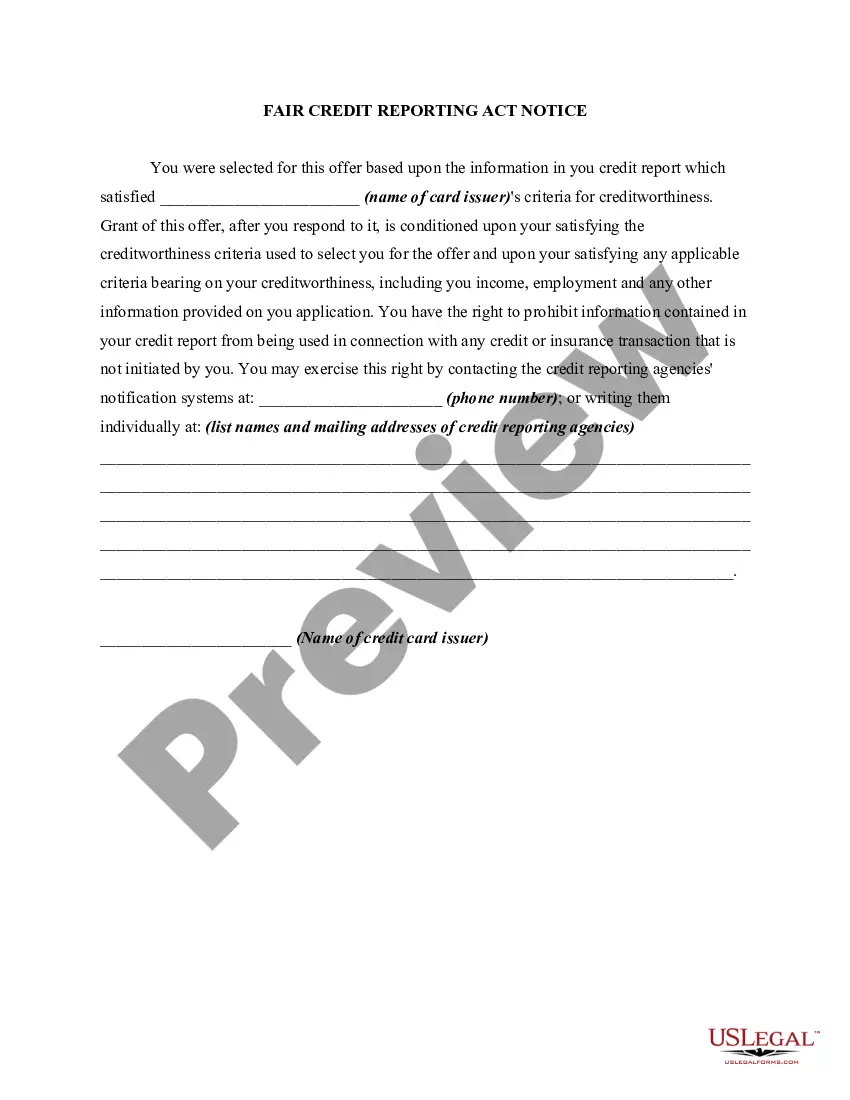

Whenever credit for personal, family, or household purposes involving a consumer is denied or the charge for the credit is increased either wholly or partly because of information obtained from a person other than a credit reporting agency bearing on the consumer's creditworthiness, credit standing, credit capacity, character, general reputation, personal characteristics, or mode of living, certain requirements must be met. The user of such information, when the adverse action is communicated to the consumer, must clearly and accurately disclose the consumer's right to make a written request for disclosure of the information. If such a request is made and is received within 60 days after the consumer learned of the adverse action, the user, within a reasonable period of time, must disclose to the consumer the nature of the information.

New York Notice of Increase in Charge for Credit Based on Information Received From Person Other Than Consumer Reporting Agency

Description

How to fill out Notice Of Increase In Charge For Credit Based On Information Received From Person Other Than Consumer Reporting Agency?

If you want to complete, down load, or print legal file themes, use US Legal Forms, the most important collection of legal varieties, which can be found on the Internet. Take advantage of the site`s basic and handy search to get the papers you will need. A variety of themes for enterprise and person purposes are categorized by classes and claims, or search phrases. Use US Legal Forms to get the New York Notice of Increase in Charge for Credit Based on Information Received From Person Other Than Consumer Reporting Agency in just a handful of click throughs.

In case you are currently a US Legal Forms buyer, log in to your bank account and then click the Obtain option to obtain the New York Notice of Increase in Charge for Credit Based on Information Received From Person Other Than Consumer Reporting Agency. You may also access varieties you previously saved in the My Forms tab of your bank account.

Should you use US Legal Forms the very first time, follow the instructions listed below:

- Step 1. Be sure you have chosen the shape for the correct town/nation.

- Step 2. Utilize the Review solution to look through the form`s articles. Never forget about to read through the description.

- Step 3. In case you are not happy using the kind, utilize the Search discipline at the top of the monitor to find other variations of your legal kind design.

- Step 4. After you have found the shape you will need, select the Acquire now option. Pick the prices strategy you like and put your references to register for the bank account.

- Step 5. Method the deal. You can utilize your bank card or PayPal bank account to accomplish the deal.

- Step 6. Choose the file format of your legal kind and down load it in your product.

- Step 7. Total, change and print or indicator the New York Notice of Increase in Charge for Credit Based on Information Received From Person Other Than Consumer Reporting Agency.

Each legal file design you acquire is your own permanently. You may have acces to every kind you saved with your acccount. Select the My Forms segment and pick a kind to print or down load once more.

Compete and down load, and print the New York Notice of Increase in Charge for Credit Based on Information Received From Person Other Than Consumer Reporting Agency with US Legal Forms. There are many skilled and status-certain varieties you may use for your personal enterprise or person requires.

Form popularity

FAQ

The Consumer Credit Fairness Act of 2021 ? which was signed into law last November ? will go into effect next month and reduces the statute of limitations for consumer debt collection from six years to three years.

Section 605(h)(1) of the Fair Credit Reporting Act requires that, when providing a consumer report to a person that requests the report (a user), a nationwide consumer reporting agency (NCRA) must provide a notice of address discrepancy to the user if the address provided by the user in its request ?substantially ...

Statute of Limitations in New York Thanks to a law passed in 2021, the statute of limitations of debt in New York is three years, which means that's how much time a debt collector has to file a lawsuit to recover the debt through the court system.

The Consumer Credit Fairness Act requires plaintiffs to file certain affidavits when seeking a default judgment in any consumer debt case as follows: If the plaintiff is the original creditor, the application MUST include an Affidavit of Facts by Original Creditor [UCS-CCR3].

Effective April 7, 2022, the New York statute of limitations for debt collection lawsuits arising out of a consumer credit transaction is reduced from six years to three years. Also, payment toward the debt or written or oral affirmation of the debt by the consumer does not revive or extend the limitations period.

Enacts the New York privacy act to require companies to disclose their methods of de-identifying personal information, to place special safeguards around data sharing and to allow consumers to obtain the names of all entities with whom their information is shared.

Thus, under the FCRA, certain consumer information will be subject to two opt-out notices, a sharing opt-out notice (Section 603(d)) and a marketing use opt-out notice (Section 624). These two opt-out notices may be consolidated. Federal Register to implement this section (72 FR 62910).

What Is the New York Fair Debt Collection Practices Act? New York's version of the FDCPA (sometimes referred to as the New York Debt Collection Procedures Act) is similar to the federal FDCPA. Congress passed the FDCPA back in 1978 to stop abusive debt collection practices used by certain debt collectors.