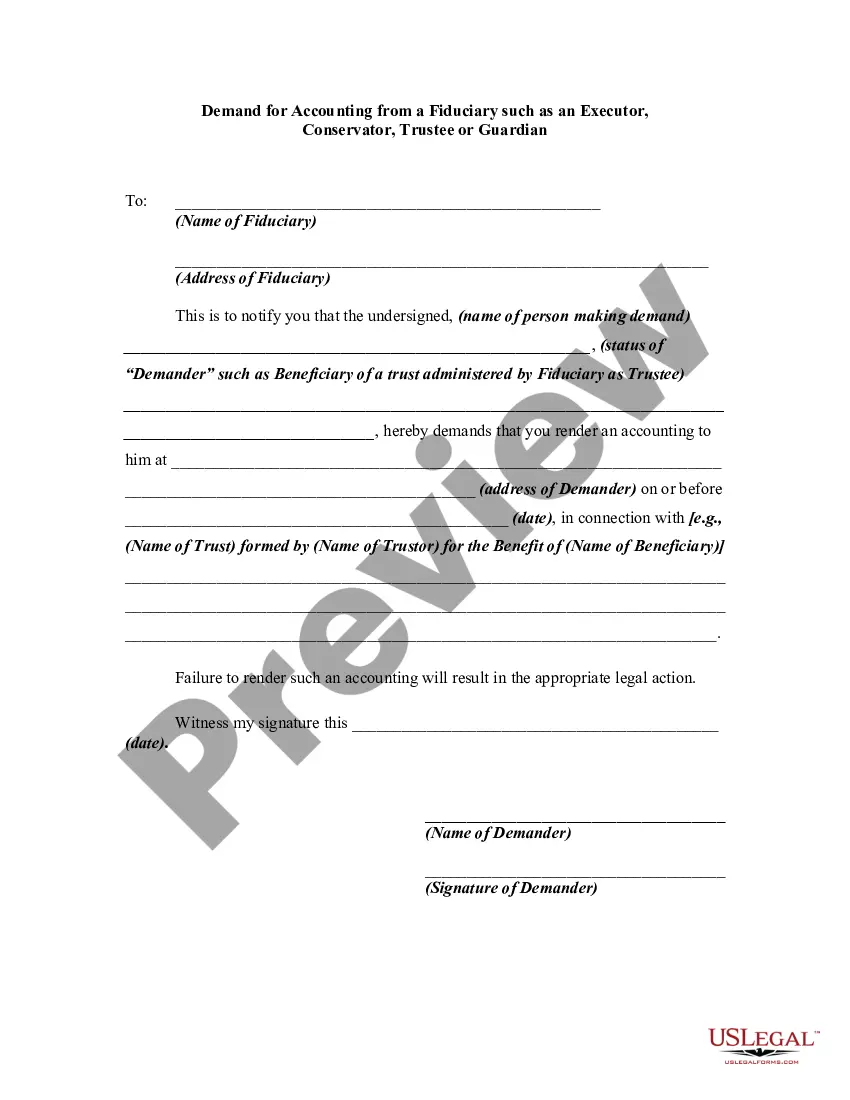

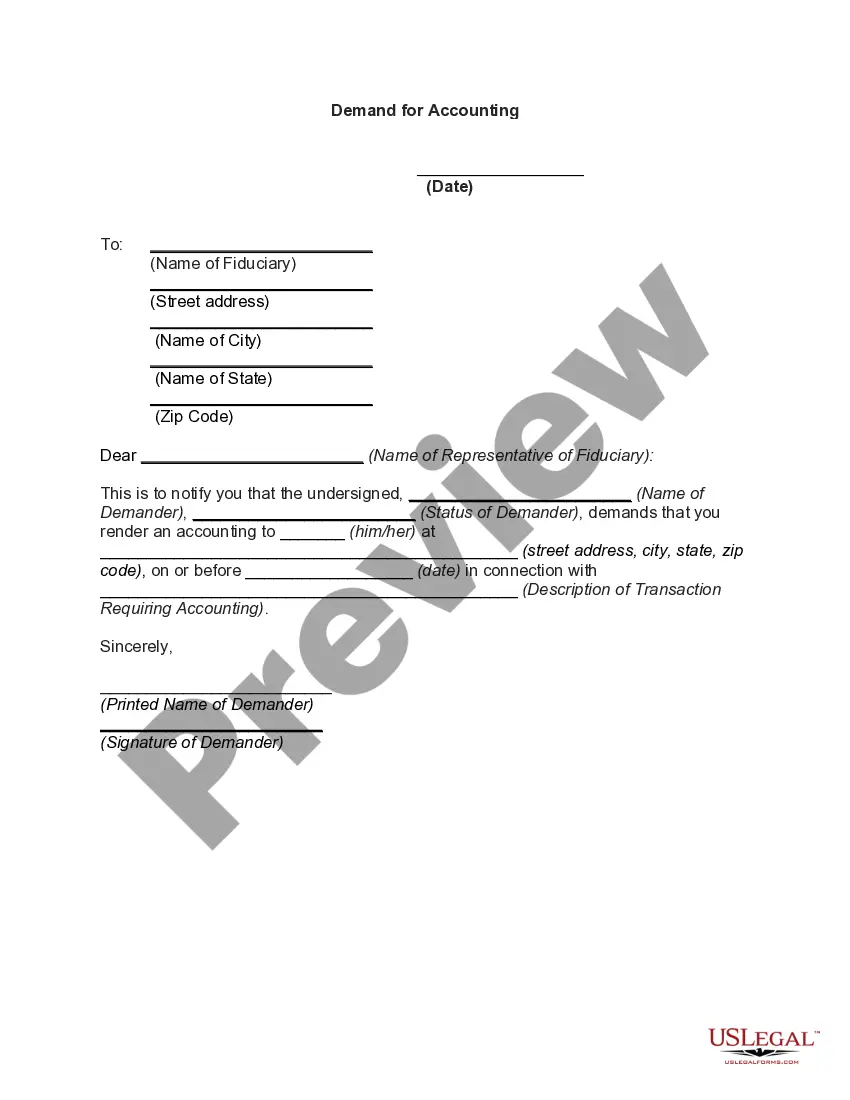

Sometimes, a prior demand by a potential plaintiff for an accounting, and a refusal by the fiduciary to account, are conditions precedent to the bringing of an action for an accounting. This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

North Carolina Demand for Accounting from a Fiduciary

Instant download

Description

How to fill out Demand For Accounting From A Fiduciary?

US Legal Forms - one of the largest collections of legal documents in the United States - offers a variety of legal template formats that you can obtain or print. By utilizing the site, you can access thousands of documents for business and personal purposes, organized by categories, states, or keywords.

You can find the latest versions of documents such as the North Carolina Demand for Accounting from a Fiduciary in just a few minutes. If you already have a monthly subscription, Log In and obtain the North Carolina Demand for Accounting from a Fiduciary in the US Legal Forms library. The Download button will appear on every document you view. You can access all previously downloaded documents in the My documents section of your profile.

If you are using US Legal Forms for the first time, here are some simple instructions to get started: Ensure you have selected the correct form for your area/region. Click the Preview button to review the document’s content. Check the document description to make certain you have selected the right form. If the document does not meet your needs, use the Search box at the top of the screen to find one that does. If you are satisfied with the form, confirm your choice by clicking on the Get now button. Then, select your preferred pricing plan and provide your details to register for an account. Complete the purchase. Use your credit card or PayPal account to finalize the transaction. Choose the format and download the document to your device. Edit. Fill out, modify, print, and sign the downloaded North Carolina Demand for Accounting from a Fiduciary.

- Each template you add to your account does not have an expiration date and is yours permanently.

- So, if you want to download or print another copy, simply visit the My documents section and click on the document you need.

- Access the North Carolina Demand for Accounting from a Fiduciary with US Legal Forms, the largest collection of legal document templates.

- Utilize thousands of professional and state-specific templates that meet your business or personal requirements.

Form popularity

FAQ

Generally, any beneficiary of a trust can demand an accounting from the fiduciary. This includes individuals or entities with a legal interest in the trust assets. By understanding your rights, you can effectively use the North Carolina Demand for Accounting from a Fiduciary to ensure proper asset management.

A trust account in North Carolina is a financial account established to hold assets on behalf of another party, typically managed by a fiduciary. This account is separate from the fiduciary's personal assets, ensuring that the funds are used solely for the intended beneficiaries. Understanding how these accounts function can clarify your rights and responsibilities under a North Carolina Demand for Accounting from a Fiduciary.

Yes, a beneficiary can demand an accounting from the fiduciary. This right is supported by North Carolina law, which allows beneficiaries to seek transparency regarding the management of trust assets. If you feel your rights as a beneficiary are being overlooked, exercising this demand is a critical step.

You can request an accounting by drafting a formal letter or using a specific form that outlines your request. Ensure you include the details of the fiduciary relationship and clearly specify what information you require. Utilizing platforms like US Legal Forms can simplify this process, providing templates tailored for a North Carolina Demand for Accounting from a Fiduciary.

Yes, there is often a strong demand for accounting, especially when beneficiaries suspect mismanagement. North Carolina law allows beneficiaries to request a detailed accounting to ensure transparency. This demand acts as a crucial tool for maintaining trust and accountability among fiduciaries.

To compel an accounting from a reluctant trustee, you may need to send a formal written demand. This demand should clearly state your request for the accounting documentation. If the trustee still refuses, consider seeking legal assistance to explore your options under the North Carolina Demand for Accounting from a Fiduciary guidelines.

The five fiduciary duties typically include the duty of care, duty of loyalty, duty of obedience, duty of full disclosure, and duty of accounting. Each of these responsibilities requires fiduciaries to act in the best interests of those they serve. If you feel these duties have been compromised, a North Carolina Demand for Accounting from a Fiduciary may help you ensure accountability.

An example of a violation of the duty of accounting occurs when a fiduciary fails to provide detailed financial records or misrepresents financial information to the beneficiaries. Such actions can lead to a loss of trust and financial harm. If you believe a breach has occurred, consider pursuing a North Carolina Demand for Accounting from a Fiduciary to rectify the situation.

A fiduciary in accounting is an individual or entity trusted to manage the financial assets and interests of another party, such as a trustee or an executor. They are legally required to maintain a high standard of care in their financial dealings. If you're dealing with misconduct, a North Carolina Demand for Accounting from a Fiduciary might address your concerns effectively.

To file a breach of fiduciary duty, gather evidence that shows the fiduciary did not fulfill their obligations. You typically need to establish that the fiduciary acted against the interests of the beneficiaries. A North Carolina Demand for Accounting from a Fiduciary can also help you take formal action against a fiduciary who has failed in their duties.