New Mexico Assignment of Life Insurance as Collateral

Description

How to fill out Assignment Of Life Insurance As Collateral?

US Legal Forms - one of several most significant libraries of lawful types in America - delivers a variety of lawful papers templates it is possible to down load or produce. Making use of the site, you can get thousands of types for company and individual purposes, categorized by categories, states, or keywords.You can find the most recent types of types just like the New Mexico Assignment of Life Insurance as Collateral within minutes.

If you already have a registration, log in and down load New Mexico Assignment of Life Insurance as Collateral from your US Legal Forms collection. The Obtain option will show up on every kind you perspective. You gain access to all formerly saved types inside the My Forms tab of your respective accounts.

If you want to use US Legal Forms the very first time, listed here are simple recommendations to obtain started:

- Be sure you have chosen the proper kind for the area/region. Click the Review option to analyze the form`s content. Read the kind outline to actually have selected the right kind.

- If the kind does not match your specifications, use the Look for industry towards the top of the display screen to discover the one that does.

- If you are happy with the shape, validate your decision by clicking the Acquire now option. Then, opt for the prices program you prefer and supply your qualifications to sign up for the accounts.

- Process the transaction. Make use of bank card or PayPal accounts to accomplish the transaction.

- Pick the format and down load the shape on your own system.

- Make adjustments. Fill up, edit and produce and indication the saved New Mexico Assignment of Life Insurance as Collateral.

Each and every web template you included with your account lacks an expiration date which is your own property permanently. So, if you want to down load or produce one more copy, just check out the My Forms area and click in the kind you will need.

Obtain access to the New Mexico Assignment of Life Insurance as Collateral with US Legal Forms, the most substantial collection of lawful papers templates. Use thousands of skilled and express-particular templates that meet up with your organization or individual demands and specifications.

Form popularity

FAQ

Can you cash out term life insurance? Since a term life insurance policy doesn't come with a cash value component, it's not possible to cash it out. This policy solely includes a death benefit that your beneficiaries may receive if you die before the end of the policy's term.

Only permanent policies can build cash value. Term life insurance is typically less expensive, but it does not build cash.

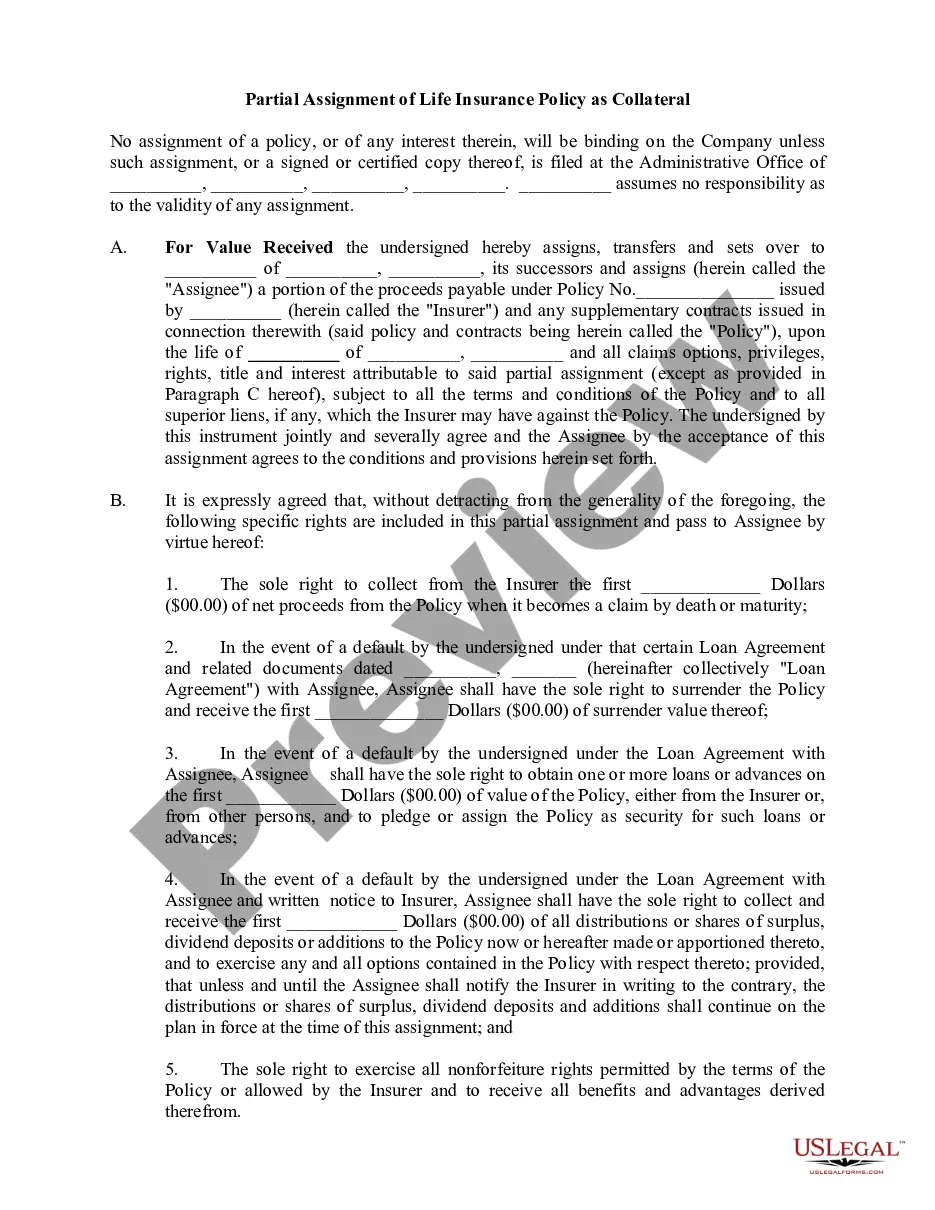

You can use either term or whole life insurance policy as collateral, but the death benefit must meet the lender's terms. Alternately, the policy owner's access to the cash value is restricted to protect the collateral.

The collateral assignment is irrevocable as established by a written agreement preventing the holder of the life insurance policy from affecting or using the cash surrender value after the irrevocable assignment.

Any type of life insurance policy is acceptable for collateral assignment, provided the insurance company allows assignment for the policy. Some banks may require an escrow account for the life insurance premiums, others may require proof of premiums paid or prepaid.

The limit for borrowing money from life insurance is set by the insurer, and it's typically no more than 90% of the policy's cash value. When your policy has enough cash value (minimums vary by insurer), you can use it as collateral to request a loan from your insurance company.

If you have a term policy, you will not be able to borrow against it. However, you may want to consider converting your policy to whole life insurance to take advantage of this option in the future. Look up the current cash value: Find out how much your policy is currently worth.

Term life insurance can be extremely valuable to your family and to your own peace of mind, but since it doesn't create cash value, it doesn't count as an asset.