The Truth-in-Lending Act (TILA) is part of the Federal Consumer Credit Protection Act. The purpose of the TILA is to make full disclosure to debtors of what they are being charged for the credit they are receiving. The Act merely asks lenders to be honest to the debtors and not cover up what they are paying for the credit. Regulation Z is a federal regulation prepared by the Federal Reserve Board to carry out the details of the Act. TILA applies to consumer credit transactions. Consumer credit is credit for personal or household use and not commercial use.

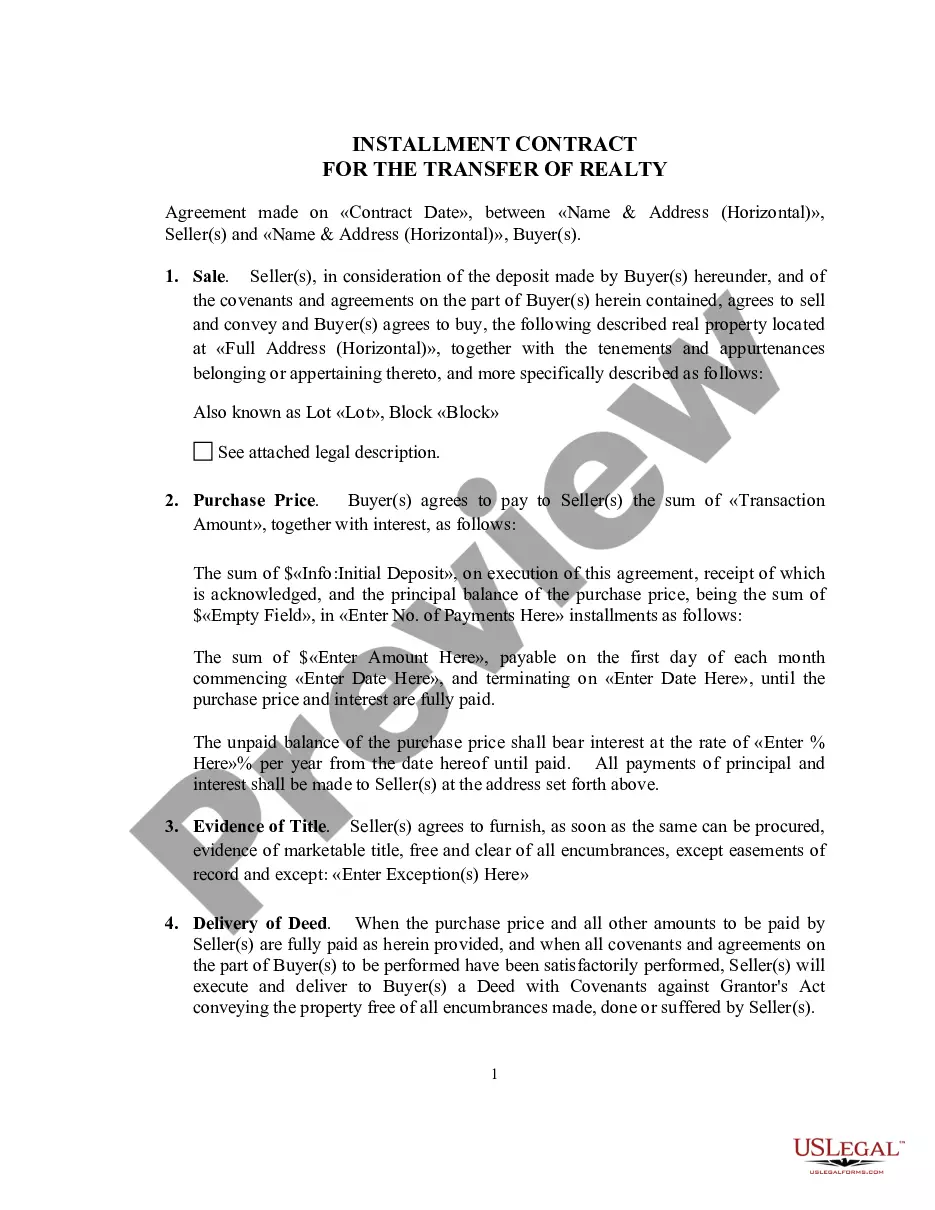

Closed-end transactions involve a fixed amount to be paid back over a period of time such as a note or a retail installment contract.

Montana General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures

Category:

State:

Multi-State

Control #:

US-02514BG

Format:

Word;

PDF;

Rich Text

Instant download

Description

Free preview

How to fill out General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures?

If you need to finalize, acquire, or print licensed document templates, utilize US Legal Forms, the premier compilation of legal forms, accessible online.

Utilize the site’s straightforward and convenient search to find the documents you need.

A selection of templates for business and personal purposes are organized by categories and requests, or keywords.

Step 4. Once you locate the form you need, click the Get now button. Choose the payment plan you prefer and enter your details to sign up for an account.

Step 5. Complete the transaction. You can use your Visa or Mastercard or PayPal account to finalize the payment. Step 6. Select the format of the legal form and download it to your device.

- Utilize US Legal Forms to acquire the Montana General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures with just a few clicks.

- If you are already a US Legal Forms user, sign in to your account and click the Download button to obtain the Montana General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures.

- You can also access forms you previously downloaded within the My documents section of your account.

- If you are using US Legal Forms for the first time, follow the steps below.

- Step 1. Confirm you have selected the form for the correct city/country.

- Step 2. Use the Preview option to review the form's content. Be sure to read the summary.

- Step 3. If you are unsatisfied with the form, use the Search field at the top of the screen to find other types of the legal form format.

Form popularity

FAQ

The retail installment contract disclosures provide essential information about the terms and costs associated with the agreement. These disclosures are part of the Montana General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures and include details on interest rates, total costs, and payment schedules. By reviewing these disclosures, buyers can ensure they are fully informed. Resources from uslegalforms can assist in navigating these critical details.

Generally, a retail installment contract is not classified as a security. Instead, it is a financing agreement that details the payment process for goods purchased on credit, as defined in the Montana General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures. Understanding the distinctions between securities and retail installment contracts is essential for consumers. Utilizing resources like uslegalforms can simplify this understanding.

Yes, a buyer can get out of an installment contract under certain circumstances. Legal provisions allow for cancellation if the seller fails to meet obligations outlined in the Montana General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures. However, it is crucial to understand any potential penalties or fees that may apply. Consulting with a legal professional or using platforms like uslegalforms can provide guidance on the process.

The Truth in Lending Act mandates several key disclosures to protect consumers. These include the annual percentage rate (APR), total finance charges, total payments, and payment schedule. Each disclosure aids in promoting transparency for borrowers engaged in credit transactions. Familiarizing yourself with the Montana General Disclosures Required By The Federal Truth In Lending Act - Retail Installment Contract - Closed End Disclosures is essential to ensure you are informed throughout the lending process.

Regulation Z also requires mortgage lenders to provide borrowers with a written disclosure of rates, fees and other finance charges. Plus, if you have an adjustable-rate mortgage, they're required to let you know in advance if your rate will be changing.

Federal regulations require the disclosure of all relevant financial information by publicly-listed companies. In addition to financial data, companies are required to reveal their analysis of their strengths, weaknesses, opportunities, and threats.

The value of a closed-end credit APR must be disclosed as a single rate only, whether the loan has a single interest rate, a variable interest rate, a discounted variable interest rate, or graduated payments based on separate interest rates (step rates), and it must appear with the segregated disclosures.

Regulation Z also requires mortgage lenders to provide borrowers with a written disclosure of rates, fees and other finance charges. Plus, if you have an adjustable-rate mortgage, they're required to let you know in advance if your rate will be changing.

inLending Disclosure Statement provides information about the costs of your credit. Effective October 3, 2015, for most kinds of mortgage loans a form called the Loan Estimate replaced the initial TruthinLending disclosure, and a Closing Disclosure replaced the final TruthinLending disclosure.

In any closed-end credit transaction, TILA requires disclosure of the total finance charge, which is the sum of all charges, expressed as a dollar amount, that meet the regulatory definition of finance charge.