The Fair Credit Reporting Act (FCRA) is designed to help ensure that credit bureaus furnish correct and complete information to businesses to use when evaluating your application. Your rights include:

The right to receive a copy of your credit report. The copy of your report must contain all of the information in your file at the time of your request.

The right to know the name of anyone who received your credit report in the last year for most purposes or in the last two years for employment purposes.

Any company that denies your application must supply the name and address of the credit bureau they contacted, provided the denial was based on information given by the credit bureau.

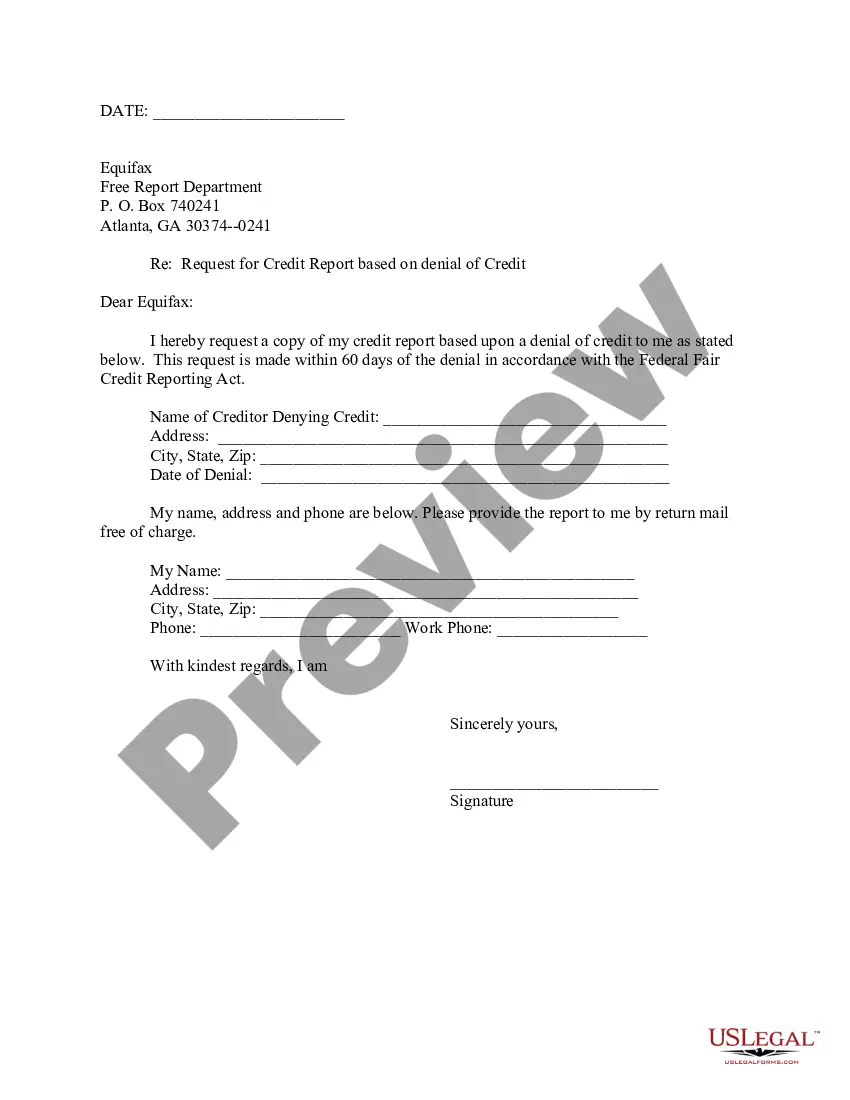

The right to a free copy of your credit report when your application is denied because of information supplied by the credit bureau. Your request must be made within 60 days of receiving your denial notice.

If you contest the completeness or accuracy of information in your report, you should file a dispute with the credit bureau and with the company that furnished the information to the bureau. Both the credit bureau and the furnisher of information are legally obligated to investigate your dispute.

A right to add a summary explanation to your credit report if your dispute is not resolved to your satisfaction.

New Mexico Request for Disclosure of Reasons for Denial of Credit Application Where Action Was Based on Information Not Obtained by Reporting Agency

Description

How to fill out Request For Disclosure Of Reasons For Denial Of Credit Application Where Action Was Based On Information Not Obtained By Reporting Agency?

It is possible to commit several hours on the Internet searching for the legal file design that meets the federal and state specifications you require. US Legal Forms offers a large number of legal types which are evaluated by experts. It is simple to obtain or printing the New Mexico Request for Disclosure of Reasons for Denial of Credit Application Where Action Was Based on Information Not Obtained by Reporting Agency from your assistance.

If you have a US Legal Forms profile, you may log in and click the Download option. Afterward, you may complete, modify, printing, or sign the New Mexico Request for Disclosure of Reasons for Denial of Credit Application Where Action Was Based on Information Not Obtained by Reporting Agency. Every single legal file design you get is yours permanently. To have an additional backup of the obtained develop, check out the My Forms tab and click the corresponding option.

If you are using the US Legal Forms internet site the very first time, keep to the simple directions listed below:

- First, make certain you have selected the proper file design for the state/town of your liking. Browse the develop description to make sure you have chosen the appropriate develop. If offered, make use of the Review option to search throughout the file design at the same time.

- If you would like find an additional model from the develop, make use of the Lookup industry to get the design that fits your needs and specifications.

- Upon having found the design you would like, click Purchase now to carry on.

- Select the rates strategy you would like, enter your qualifications, and register for a merchant account on US Legal Forms.

- Full the purchase. You should use your charge card or PayPal profile to purchase the legal develop.

- Select the structure from the file and obtain it in your product.

- Make alterations in your file if needed. It is possible to complete, modify and sign and printing New Mexico Request for Disclosure of Reasons for Denial of Credit Application Where Action Was Based on Information Not Obtained by Reporting Agency.

Download and printing a large number of file templates utilizing the US Legal Forms site, which offers the greatest selection of legal types. Use skilled and state-particular templates to handle your business or individual requires.

Form popularity

FAQ

If you have experienced problems with establishing credit or with accuracy of the credit reports that the credit bureaus have issued about you, these letter provide important information about the state of your credit at the time of the denial.

Equal Credit Opportunity Act (ECOA) The Dodd-Frank Act granted rule-making authority under ECOA to the CFPB and, with respect to entities within its jurisdiction, granted authority to the CFPB to supervise for and enforce compliance with ECOA and its implementing regulations.

A creditor must disclose the principal reasons for denying an application or taking other adverse action. The regulation does not mandate that a specific number of reasons be disclosed, but disclosure of more than four reasons is not likely to be helpful to the applicant.

The Dodd-Frank Act also amended two provisions of the FCRA to require the disclosure of a credit score and related information when a credit score is used in taking an adverse action or in risk-based pricing.

Adverse action notices under the ECOA and Regulation B are designed to help consumers and businesses by providing transparency to the credit underwriting process and protecting against potential credit discrimination by requiring creditors to explain the reasons adverse action was taken.

The FCRA also requires a creditor to disclose, as applicable, a credit score it used in taking adverse action along with related information, including up to four key factors that adversely affected the consumer's credit score (or up to five factors if the number of inquiries made with respect to that consumer report ...

Regulation B A written statement of actual and specific reasons for the adverse action or, if not providing the specific reason within the written notice, a statement that the applicant has a right to receive the specific reason for adverse action if requested within 60 days of the notification.

Regulation B prohibits creditors from requesting and collecting specific personal information about an applicant that has no bearing on the applicant's ability or willingness to repay the credit requested and could be used to discriminate against the applicant.