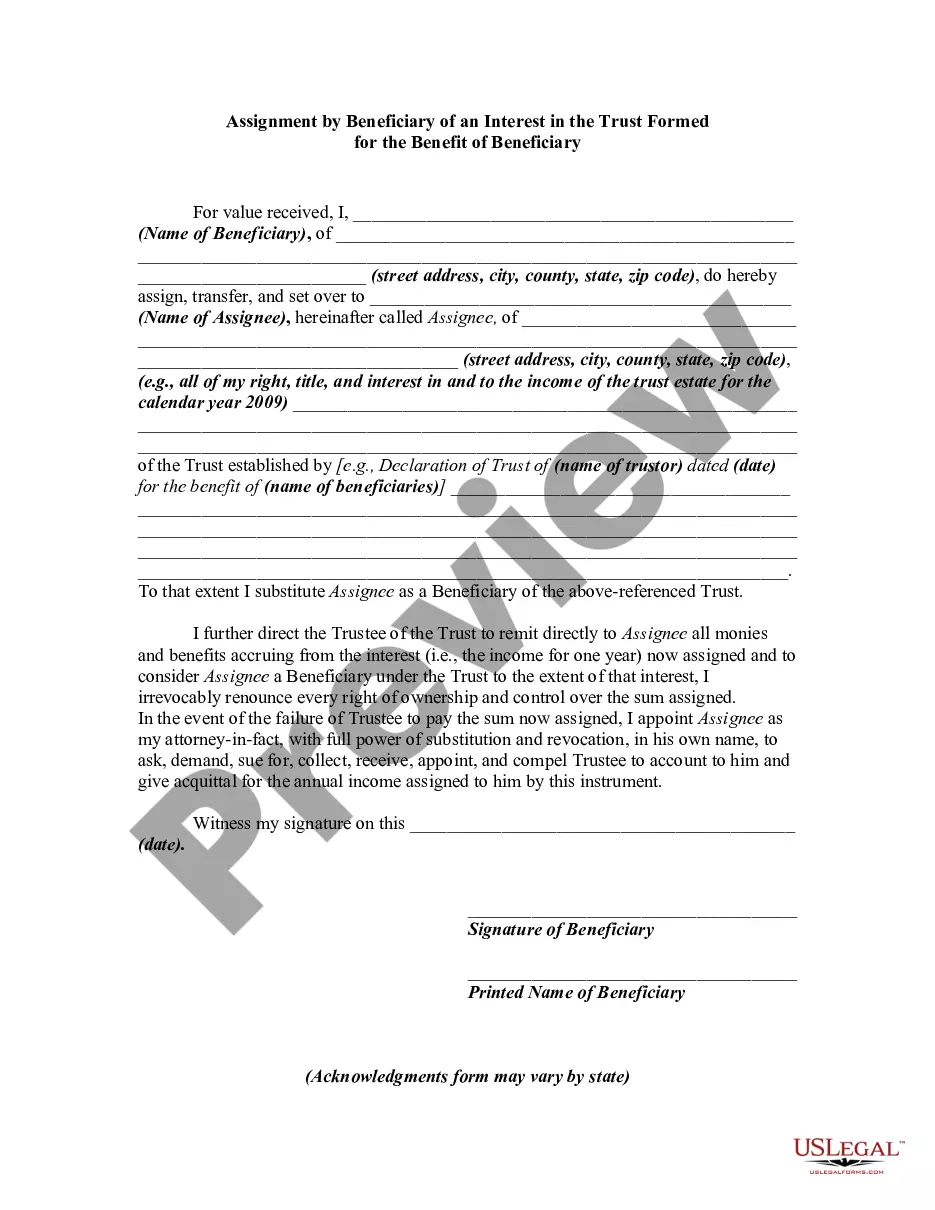

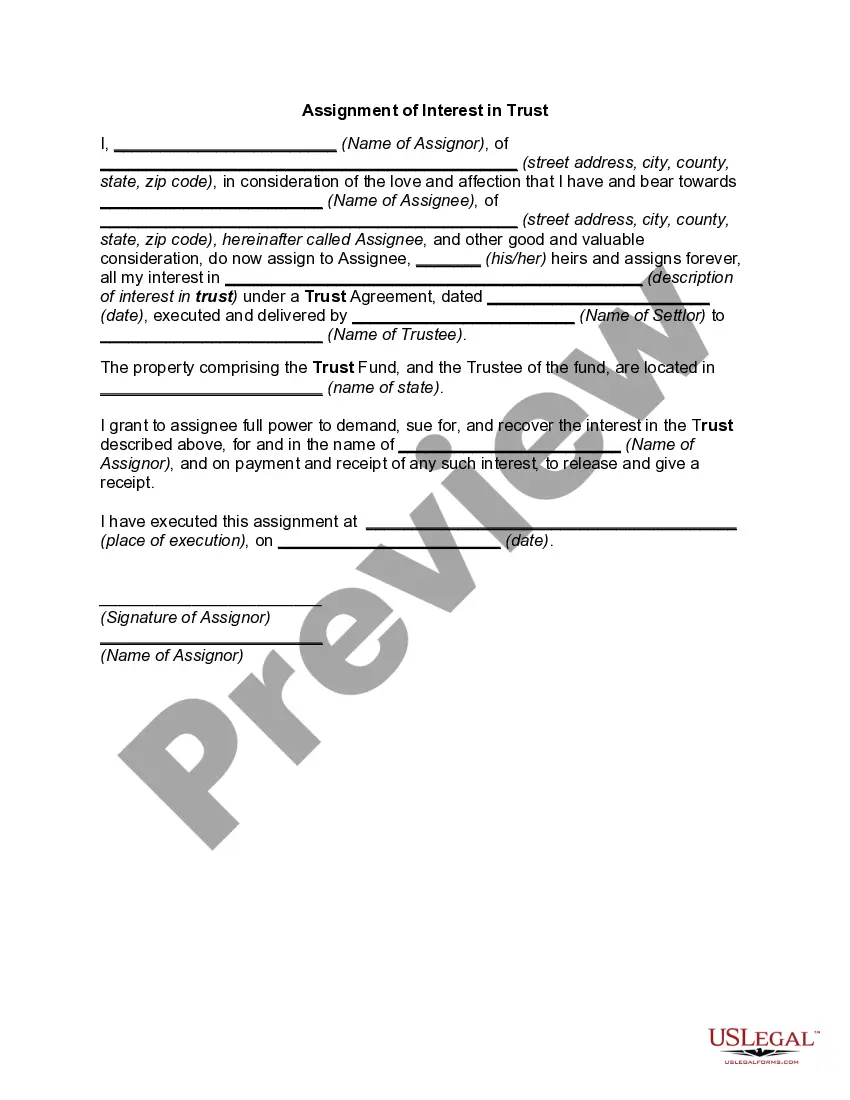

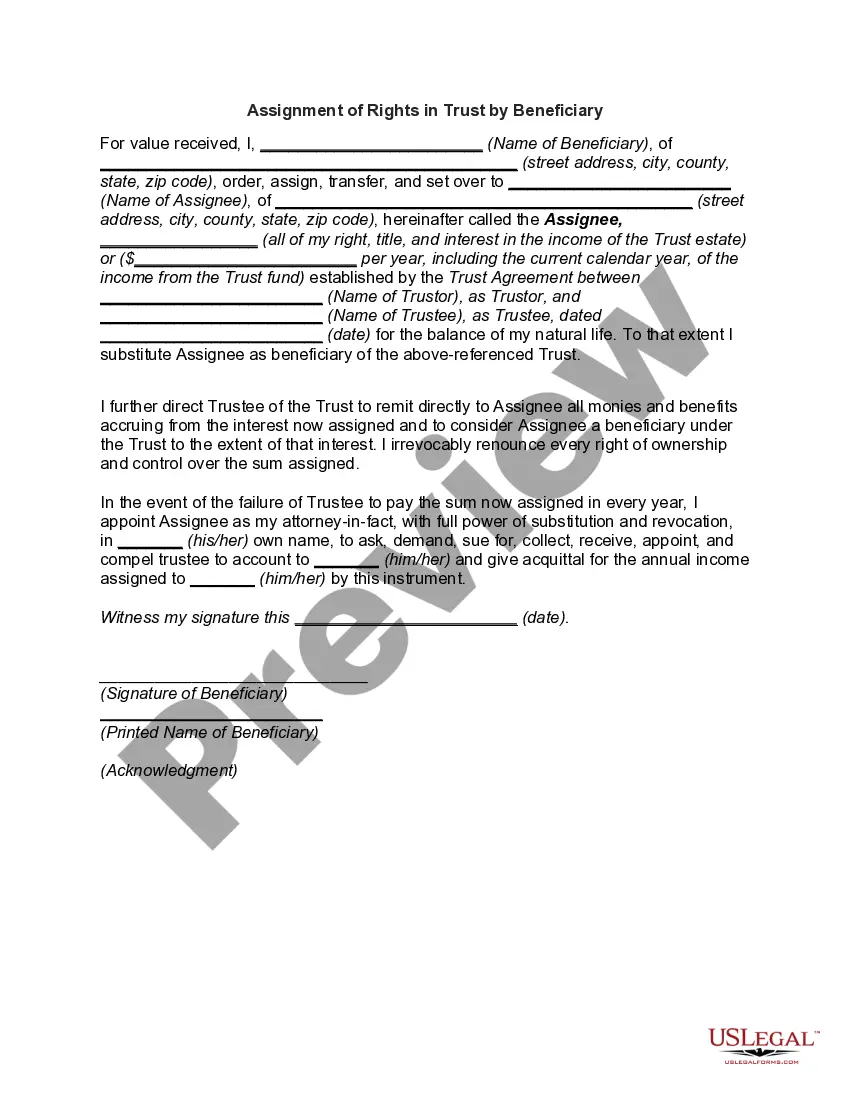

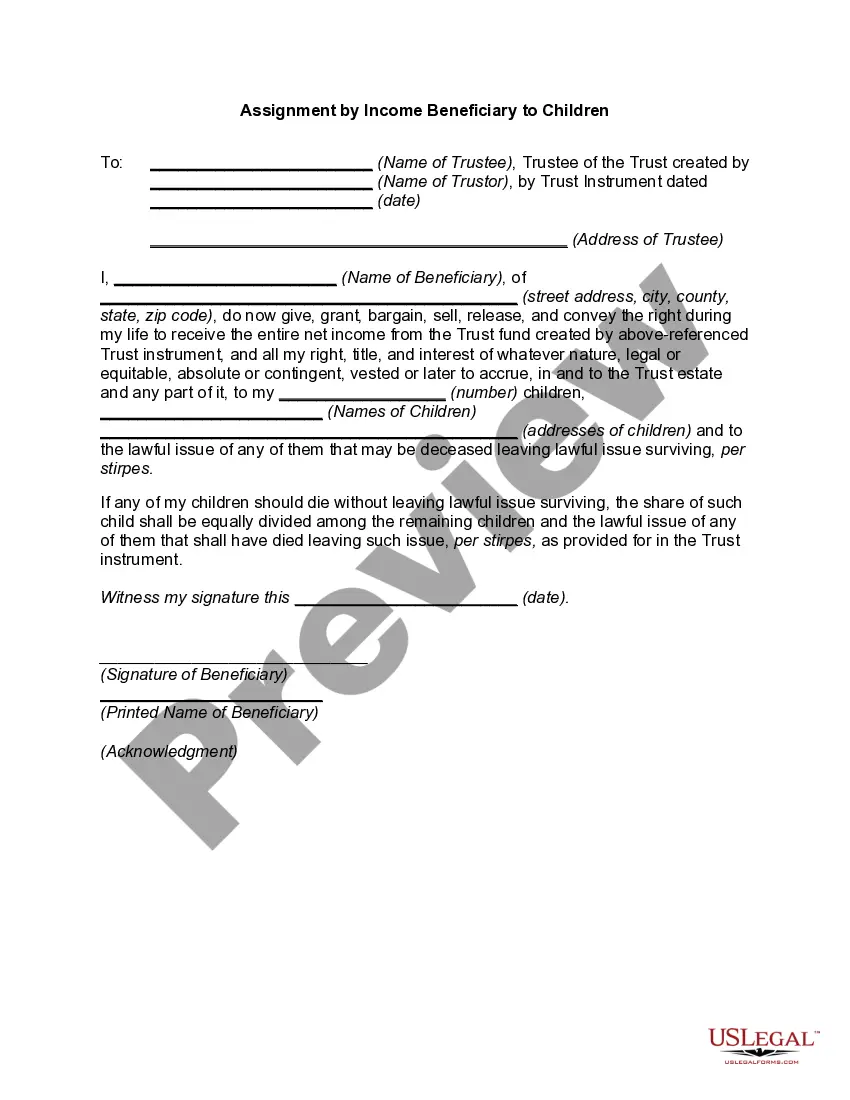

An assignment by a beneficiary of a portion of his or her interest in a trust is usually regarded as a transfer of a right, title, or estate in property rather than a chose in action (like an account receivable). As a general rule, the essentials of such an assignment or transfer are the same as those for any transfer of real or personal property. This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

North Carolina Assignment by Beneficiary of a Percentage of the Income of a Trust

Instant download

Description

Free preview

How to fill out Assignment By Beneficiary Of A Percentage Of The Income Of A Trust?

If you desire to compile, acquire, or generate official document templates, utilize US Legal Forms, the most extensive collection of official forms accessible online.

Leverage the website's straightforward and convenient search function to procure the documents you require.

A range of templates for commercial and personal purposes are organized by categories and states, or keywords.

Step 5. Process the payment. You may use your credit card or PayPal account to complete the transaction.

Step 6. Select the format of your official form and download it onto your device.

- Utilize US Legal Forms to secure the North Carolina Assignment by Beneficiary of a Percentage of the Income of a Trust in just a few clicks.

- If you are already a US Legal Forms user, Log In to your account and click the Obtain button to retrieve the North Carolina Assignment by Beneficiary of a Percentage of the Income of a Trust.

- You can also access forms you previously downloaded in the My documents section of your account.

- If it is your first time using US Legal Forms, follow the instructions below.

- Step 1. Ensure you have selected the form for the correct city/state.

- Step 2. Use the Preview feature to review the form’s details. Remember to check the outline.

- Step 3. If you are dissatisfied with the form, utilize the Search field at the top of the screen to find alternative versions of the official form template.

- Step 4. After locating the form you need, click the Buy now button. Choose the pricing plan you prefer and enter your details to register for an account.

Form popularity

FAQ

In North Carolina, when a beneficiary receives distributions from a trust, these distributions are generally subject to taxation. The key factor is whether the distribution is classified as income or principal. When you utilize the North Carolina Assignment by Beneficiary of a Percentage of the Income of a Trust, it's essential to understand that income distributions may be taxable based on the trust's earning. For tailored legal guidance, consider using USLegalForms, as they offer resources to help you navigate these complex tax implications.

Reporting beneficiary income from a trust requires clear understanding of IRS guidelines as well as state regulations in North Carolina. First, gather all relevant documentation concerning distributions made to the beneficiary. When filing taxes, you need to report the income received from the trust by the beneficiary on their tax return, ensuring accuracy. For a comprehensive approach to navigating these requirements, U.S. Legal Forms provides helpful templates and guides related to North Carolina Assignment by Beneficiary of a Percentage of the Income of a Trust.

To allocate trust income in North Carolina, first review the trust document to understand its specific terms for income distribution. Generally, the income generated by the trust is divided among beneficiaries based on the instruction provided in the trust. In cases of North Carolina Assignment by Beneficiary of a Percentage of the Income of a Trust, the beneficiaries must follow this allocation process rigorously to ensure compliance with state laws. For a more seamless experience, consider using resources from U.S. Legal Forms to assist with documentation.

Yes, North Carolina does tax trust income. When a trustee distributes income to beneficiaries, those beneficiaries may need to report that income on their personal tax returns. In terms of structure, a North Carolina Assignment by Beneficiary of a Percentage of the Income of a Trust allows clarity on how the income is shared and taxed among beneficiaries. Understanding the tax implications is vital for effective financial planning and compliance.

The distribution of income from a trust refers to how the income generated by trust assets is allocated to the beneficiaries. In the context of a North Carolina Assignment by Beneficiary of a Percentage of the Income of a Trust, it is essential to understand that beneficiaries receive a specified portion of the trust's income. This distribution can vary based on the trust's terms and the agreement between the trustee and beneficiaries. Efficient management ensures that beneficiaries receive their fair share in a timely manner.

Certain assets may be exempt from estate tax, including life insurance proceeds, retirement accounts, and some jointly owned property. These exemptions can vary based on state laws and specific circumstances. When dealing with the North Carolina Assignment by Beneficiary of a Percentage of the Income of a Trust, it is crucial for individuals to understand which assets may be exempt to ensure effective estate planning.

Yes, income from a trust is typically taxable to the beneficiary who receives it. Beneficiaries must report this income on their income tax return, which can influence their taxable income for the year. By utilizing the North Carolina Assignment by Beneficiary of a Percentage of the Income of a Trust wisely, beneficiaries can better manage their tax responsibilities and financial planning.

Trust income is generally taxed to the beneficiary based on their individual tax bracket. When a beneficiary receives income from a trust, they report it on their tax return, which allows them to fulfill their tax obligations. Understanding the North Carolina Assignment by Beneficiary of a Percentage of the Income of a Trust is essential for beneficiaries to be aware of how trust income can influence their tax situation.

Accounts with beneficiaries may be subject to estate tax, depending on the overall value of the estate and applicable state laws. In North Carolina, the estate tax laws have specific thresholds that determine tax liability. It is advisable for individuals to review the implications of the North Carolina Assignment by Beneficiary of a Percentage of the Income of a Trust carefully, as this can impact estate planning decisions.

Generally, estate distributions are not taxable to the beneficiary upon receipt. However, the income generated from those assets, such as trust income, may be subject to taxation. When considering the North Carolina Assignment by Beneficiary of a Percentage of the Income of a Trust, it is vital for beneficiaries to consult with a tax professional to understand any potential tax implications.