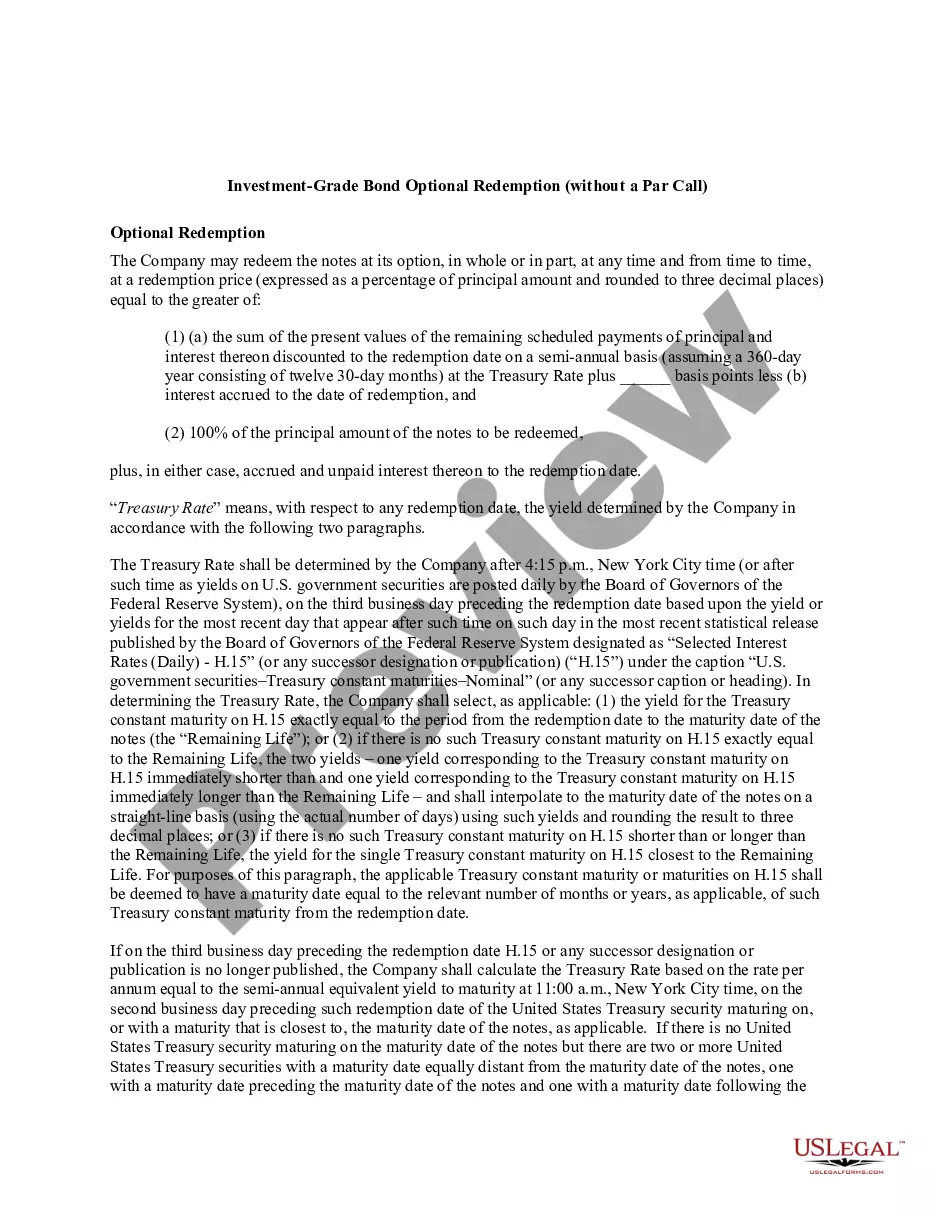

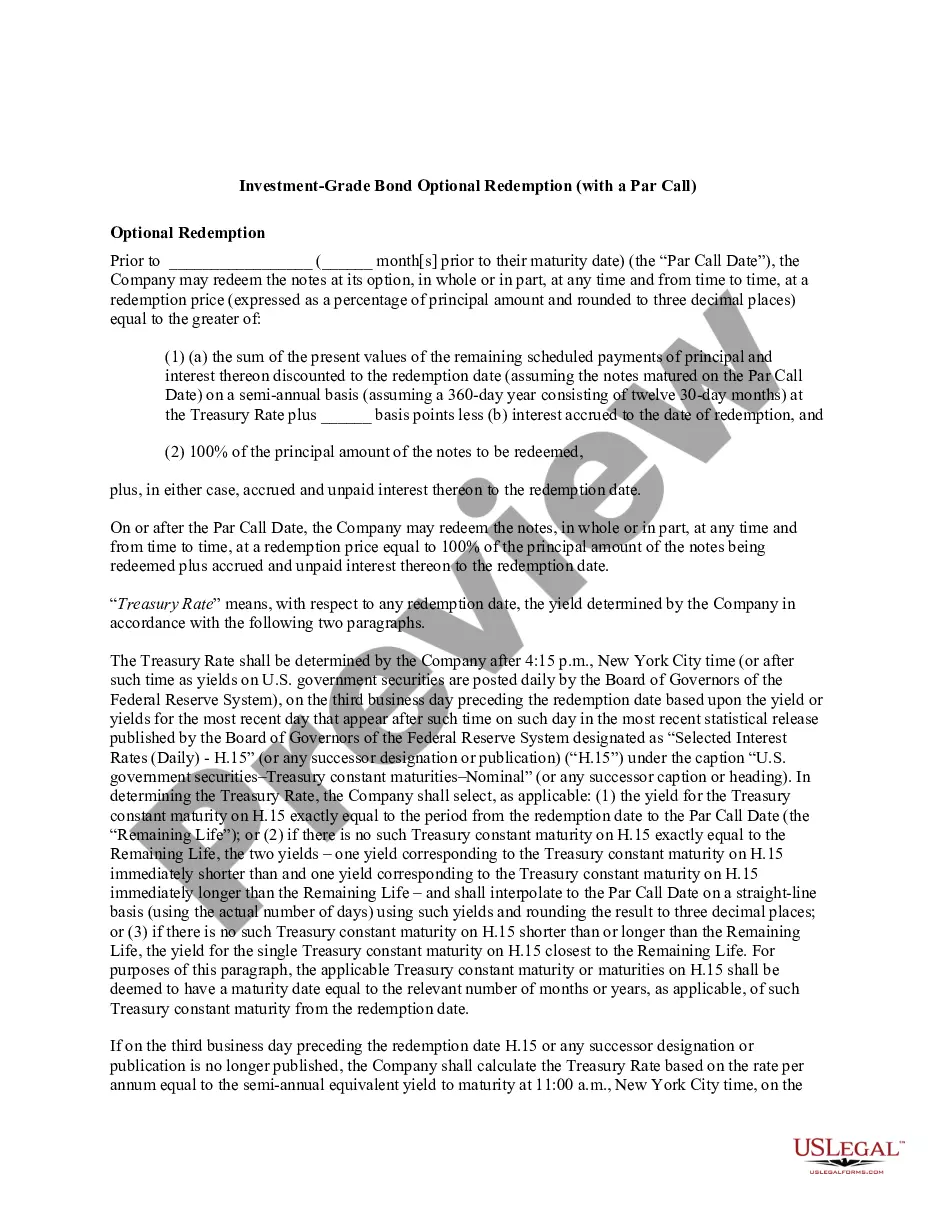

"Investment-grade bond optional redemption provisions, and the calculation of the make-whole redemption price, can vary by issuer and by the methodology used by the investment bank assisting with such calculation. This variation in language and calculation results in a lack of standardization in the manner of calculating the redemption price. As a result, market participants have expressed the desire for standardized language in investment-grade bond optional redemption provisions.

"

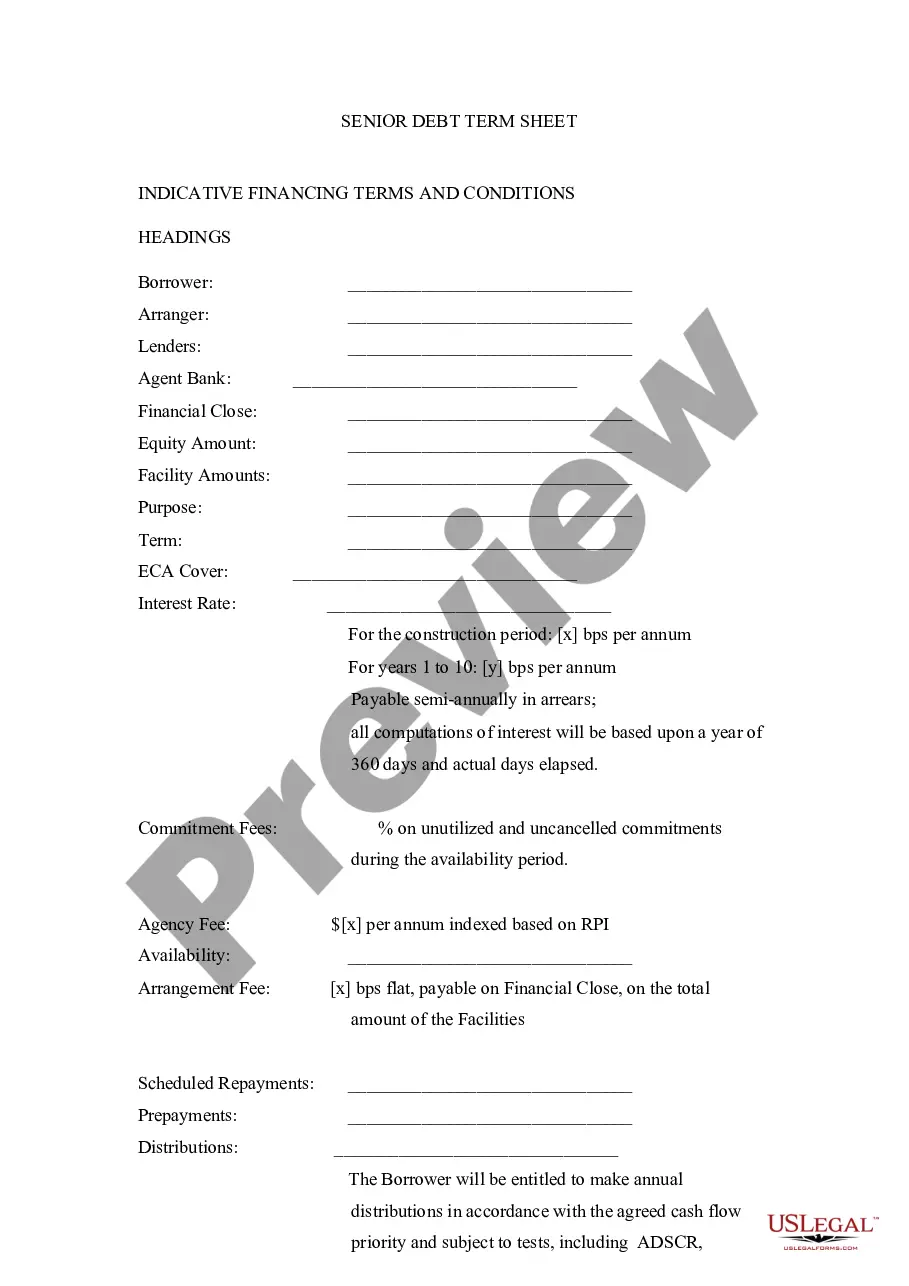

New Hampshire Executive Summary Investment-Grade Bond Optional Redemption

State:

Multi-State

Control #:

US-ENTREP-0050-1

Format:

Word;

Rich Text

Instant download

Description

Free preview

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Built-in online Word editor

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Export easily

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

E-sign your document

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

Notarize online 24/7

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

Store your document securely

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Executive Summary Investment-Grade Bond Optional Redemption?

US Legal Forms - one of many most significant libraries of legitimate kinds in America - delivers a wide array of legitimate document layouts you can acquire or print out. Utilizing the site, you can find 1000s of kinds for company and specific uses, sorted by categories, states, or key phrases.You can find the most recent variations of kinds such as the New Hampshire Executive Summary Investment-Grade Bond Optional Redemption in seconds.

If you currently have a monthly subscription, log in and acquire New Hampshire Executive Summary Investment-Grade Bond Optional Redemption from your US Legal Forms catalogue. The Obtain switch will appear on each and every develop you perspective. You have access to all in the past delivered electronically kinds inside the My Forms tab of your respective accounts.

If you would like use US Legal Forms the very first time, here are simple guidelines to get you started:

- Be sure to have chosen the proper develop for your personal town/region. Select the Review switch to review the form`s content material. Look at the develop information to ensure that you have chosen the correct develop.

- In case the develop does not fit your demands, make use of the Research industry on top of the screen to obtain the one that does.

- When you are pleased with the shape, confirm your option by clicking the Purchase now switch. Then, opt for the prices prepare you like and give your references to register on an accounts.

- Procedure the financial transaction. Make use of Visa or Mastercard or PayPal accounts to finish the financial transaction.

- Find the formatting and acquire the shape on the product.

- Make modifications. Load, change and print out and indicator the delivered electronically New Hampshire Executive Summary Investment-Grade Bond Optional Redemption.

Every design you included with your bank account does not have an expiry day and is also yours permanently. So, in order to acquire or print out an additional duplicate, just go to the My Forms segment and click on the develop you want.

Gain access to the New Hampshire Executive Summary Investment-Grade Bond Optional Redemption with US Legal Forms, the most substantial catalogue of legitimate document layouts. Use 1000s of specialist and condition-certain layouts that meet your organization or specific requirements and demands.

Form popularity

FAQ

When a company redeems bonds, the accounting will typically involve: Removing the Bonds Payable Liability: The face value of the bonds is removed from the liability section of the balance sheet. Paying Cash: The company reduces its cash balance by the amount paid to redeem the bonds.

As a bond issuer, the company is a borrower. As such, the act of issuing the bond creates a liability. Thus, bonds payable appear on the liability side of the company's balance sheet. Generally, bonds payable fall in the non-current class of liabilities.

Journalizing Early Redemption Debit: Bonds payable by the portion of the face value being redeemed. Credit: Cash for the bond payable amount multiplied by the callable rate. Debit/Credit: Premium or discount by the a portion of the unamortized balance (same portion as bond payable being redeemed)

Optional Redemption On or after the Par Call Date, the Company may redeem the notes, in whole or in part, at any time and from time to time, at a redemption price equal to 100% of the principal amount of the notes being redeemed plus accrued and unpaid interest thereon to the redemption date.

Accounting for Bond Redemption When it is time to redeem the bonds, all premiums and discounts should have been amortized, so the entry is simply a debit to the bonds payable account and a credit to the cash account.

If bonds are issued at par or face value on an interest date, the entry is straightforward: Cash is debited and Bonds Payable is credited for the total dollar amount of the bond issue.