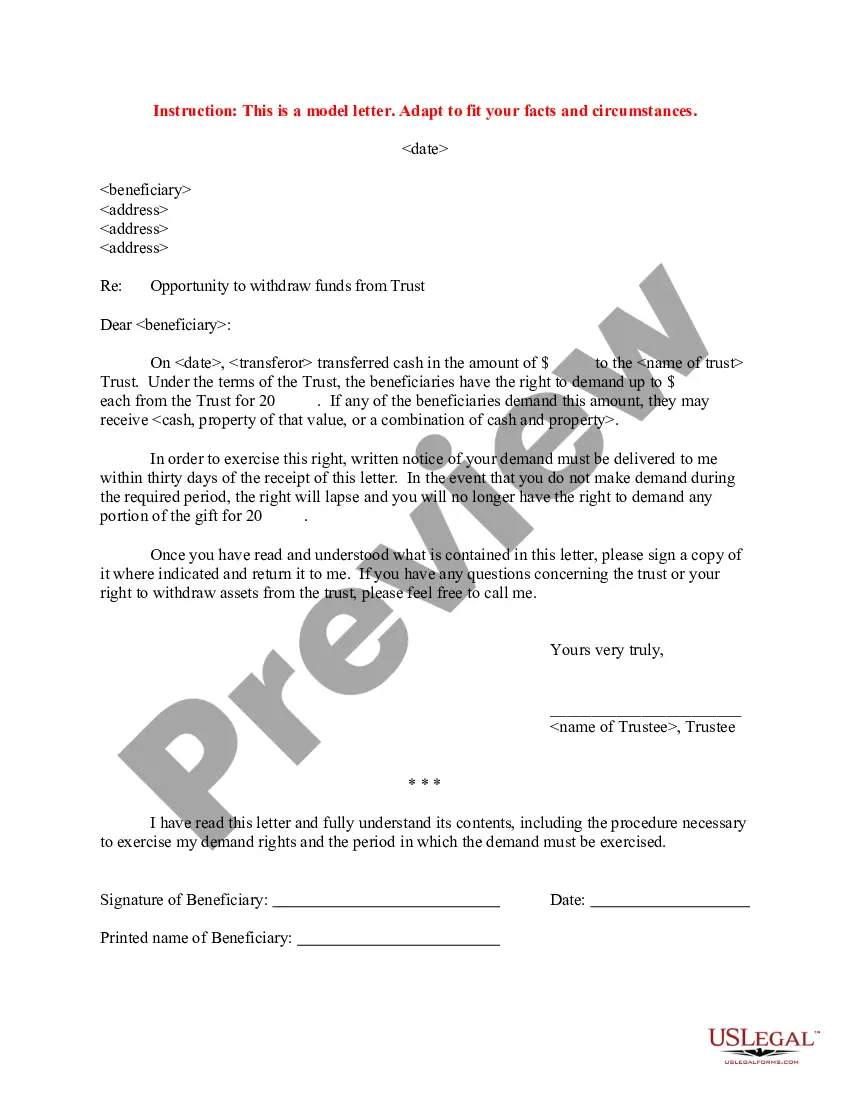

Trustee informs the trustor that he/she has the right to demand a certain amount of funds from the trust during the year. If the trustor demands a withdrawal for any of the beneficiaries, he/she may receive cash, property of that value, or a combination of cash and property.

New Jersey Letter regarding trust money

Instant download

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Letter Regarding Trust Money?

Are you currently in a situation where you require documentation for either commercial or personal reasons almost all the time.

There are numerous trustworthy document templates accessible online, but finding versions you can rely on is not easy.

US Legal Forms offers a vast array of form templates, such as the New Jersey Letter regarding trust money, that are designed to comply with state and federal regulations.

If you locate the correct form, simply click Purchase now.

Choose the payment option you prefer, fill in the necessary information to create your account, and complete the purchase using your PayPal or Visa or Mastercard.

- If you are already familiar with the US Legal Forms website and have a free account, just Log In.

- Afterwards, you can download the New Jersey Letter regarding trust money template.

- If you do not have an account and wish to start using US Legal Forms, follow these steps.

- Select the form you need and ensure it is for the correct city/county.

- Use the Review feature to examine the form.

- Check the summary to confirm you have chosen the appropriate form.

- If the form is not what you are looking for, use the Search section to find the form that meets your needs.

Form popularity

FAQ

Grantor trusts are required to file a New Jersey Gross Income Tax Fiduciary Return. If the grantor trust income is reportable by or tax- able to the grantor for Federal income tax purposes, it is also taxable to the grantor for New Jersey gross income tax purposes.

Generally, a will contest can be filed at any time prior to admission of a will to probate. If the decedent's will has already been admitted to probate, the statute of limitations on contesting a will is generally 120 days from the date of admission.

Trust beneficiaries generally have six months from the receipt of adequate reports to bring claims for breach of fiduciary duty by a Trustee. However, as is often the case in the law, there is always an exception.

If you can prove that the decedent created the trust under coercion, undue influence, or pressure from someone (usually a close family member, caregiver, or supposed beneficiary), a qualified probate court can invalidate the trust.

One example would be a monthly payout from the trust for the rest of your life. Often times, trustees are able to distribute trust assets to beneficiaries for general well-being. One distribution method is so common it is often referred to as HEMS, which stands for: health, education, maintenance, and support.

Issues in New Jersey Will ContestsA will contest is a challenge to the validity of a trust or a will. Some of the most common allegations in NJ will contests include: Undue influence by someone, usually in a position of trust, who persuades the person making the will to name them as a beneficiary.

Trusts Exempt from Tax Trusts that form part of a pension or profit-sharing plan, and trusts that are taxable as corporations for federal income tax purposes, are not required to file Form NJ-1041 or pay New Jersey Income Tax.

Trust beneficiaries must pay taxes on income and other distributions that they receive from the trust. Trust beneficiaries don't have to pay taxes on returned principal from the trust's assets. IRS forms K-1 and 1041 are required for filing tax returns that receive trust disbursements.

A trust can be contested, but only on certain grounds and by persons who have a financial stake in the outcome of the contest.

Key Takeaways. Revocable trusts, as their name implies, can be altered or completely revoked at any time by their grantorthe person who established them. The first step in dissolving a revocable trust is to remove all the assets that have been transferred into it.