New Jersey Shareholder and Corporation agreement to issue additional stock to a third party to raise capital

Description

How to fill out Shareholder And Corporation Agreement To Issue Additional Stock To A Third Party To Raise Capital?

Selecting the optimal approved document format can pose a challenge.

It goes without saying, there are numerous templates accessible online, but how can you locate the authorized version you need.

Utilize the US Legal Forms platform.

If you are a new user of US Legal Forms, here are straightforward steps for you to follow: First, make sure you have selected the right form for your locality/state. You can review the document using the Preview button and read the form description to confirm this is the right choice for you.

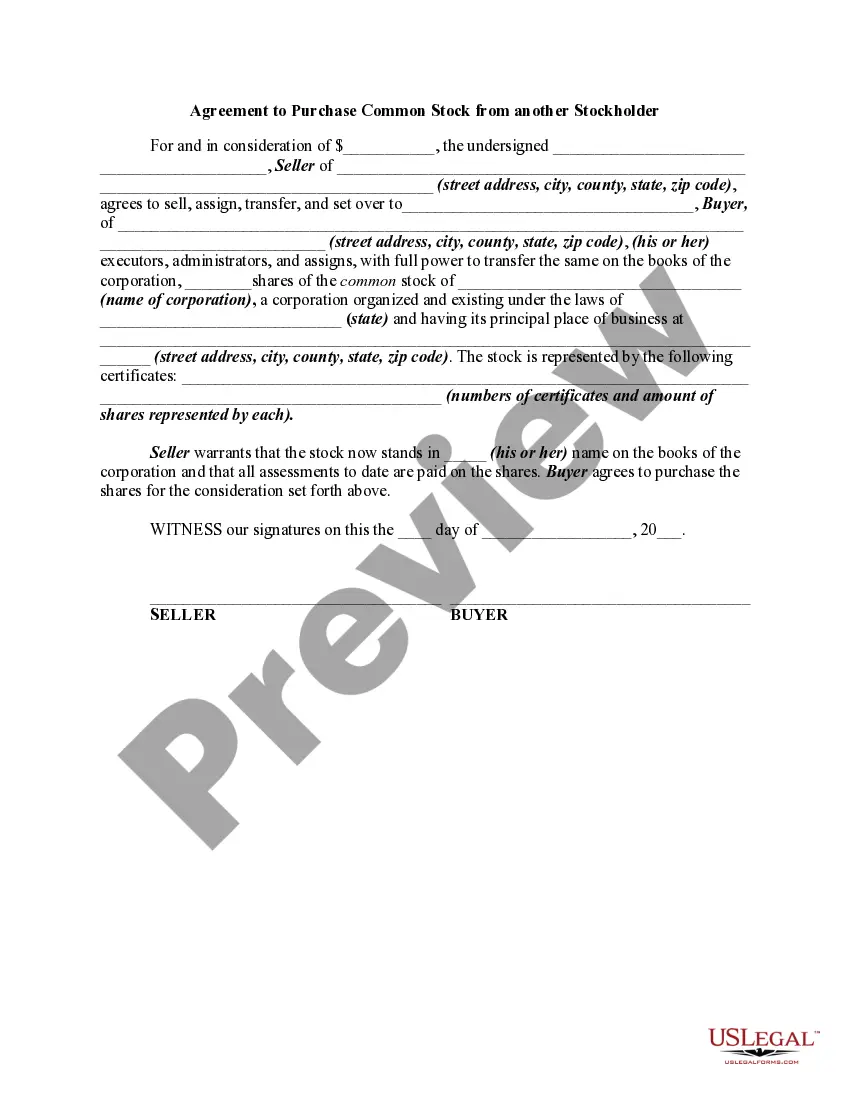

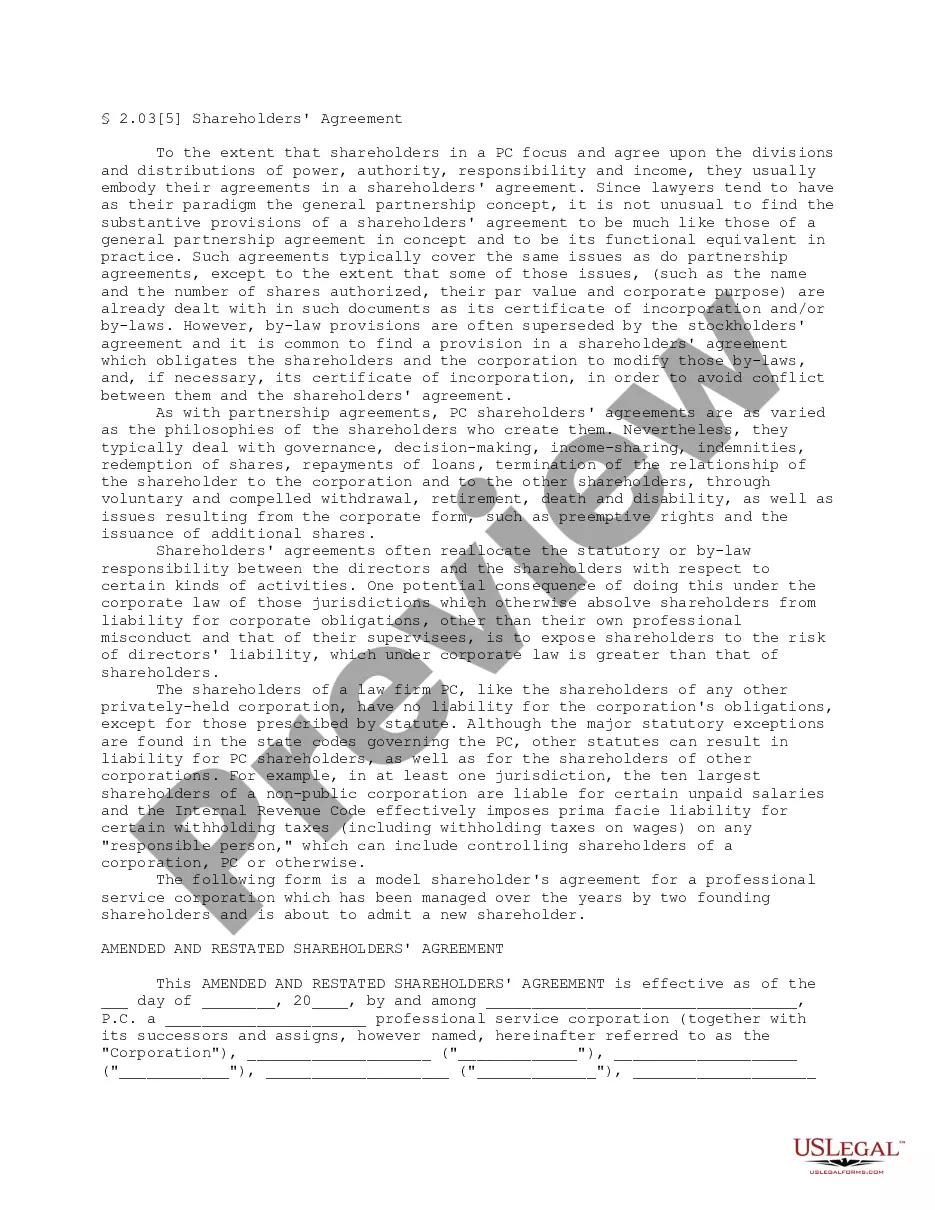

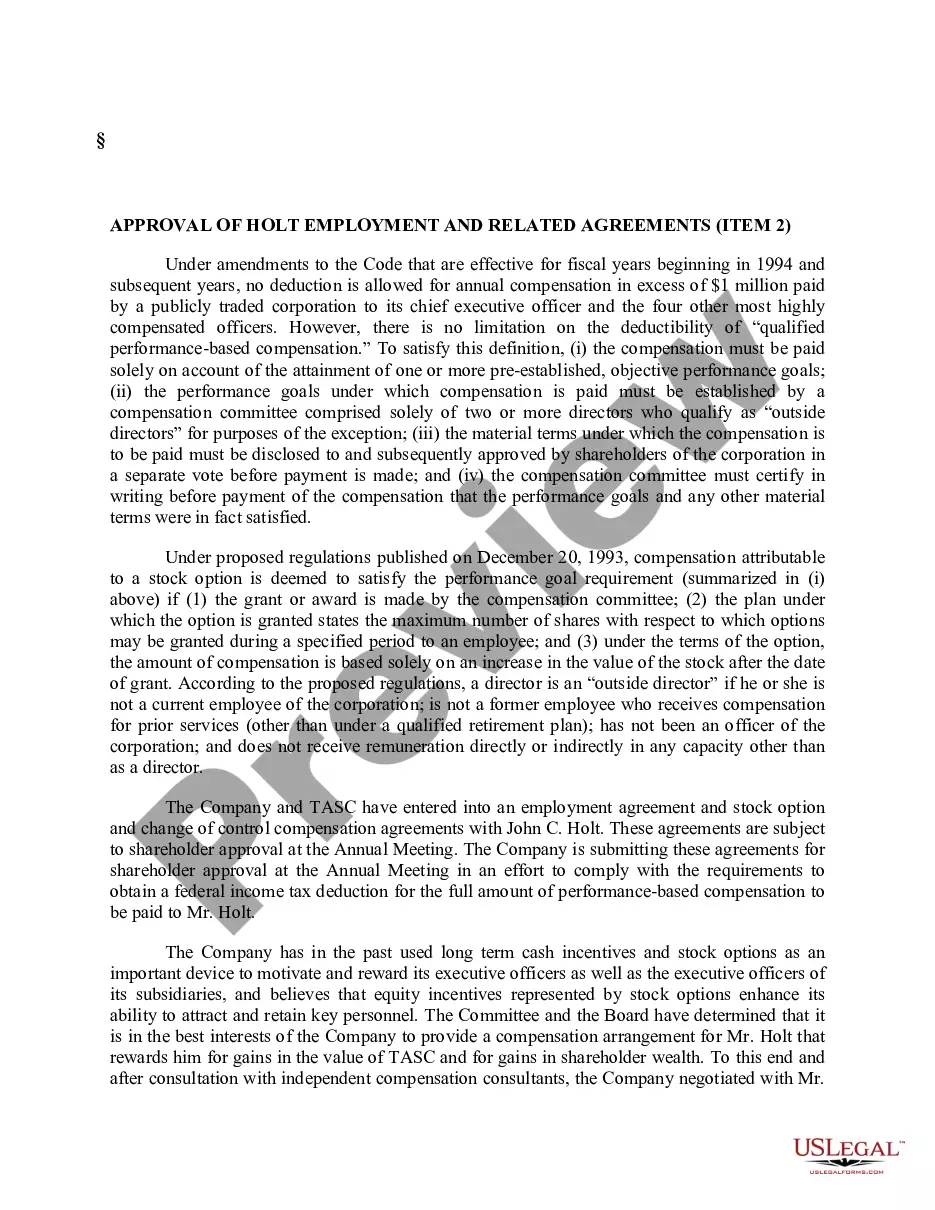

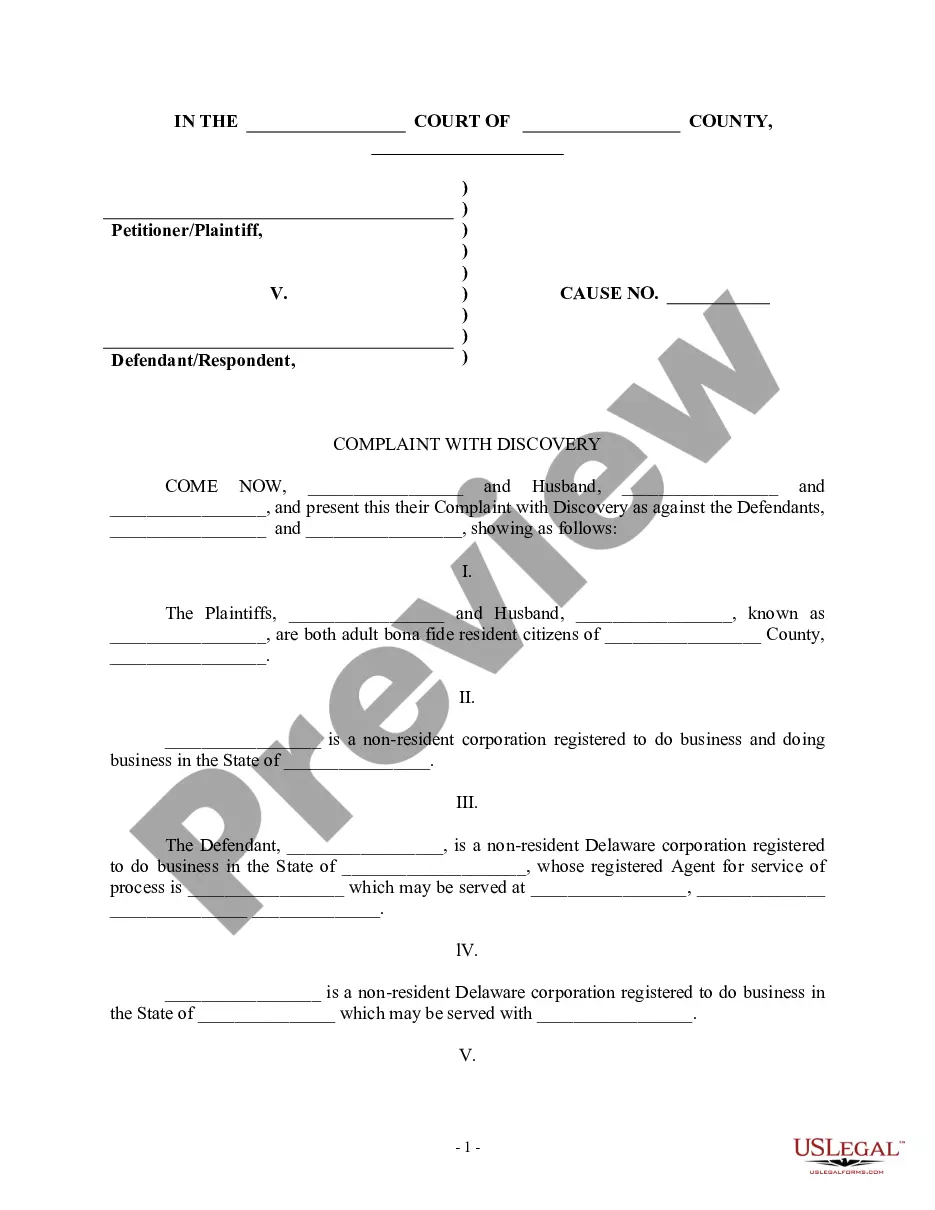

- The service provides a vast array of templates, such as the New Jersey Shareholder and Corporation agreement to issue additional stock to a third party to raise capital, which can be applied for both business and personal purposes.

- All forms are reviewed by professionals and adhere to state and federal regulations.

- If you are already registered, Log In to your account and click the Obtain button to get the New Jersey Shareholder and Corporation agreement to issue additional stock to a third party to raise capital.

- Use your account to view the authorized forms you have previously purchased.

- Go to the My documents section of your account to download another copy of the document you need.

Form popularity

FAQ

(a) Every corporation that has elected and qualifies pursuant to Section 1361 of the Internal Revenue Code and has qualified and been accepted as a New Jersey S Corporation is required to file a CBT-100S.

For taxpayers with Entire Net Income greater than $100,000, the tax rate is 9% (. 09) on adjusted entire net income or such portion thereof as may be allocable to New Jersey. For taxpayers with Entire Net Income greater than $50,000 and less than or equal to $100,000, the tax rate is 7.5% (.

Every partnership that has income or loss derived from sources in the State of New Jersey, or has any type of New Jersey resident partner, must file Form NJ-1065. Form NJ- CBT-1065 must be filed when the entity is required to calculate a tax on its nonresident partner(s).

A foreign corporation that owns a New Jersey partnership must file Form CBT-100S to claim the tax paid on their behalf by the part- nership. The foreign corporation cannot transfer the tax paid by the partnership on its behalf to any of its shareholders. Out-of-Business Corporations.

The number of shares that a company needs to have in order to form an S-corporation is essentially determined by the owners of the business. An S-corporation owner can choose to have as little as 10,000 shares of stock, or as many as a million shares of stock.

Limited number of shareholders: An S corp cannot have more than 100 shareholders, meaning it can't go public and limiting its ability to raise capital from new investors.

The number of authorized shares per company is assessed at the company's creation and can only be increased or decreased through a vote by the shareholders.

An S corporation can be authorized to issue 50,000 shares, but the boards of directors can decide to give out 10,000 shares instead of 50,000. That means there are 40,000 shares for the company to issue at another date in the future if they need to increase capital.

The New Jersey Business Alternative Income Tax also referred to as BAIT or NJ BAIT helps business owners mitigate the negative impact of the federal state and local tax (SALT) deduction cap. It's estimated to save New Jersey business owners $200 to $400 million annually.

Issuing of extra shares will require a resolution to be passed by a general meeting of the company shareholders. The only way of avoiding diluting the company further by issuing shares to new investors is by existing shareholders taking up the extra shares on top of their own.