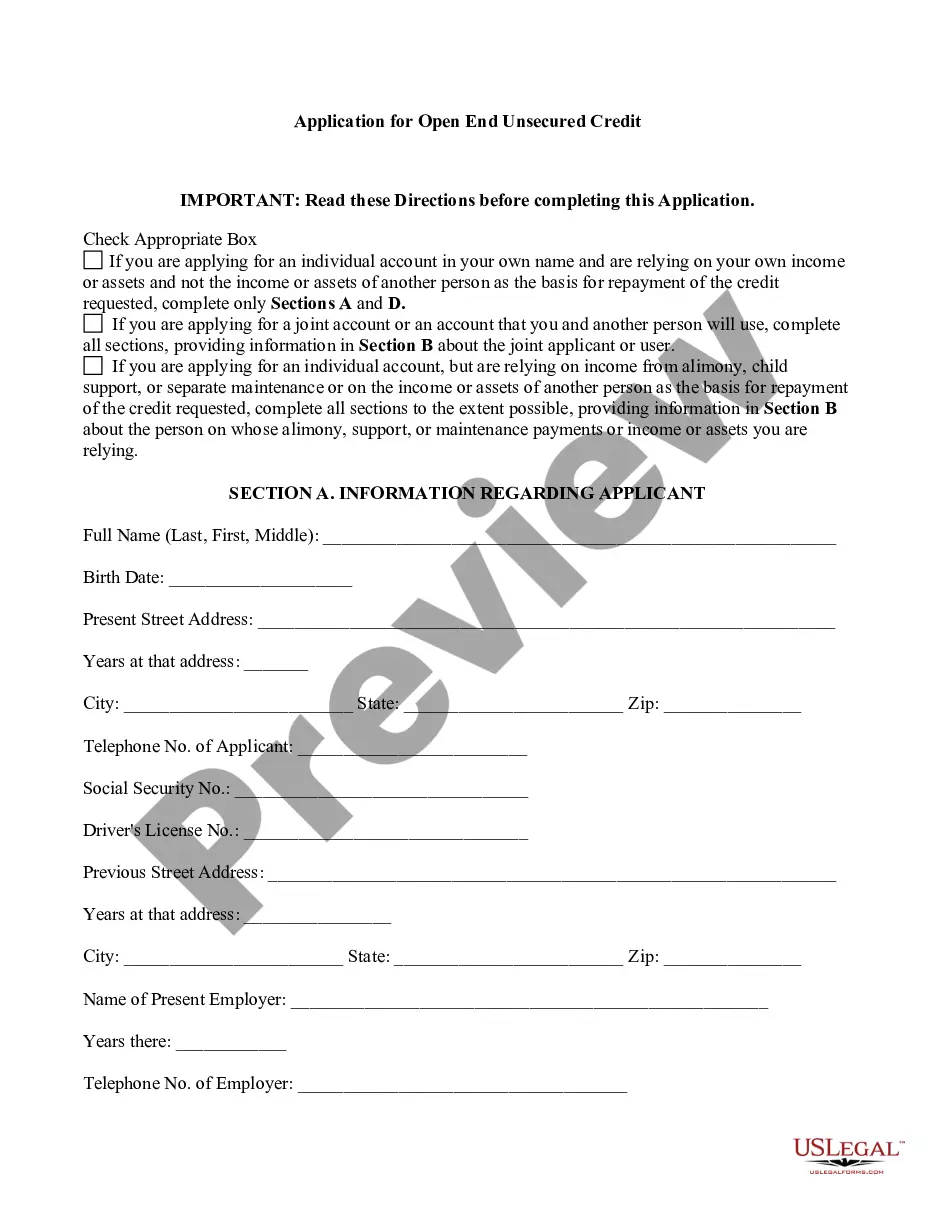

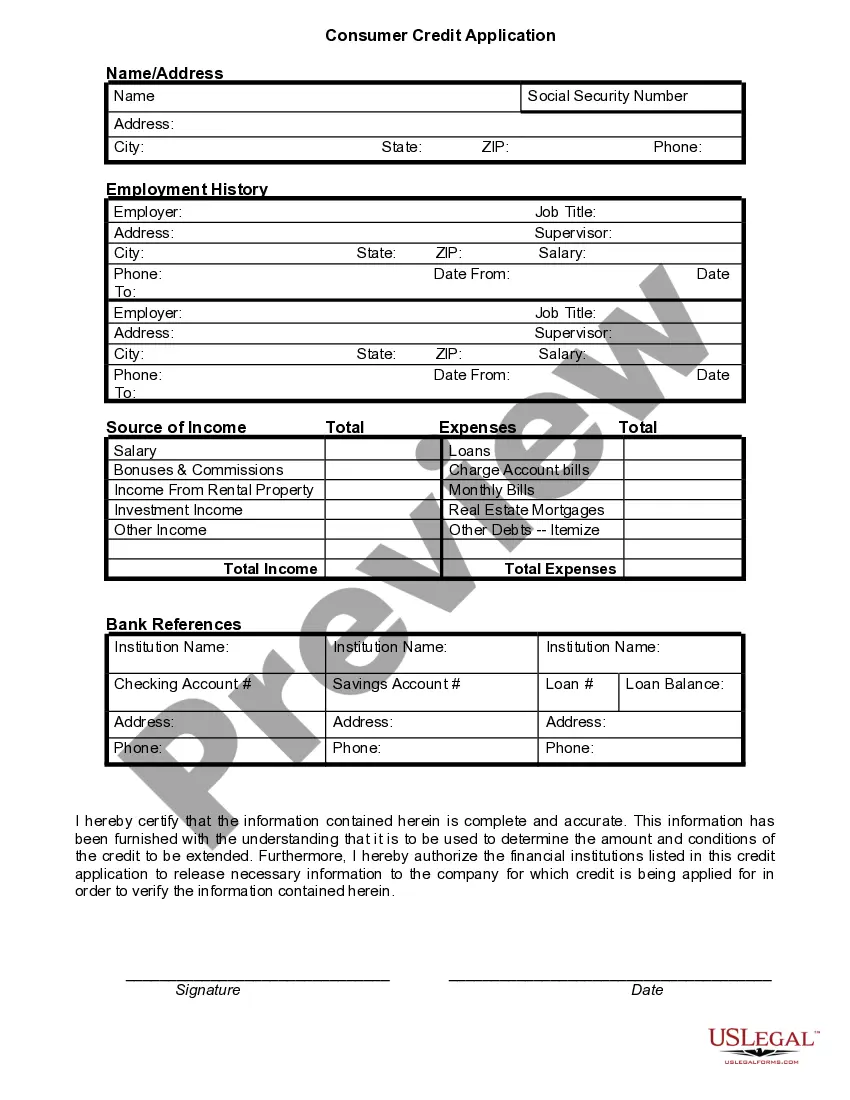

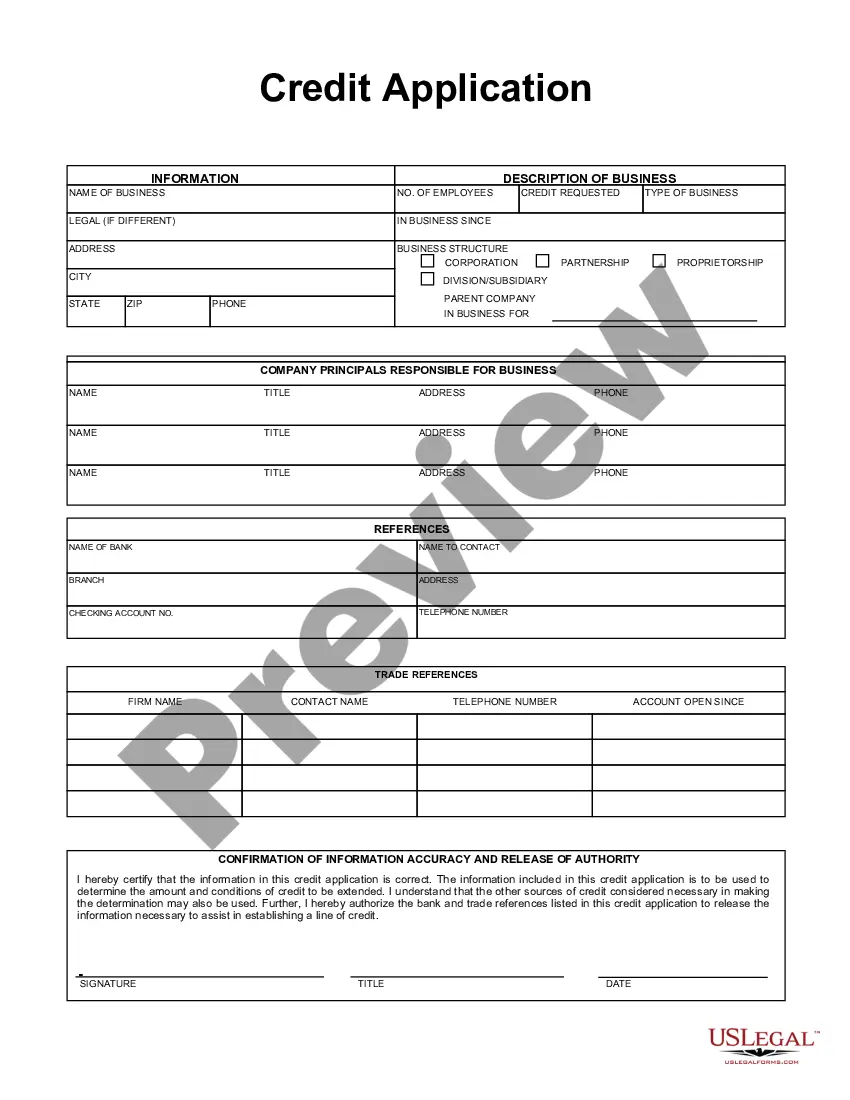

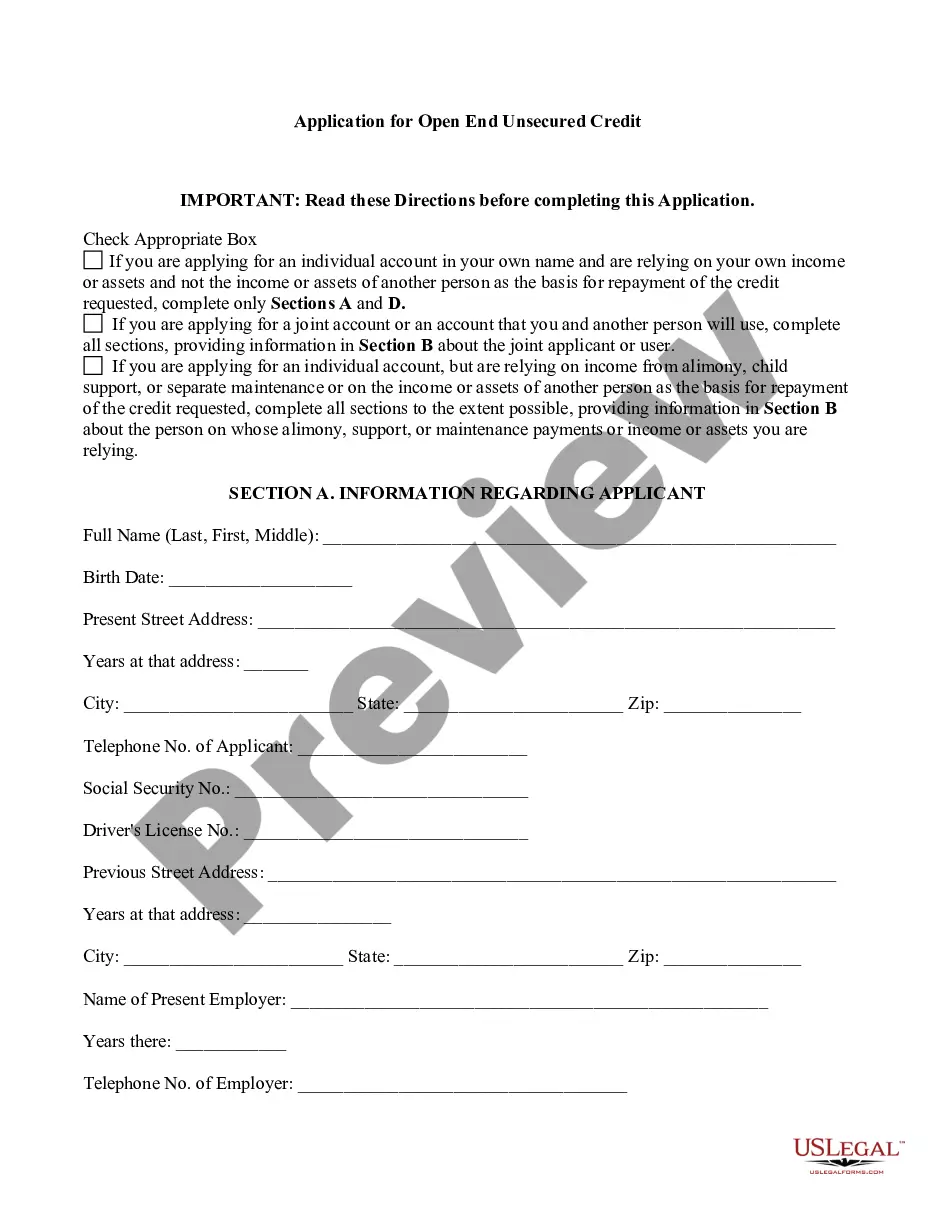

Nevada Credit Card Application for Unsecured Open End Credit

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Credit Card Application For Unsecured Open End Credit?

If you want to total, download, or print out authorized record layouts, use US Legal Forms, the largest selection of authorized forms, that can be found online. Use the site`s simple and easy convenient research to find the files you will need. Various layouts for company and individual purposes are categorized by groups and suggests, or keywords and phrases. Use US Legal Forms to find the Nevada Credit Card Application for Unsecured Open End Credit within a couple of click throughs.

Should you be previously a US Legal Forms client, log in for your accounts and click on the Obtain key to have the Nevada Credit Card Application for Unsecured Open End Credit. You can also access forms you previously delivered electronically within the My Forms tab of your accounts.

If you are using US Legal Forms the very first time, follow the instructions listed below:

- Step 1. Be sure you have chosen the form to the appropriate town/country.

- Step 2. Make use of the Review method to check out the form`s information. Never overlook to read the explanation.

- Step 3. Should you be not satisfied together with the type, make use of the Lookup industry on top of the screen to get other versions from the authorized type web template.

- Step 4. After you have located the form you will need, select the Purchase now key. Select the costs program you prefer and add your accreditations to register for the accounts.

- Step 5. Approach the purchase. You may use your credit card or PayPal accounts to accomplish the purchase.

- Step 6. Pick the format from the authorized type and download it on your system.

- Step 7. Complete, change and print out or signal the Nevada Credit Card Application for Unsecured Open End Credit.

Every authorized record web template you buy is your own property for a long time. You have acces to each type you delivered electronically in your acccount. Go through the My Forms section and select a type to print out or download again.

Remain competitive and download, and print out the Nevada Credit Card Application for Unsecured Open End Credit with US Legal Forms. There are many professional and state-certain forms you can use for your company or individual needs.

Form popularity

FAQ

Best Personal Lines of Credit at a Glance Line of CreditTypeAmountU.S. Bank Personal Line of CreditUnsecuredUp to $25,000TD Bank Personal Unsecured Line of CreditUnsecured$2,000-$50,000Regions Bank Preferred Line of CreditUnsecured$500-$50,000Regions Bank Credit LineUnsecured$500-$3,0003 more rows

Borrow from $2,500 - $25,000.

How to get an unsecured line of credit online Understand Your Credit and Income Qualifications. ... Review Unsecured Line of Credit Providers. ... Submit Your Online Line of Credit Application. ... Know Your Line of Credit Terms. ... Use What You Need. ... Repay on Time.

Credit card accounts, home equity lines of credit (HELOC), and debit cards are all common examples of open-end credit (though some, like the HELOC, have finite payback periods). The issuing bank allows the consumer to utilize borrowed funds in exchange for the promise to repay any debt in a timely manner.

The most common form of open-end credit is a credit card account. In this form of open-end credit, a credit limit is established and you may charge purchases up to that amount.

If you've ever used a credit card before, you are using what is called "open-end credit." Open-end credit is the idea that you get to withdraw funds up until a certain limit and as you repay it back, the funds are available to you again (also known as revolving credit).

Open-end credit is a loan from a bank or other financial institution that the borrower can draw on repeatedly, up to a certain pre-approved amount, and that has no fixed end date for full repayment. Open-end credit is also referred to as revolving credit. Credit cards are one common example.

While all lenders have their own requirements as to what credit scores they want their applicants to have for a line of credit, it's a good bet that some lenders will approve applicants with scores that hover around 660 to 712, which qualifies as a Fair score.

You'll typically need to have a minimum credit score of 600 or higher to qualify for an unsecured business line of credit. Although online lenders may accept bad or fair credit scores, banks will likely require good credit. Annual revenue. Most lenders have a minimum monthly or annual revenue requirement.

With open-end credit, you receive a credit line with a limit that you can draw from as needed, only paying interest on what you borrow. Common examples of open-end credit are credit cards and lines of credit. As you repay what you've borrowed, you can draw from the credit line again and again.