New Hampshire Fair Credit Act Disclosure Notice

Description

How to fill out Fair Credit Act Disclosure Notice?

If you need to collect, acquire, or produce legal document templates, utilize US Legal Forms, the largest collection of legal forms, accessible online.

Make use of the site’s simple and convenient search to locate the documents you need.

Various templates for businesses and personal purposes are organized by categories and states, or keywords.

Step 5. Process the payment. You can utilize your Visa or MasterCard or PayPal account to complete the transaction.

Step 6. Choose the format of the legal form and download it to your device.

- Use US Legal Forms to retrieve the New Hampshire Fair Credit Act Disclosure Notice with a few clicks.

- If you are already a US Legal Forms user, Log Into your account and select the Download option to get the New Hampshire Fair Credit Act Disclosure Notice.

- You can also access forms you have previously downloaded from the My documents section of your account.

- If you are using US Legal Forms for the first time, follow the steps below.

- Step 1. Ensure you have selected the form for the correct city/state.

- Step 2. Use the Preview option to review the form's content. Don't forget to read the explanation.

- Step 3. If you are unsatisfied with the form, use the Search field at the top of the screen to find alternative templates of the legal form.

- Step 4. Once you locate the form you need, click the Get now button. Choose your preferred pricing plan and enter your information to create an account.

Form popularity

FAQ

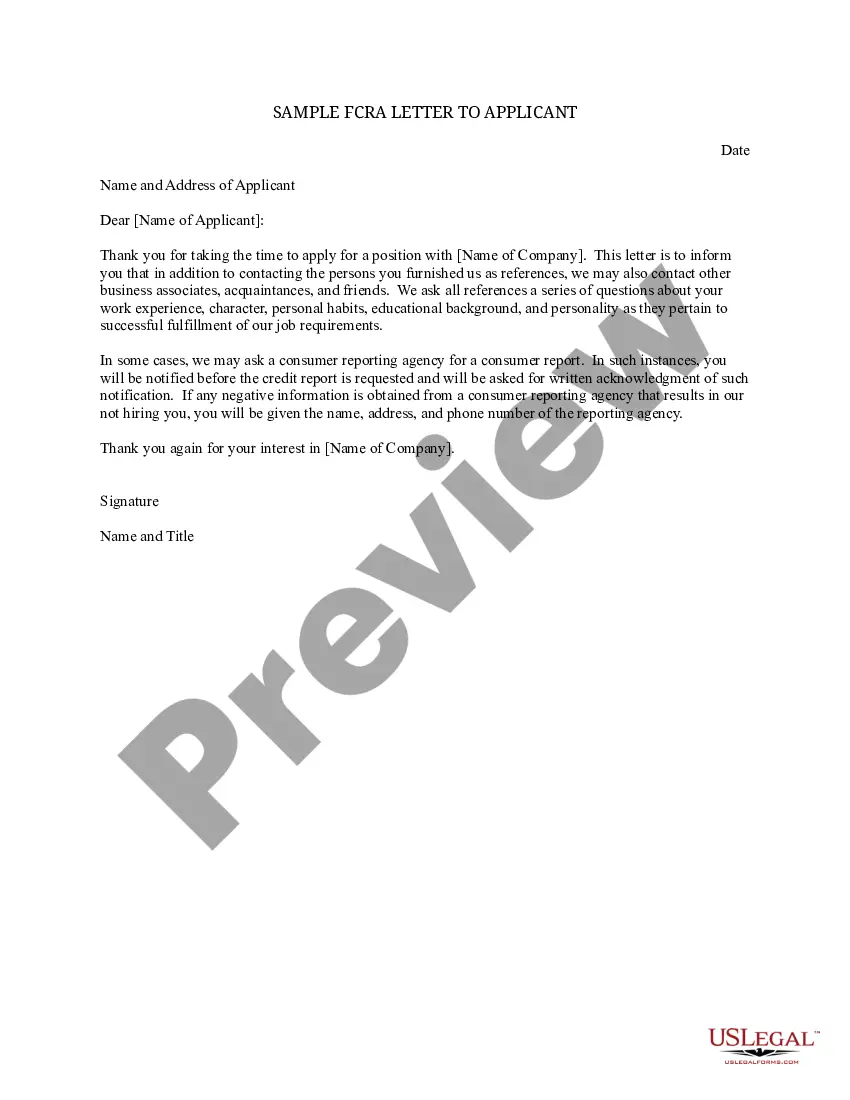

The Fair Credit Reporting Act (FCRA), 15 U.S.C. 1681-1681y, requires that this notice be provided to inform users of consumer reports of their legal obligations.

A creditor must disclose the credit score used by the person in making the credit decision on a risk-based pricing notice. Credit score has the same meaning used in §609(f)(2)(a) of the FCRA. Most credit scores that meet the FCRA definition are scores that creditors obtain from consumer reporting agencies.

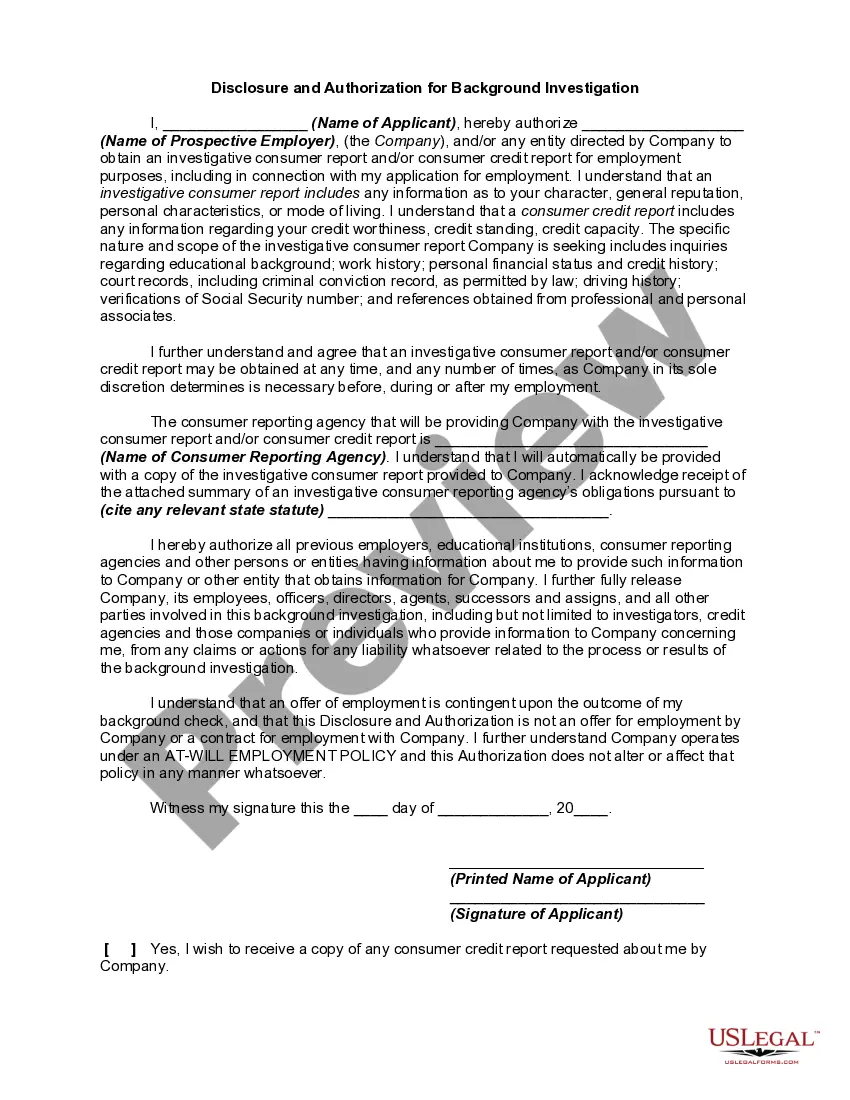

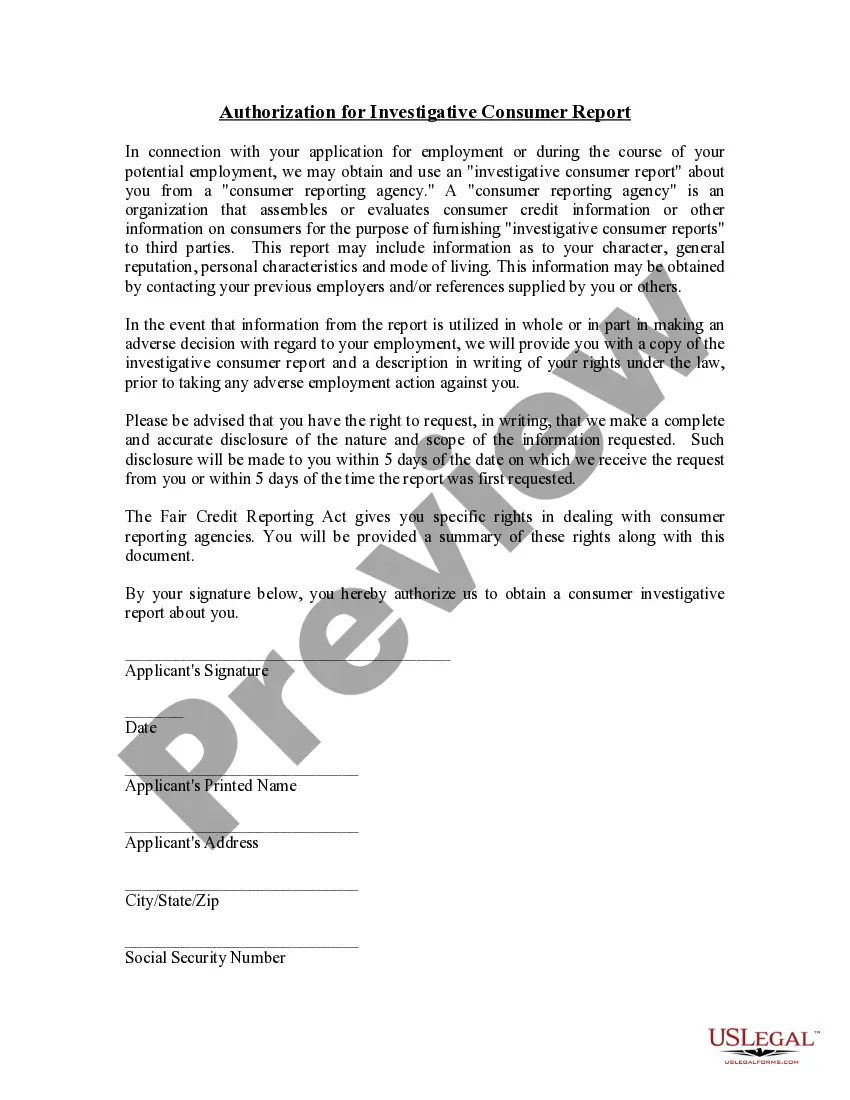

Under the FCRA, an employer may not run a background check on a prospective employee without first providing "a clear and conspicuous disclosure . . . in a document that consists solely of that disclosure, that a consumer report may be obtained for employment purposes." For efficiency, many employers include all

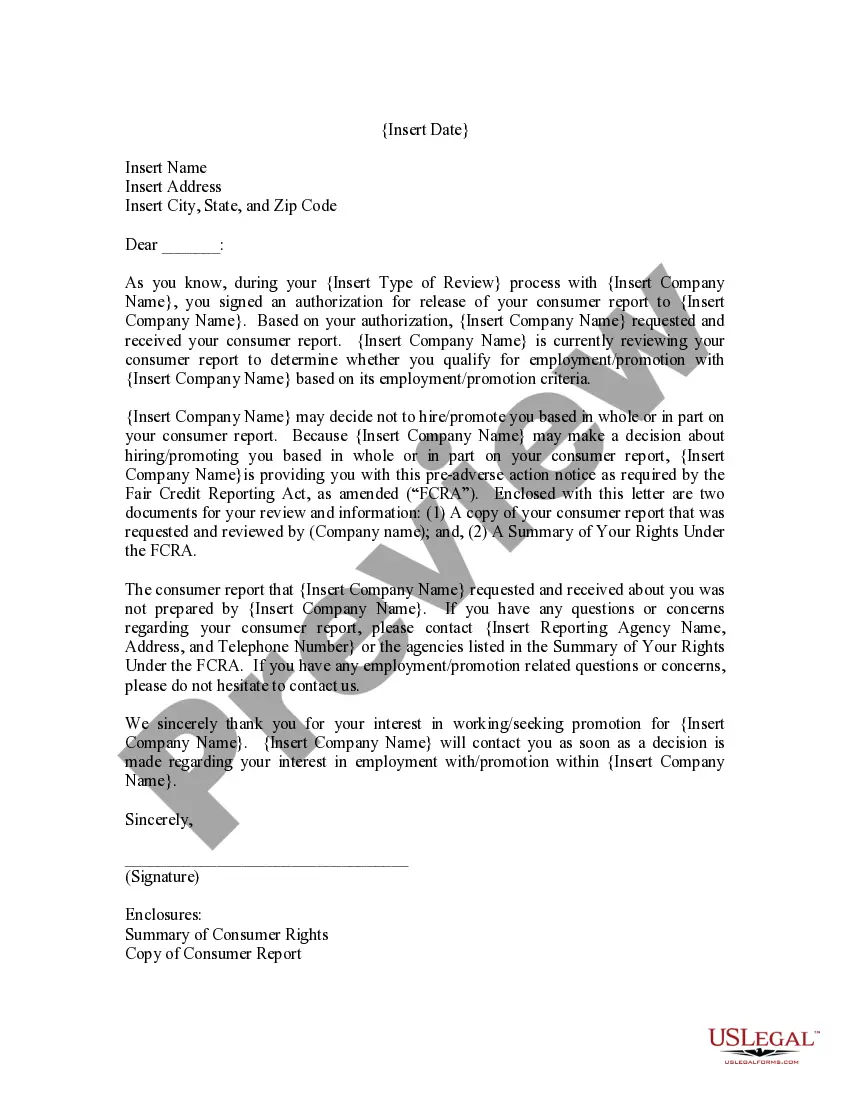

On July 21, 2010, Congress passed the Dodd-Frank Wall Street Reform and Consumer Protection Act (Dodd-Frank Act). Section 1100F of the Dodd-Frank Act amended the FCRA to require disclosure of credit scores and information relating to credit scores for both risk-based pricing and FCRA adverse action notices.

The FCRA gives you the right to be told if information in your credit file is used against you to deny your application for credit, employment or insurance. The FCRA also gives you the right to request and access all the information a consumer reporting agency has about you (this is called "file disclosure").

Under the FCRA, consumer reporting agencies are required to provide consumers with the information in their own file upon request, and consumer reporting agencies are not allowed to share information with third parties unless there is a permissible purpose.

Consumer reporting agencies must correct or delete inaccurate, incomplete, or unverifiable information. Inaccurate, incomplete, or unverifiable information must be removed or corrected, usually within 30 days. However, a consumer reporting agency may continue to report information it has verified as accurate.

Under the FCRA, an employer may not run a background check on a prospective employee without first providing "a clear and conspicuous disclosure . . . in a document that consists solely of that disclosure, that a consumer report may be obtained for employment purposes." For efficiency, many employers include all

The Act (Title VI of the Consumer Credit Protection Act) protects information collected by consumer reporting agencies such as credit bureaus, medical information companies and tenant screening services. Information in a consumer report cannot be provided to anyone who does not have a purpose specified in the Act.

A credit file disclosure provides you with all of the information in your credit file maintained by a consumer reporting company that could be provided by the consumer reporting company in a consumer report about you to a third party, such as a lender.