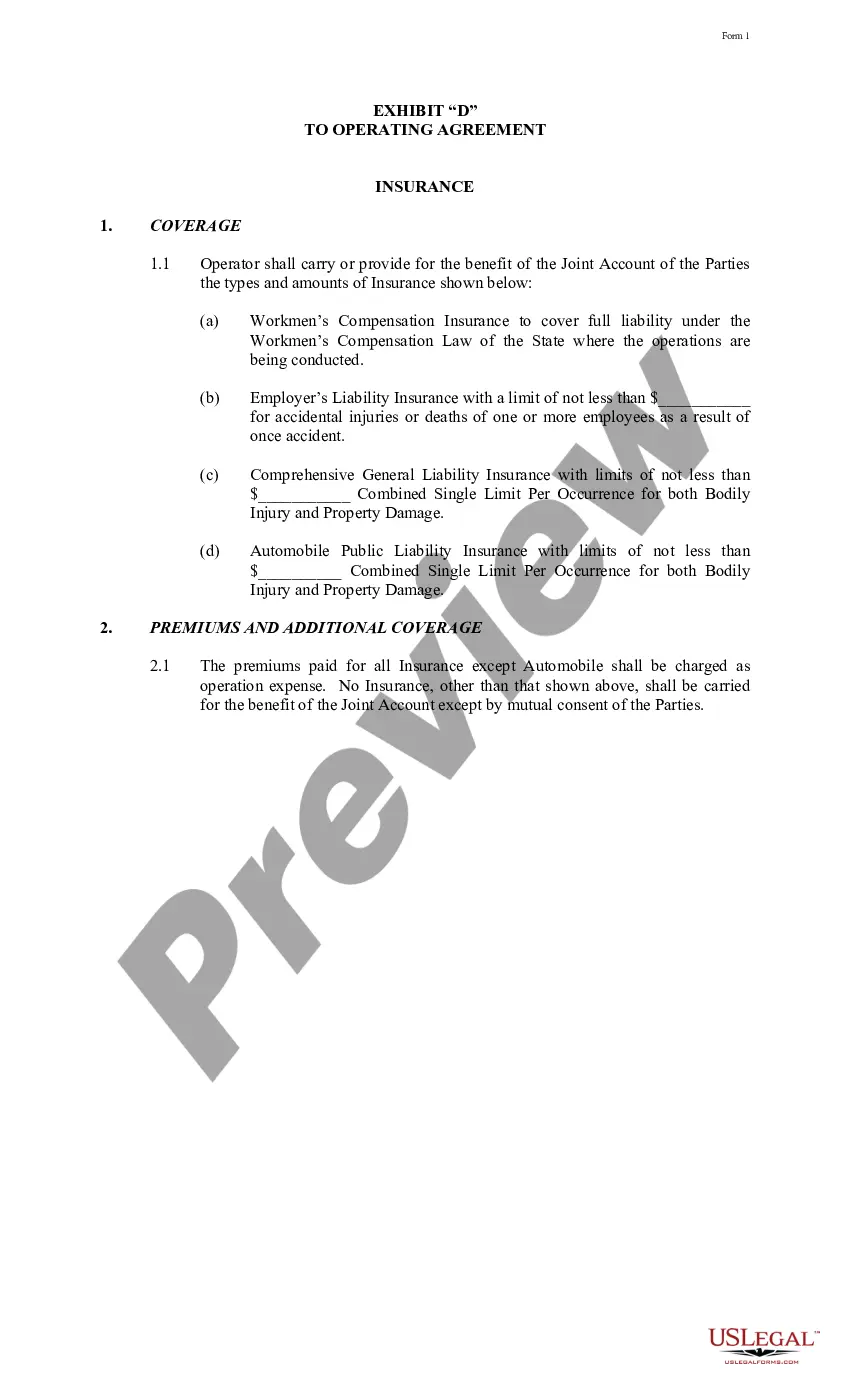

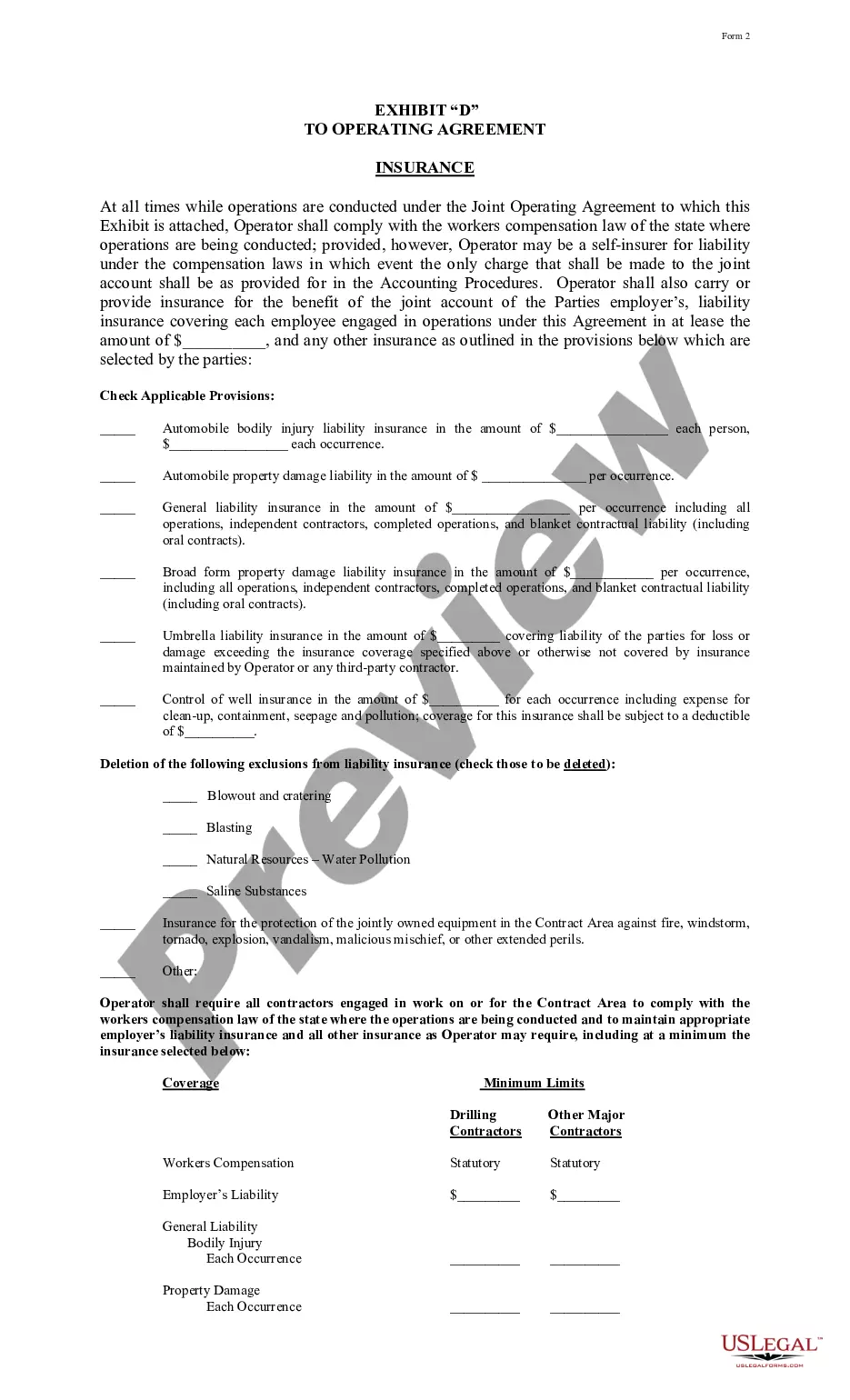

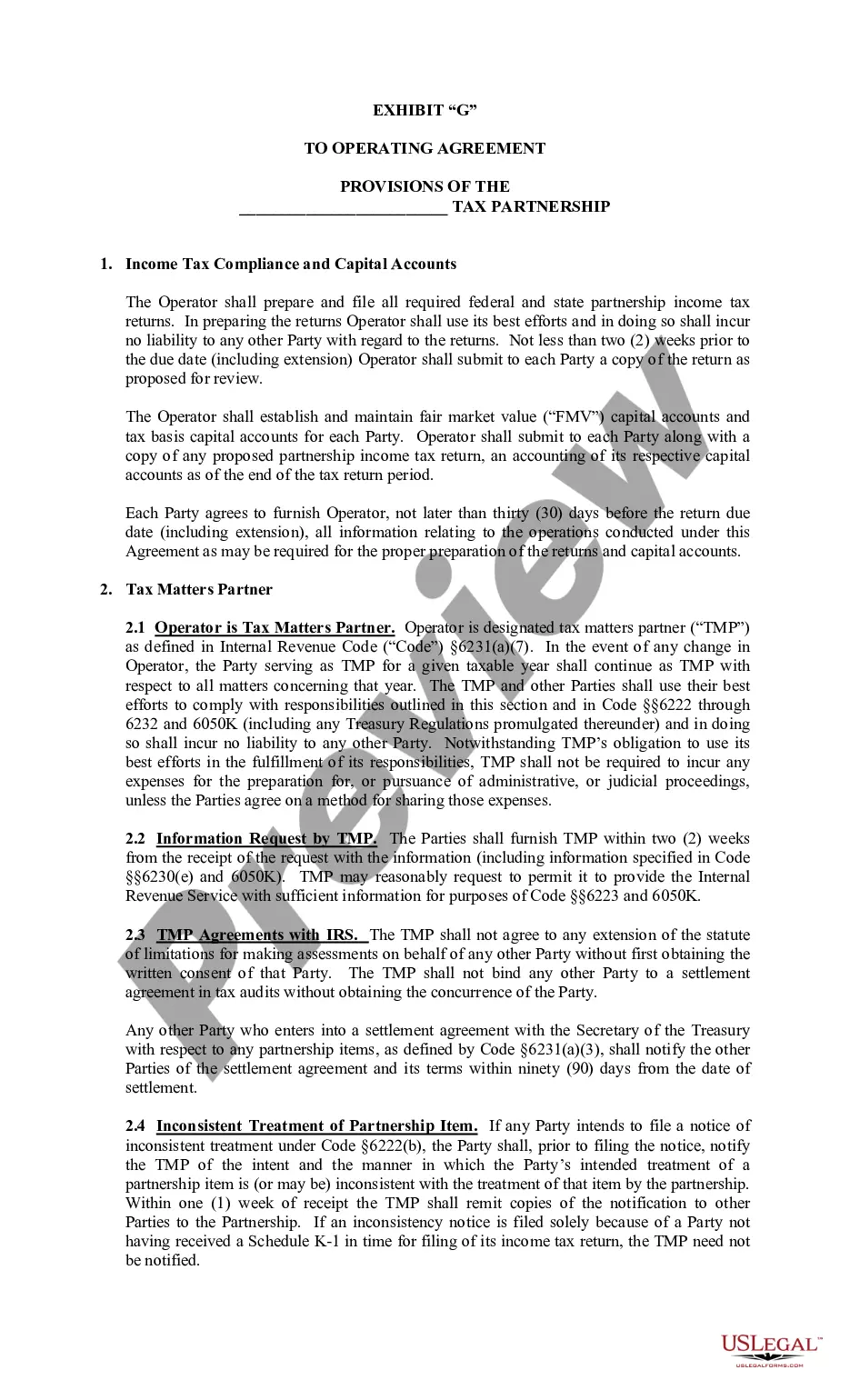

Montana Exhibit C Accounting Procedure Joint Operations

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Exhibit C Accounting Procedure Joint Operations?

Finding the right legitimate record design could be a have difficulties. Obviously, there are a lot of layouts available on the Internet, but how would you discover the legitimate develop you will need? Make use of the US Legal Forms website. The assistance offers thousands of layouts, including the Montana Exhibit C Accounting Procedure Joint Operations, that can be used for enterprise and personal requirements. All the types are examined by pros and meet up with state and federal demands.

Should you be previously authorized, log in in your profile and then click the Down load switch to get the Montana Exhibit C Accounting Procedure Joint Operations. Make use of your profile to check through the legitimate types you may have acquired in the past. Proceed to the My Forms tab of your respective profile and acquire another duplicate from the record you will need.

Should you be a new user of US Legal Forms, listed here are basic recommendations for you to comply with:

- First, be sure you have selected the appropriate develop for the metropolis/state. You may examine the form using the Preview switch and browse the form outline to make certain it is the right one for you.

- In the event the develop fails to meet up with your expectations, utilize the Seach industry to get the right develop.

- Once you are positive that the form would work, click the Purchase now switch to get the develop.

- Pick the costs program you want and type in the necessary details. Build your profile and pay money for an order making use of your PayPal profile or charge card.

- Choose the submit formatting and download the legitimate record design in your gadget.

- Total, revise and print and sign the received Montana Exhibit C Accounting Procedure Joint Operations.

US Legal Forms will be the biggest catalogue of legitimate types in which you will find different record layouts. Make use of the company to download expertly-manufactured paperwork that comply with status demands.

Form popularity

FAQ

In response to the SEC's Accounting Series Release No. 4, the American Institute of Accountants () reorganized its Committee on Accounting Procedure (CAP) in 1939 and increased it from 8 to 22 members, all accounting practitioners except for three academicians.

Committee on Accounting Procedure (CAP) 1938-1959 a. CAP was one of the committees of America Institute of Accountants (AICPA now). After the 1929 stock market crash, the government wanted to better regulate and protect the market with new accounting standards so they assigned this task to SEC.

The CAP decided early on that formulating a statement of broad principles would take too long and instead approached issues on a case-by-case basis. Without a framework and often without adequate research, the CAP relied on the members' collective experience for agreement on member-suggested solutions.

A fund is defined as a fiscal and accounting entity with a self-balancing set of accounts recording cash and other financial resources, together with all related liabilities and residual equities or balances, and changes therein, which are segregated for the purpose of carrying on specific activities or attaining ...

The Committee on Accounting Procedure (CAP) was the first private sector organization tasked with setting accounting standards in the United States. But its Accounting Research Bulletins never had binding authority.

Achievements of the Committee on Accounting Procedure (CAP) comprised bulletins which provided solutions to instant issues that arose and decreased the scope of alternative practices. The Committee, however, failed to present a well-defined and systemized body of accounting principlesthat wereneeded.