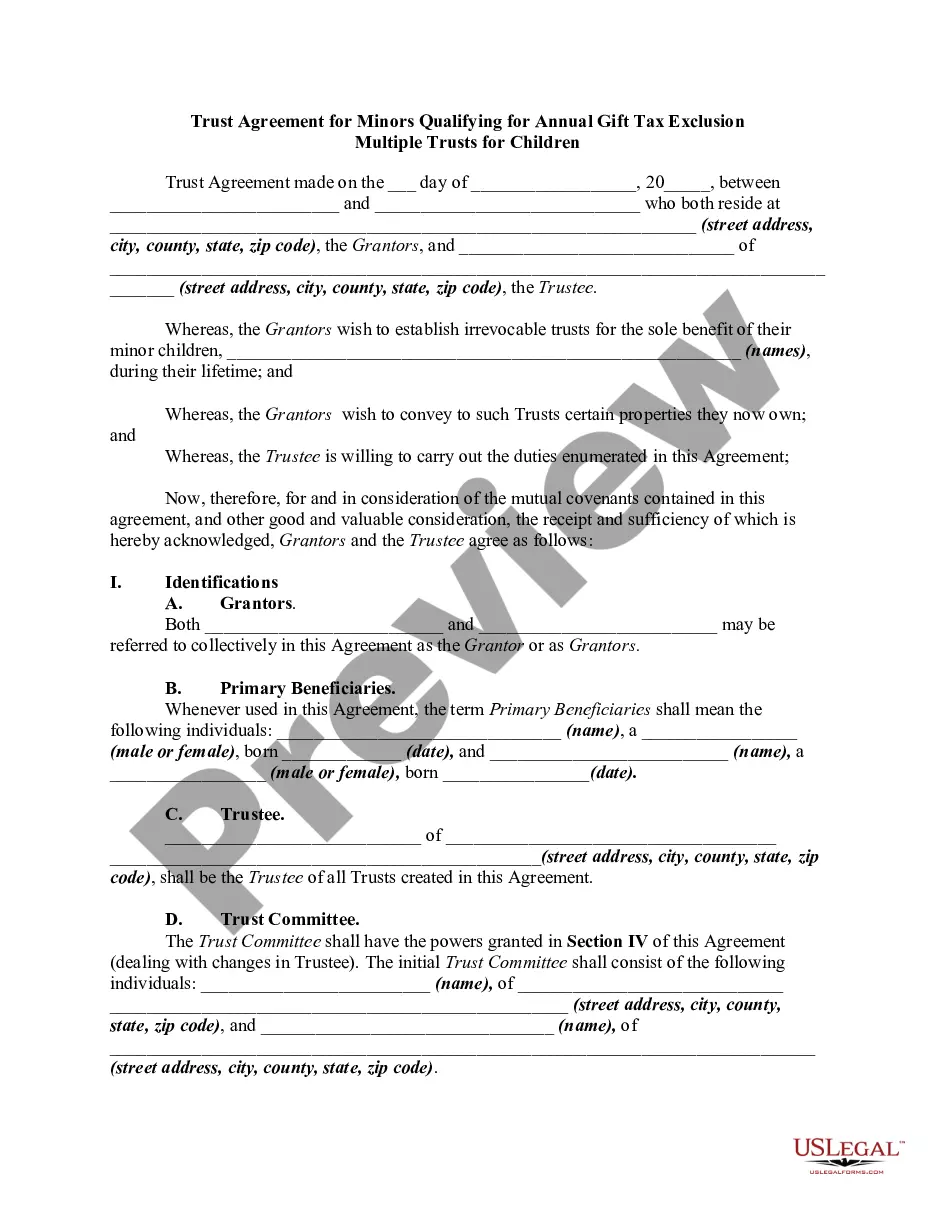

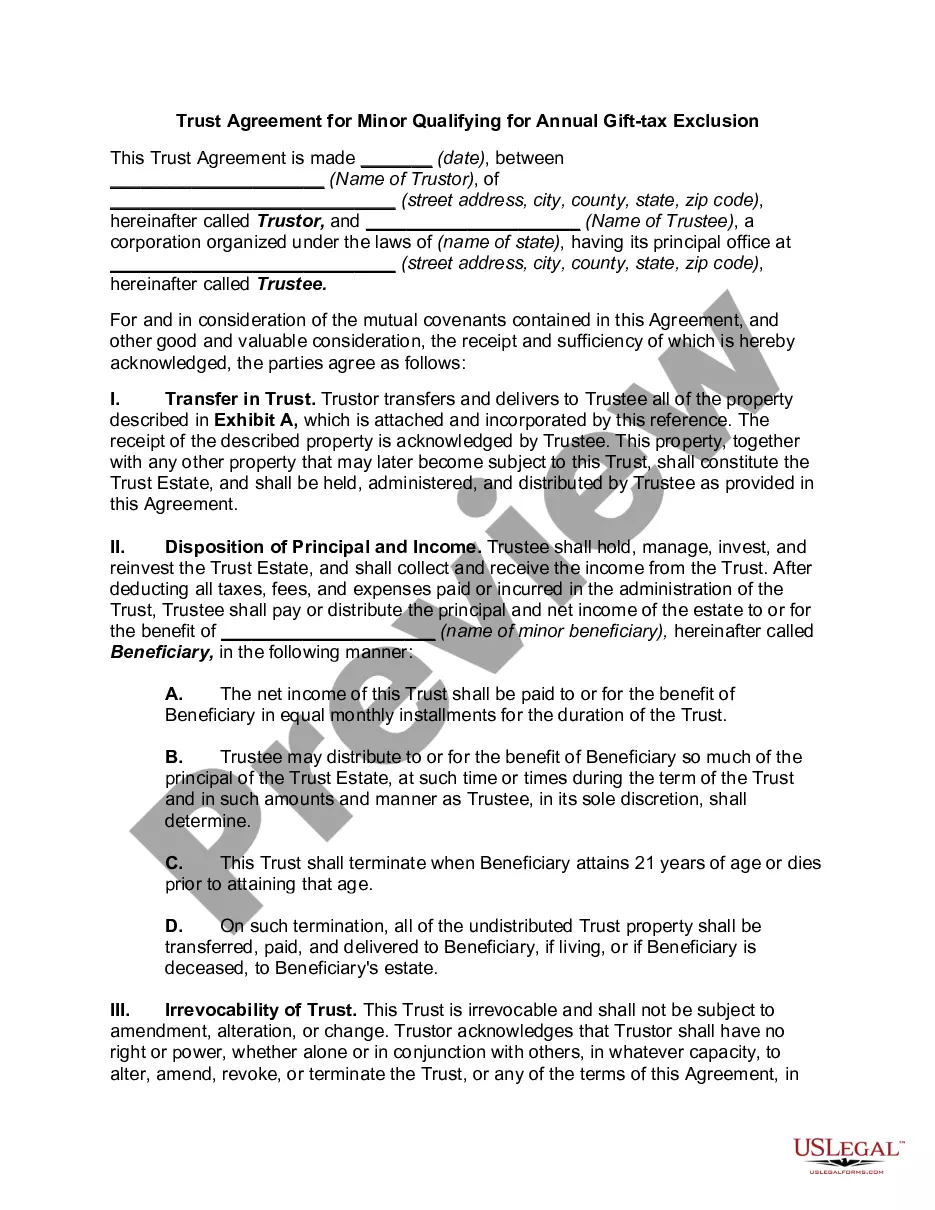

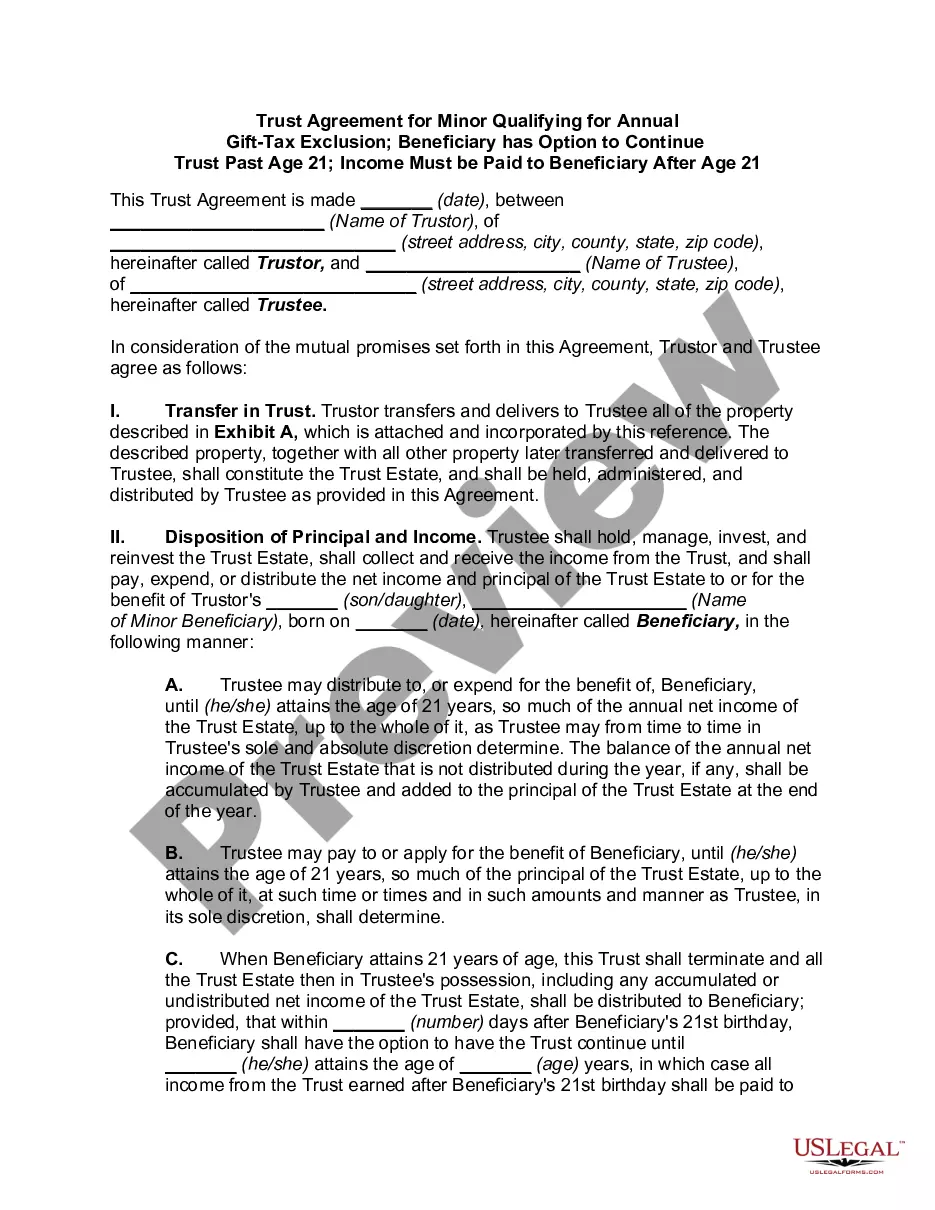

Ohio General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion

Description

How to fill out General Form Of Trust Agreement For Minor Qualifying For Annual Gift Tax Exclusion?

Locating the appropriate sanctioned document format could be a challenge.

It goes without saying, there are numerous templates available online, but how can you discover the official document you need.

Utilize the US Legal Forms website. The platform provides an extensive selection of templates, such as the Ohio General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion, which you can use for both business and personal purposes.

You can review the form using the Review button and read the form description to confirm it is suitable for you.

- All of the forms are reviewed by experts and comply with state and federal regulations.

- If you are currently registered, Log In to your account and click the Download button to access the Ohio General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion.

- Use your account to browse the legal forms you have previously purchased.

- Visit the My documents section of your account and retrieve another copy of the document you require.

- If you are a new user of US Legal Forms, here are simple instructions to follow.

- First, ensure you have selected the correct form for your city/region.

Form popularity

FAQ

A gift made during the creation of a Grantor Retained Annuity Trust (GRAT) may qualify for the annual exclusion if it meets certain criteria. Generally, if the gift involves making a present interest in the trust available to the beneficiaries, it may be eligible. The Ohio General Form of Trust Agreement for Minor Qualifying for Annual Gift Tax Exclusion can provide guidance in structuring this type of gift.

A gift in trust is a way to avoid taxes on gifts that exceed the annual gift tax exclusion amount. One type of gift in trust is a Crummey trust, which allows gifts to be given for a specific period, establishing the gifts as a present interest and eligible for the gift tax exclusion.

A Section 2503(c) trust allows all the principal and income to be used for the child until he reaches the age of 21, unlike the 2503(b) trust that extends beyond age 21 and requires income to be paid to the child annually. The trustee can pay the child's college expenses from the 2503(c) trust.

The key difference between a 2503(c) trust and a 2503(b) trust is the distribution requirement. Parents who are concerned about providing a child or other beneficiary with access to trust funds at age 21 might be better off with a 2503(b), since there is no requirement for access at age 21.

A gift in trust is a way to avoid taxes on gifts that exceed the annual gift tax exclusion amount. One type of gift in trust is a Crummey trust, which allows gifts to be given for a specific period, establishing the gifts as a present interest and eligible for the gift tax exclusion.

The federal gift tax law provides that every person can give a present interest gift of up to $14,000 each year to any individual they want.

Section 2503(b) is also known as a Qualifying Minor's Trust or Mandatory Income Trust. This is an irrevocable trust which requires distribution of income on an annual basis. Most often, distributed funds are placed into a custodial bank account until the child reaches legal age.

Present And Future InterestThe IRS does not levy gift taxes on trusts, nor does it consider payments from the trust to a beneficiary as a gift (it may be taxable income to the beneficiary, however).

Gifts in trust do not qualify for the annual exclusion unless the trust either qualifies as a Minor's Trust under Internal Revenue Code Section 2503(c) or has certain temporary withdrawal powers called Crummey powers.

Gifts in trust do not qualify for the annual exclusion unless the trust either qualifies as a Minor's Trust under Internal Revenue Code Section 2503(c) or has certain temporary withdrawal powers called Crummey powers.