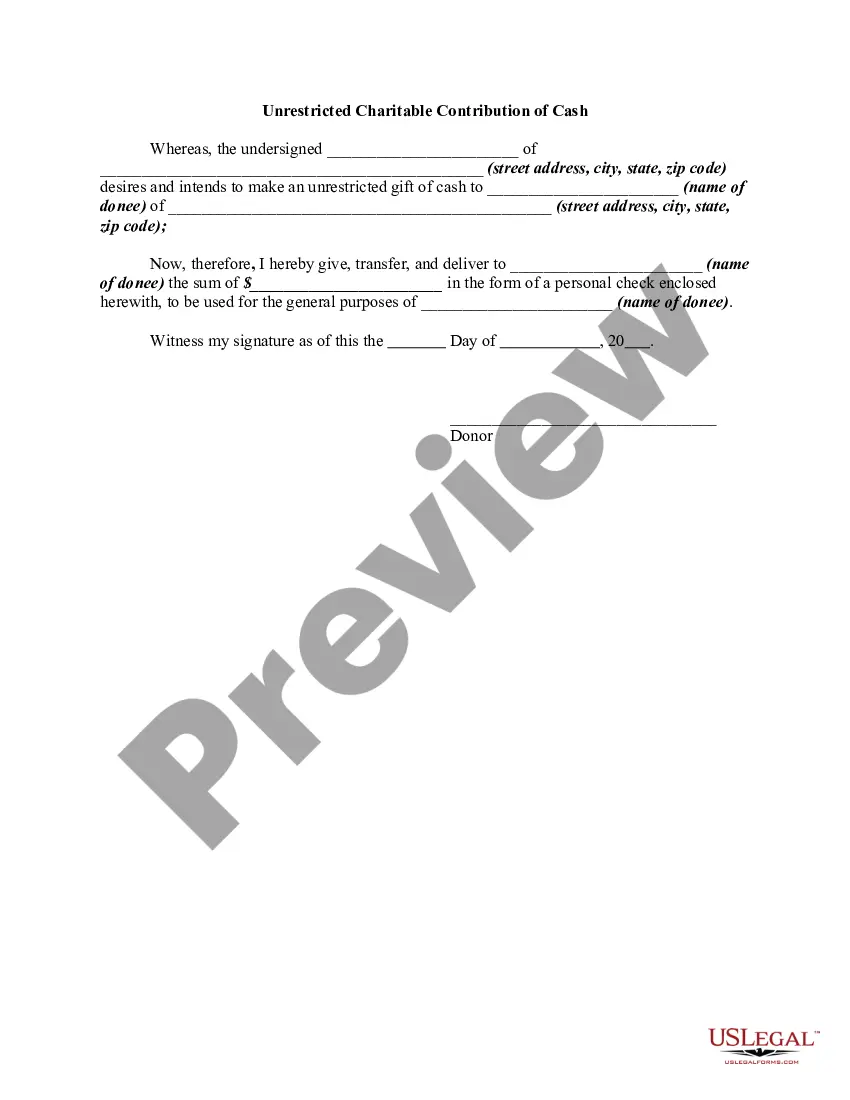

North Carolina Unrestricted Charitable Contribution of Cash

Description

How to fill out Unrestricted Charitable Contribution Of Cash?

Selecting the optimal legal documents template can be a challenge.

Clearly, there is an abundance of templates accessible online, but how can you locate the legal form you require.

Utilize the US Legal Forms website.

First, ensure that you have selected the correct form for your region/location. You can browse the form using the Preview option and read the form description to confirm that it is suitable for you.

- The service offers a vast array of templates, including the North Carolina Unrestricted Charitable Donation of Cash, which you may employ for both business and personal purposes.

- All of the forms are verified by experts and adhere to federal and state regulations.

- If you are already registered, Log Into your account and click on the Download button to obtain the North Carolina Unrestricted Charitable Donation of Cash.

- Use your account to search through the legal forms you have previously acquired.

- Visit the My documents section of your account to retrieve another copy of the document you need.

- If you are a new customer of US Legal Forms, here are simple instructions for you to follow.

Form popularity

FAQ

The 183 day rule in North Carolina determines whether an individual qualifies as a resident for tax purposes. To be considered a resident, you must spend more than 183 days in the state within a calendar year. This rule is especially important when it comes to North Carolina Unrestricted Charitable Contribution of Cash, as residents may enjoy certain tax benefits related to charitable giving. It is advisable to consult with a tax professional or use platforms like USLegalForms for guidance on how to navigate these rules effectively.

In certain situations, you can deduct charitable contributions without itemizing your deductions. As of recent tax law changes, individuals can claim a deduction of up to $300 for cash donations made to qualified charities in North Carolina, including North Carolina Unrestricted Charitable Contributions of Cash. This provision makes it easier for many donors to support non-profits while benefiting from tax relief, even if they choose the standard deduction. If you need assistance with tax forms or deductions, consider USLegalForms for user-friendly solutions.

Classifying charitable contributions involves identifying the type of donation and understanding its impact on taxes. In North Carolina, unrestricted cash contributions are treated as gifts that can support a non-profit’s operations or specific projects. Donors should keep records of their contributions, including receipts, to verify their claims. For clarity on classification, seek guidance from platforms like USLegalForms to navigate the complexities of tax regulations.

Yes, non-profits in North Carolina can achieve tax-exempt status when they meet specific requirements set by the IRS. Generally, organizations that qualify as 501(c)(3) entities are eligible for tax exemptions. This classification allows them to accept North Carolina Unrestricted Charitable Contributions of Cash while providing donors with potential tax benefits. If you're starting a non-profit, using USLegalForms can help ensure you understand the process and required documentation.

Charitable Contribution Limitation North Carolina does not allow an individual to deduct qualified contributions of up to 100% of federal adjusted gross income (AGI). For N.C. income tax purposes, an individual may only deduct qualified contributions of up to 60% of AGI.

Just like last year, individuals, including married individuals filing separate returns, who take the standard deduction can claim a deduction of up to $300 on their 2021 federal income tax for their charitable cash contributions made to certain qualifying charitable organizations.

But the special deduction is available for anyone who takes the standard deduction, which the IRS says is nine out of 10 taxpayers. But that doesn't mean you'll get the full $300 (if you're single or married filing individual returns) or $600 (if you're married and filing jointly) back.

Charitable Contributions: For cash contributions to public charities, North Carolina will continue to allow deductions up to 60% of the taxpayer's adjusted gross income. The Federal law allows a deduction up to 100% of adjusted gross income for such contributions through 2021.

Following tax law changes, cash donations of up to $300 made this year by December 31, 2020 are now deductible without having to itemize when people file their taxes in 2021. The Coronavirus Aid, Relief and Economic Security Act includes several temporary tax law changes to help charities.

The $300 deduction ($600 for joint filing) must be for donations made in cash, which includes currency, checks, credit or debit cards, and electronic funds transfers. You cannot take the deduction for contributions of property, such as clothing or household items, nor for volunteering.