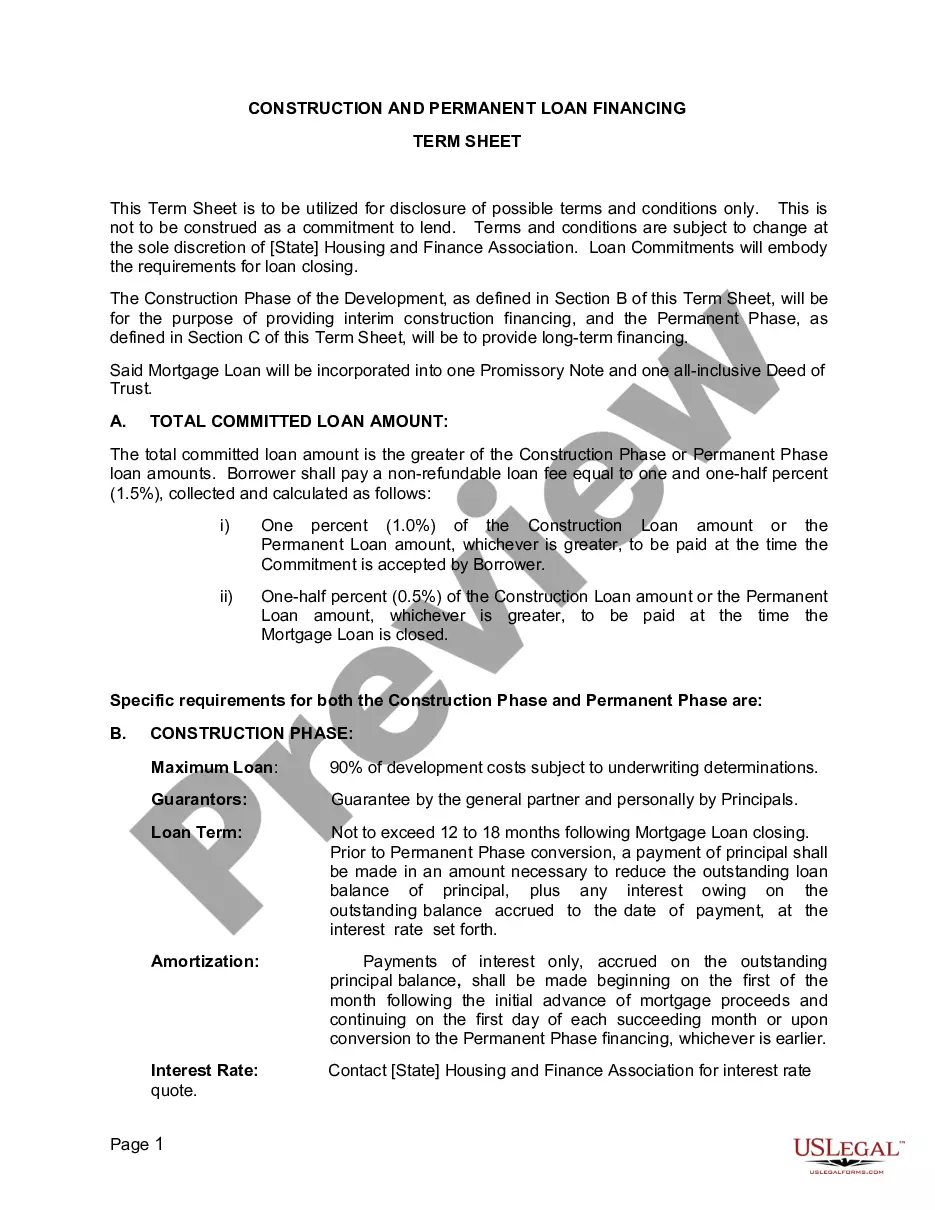

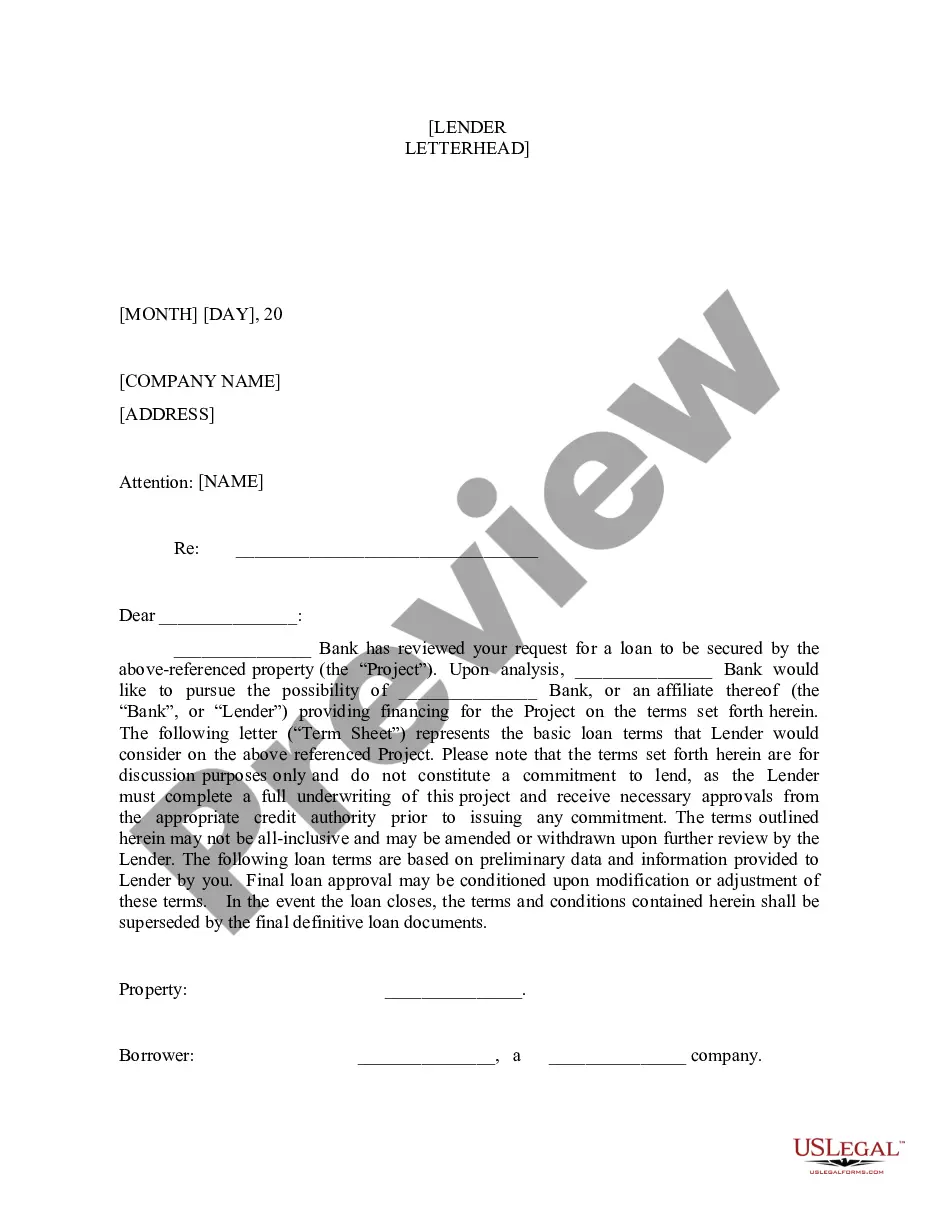

Mississippi Construction Loan Financing Term Sheet

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Construction Loan Financing Term Sheet?

If you have to comprehensive, obtain, or print legal record themes, use US Legal Forms, the biggest collection of legal types, that can be found on the web. Use the site`s easy and hassle-free search to get the papers you require. Numerous themes for enterprise and person uses are categorized by groups and suggests, or keywords and phrases. Use US Legal Forms to get the Mississippi Construction Loan Financing Term Sheet with a handful of clicks.

In case you are currently a US Legal Forms customer, log in for your bank account and click on the Download option to find the Mississippi Construction Loan Financing Term Sheet. You can even entry types you formerly acquired in the My Forms tab of the bank account.

If you are using US Legal Forms initially, refer to the instructions beneath:

- Step 1. Be sure you have chosen the shape for the correct area/country.

- Step 2. Take advantage of the Review option to look over the form`s articles. Never overlook to read through the information.

- Step 3. In case you are unsatisfied with all the develop, use the Lookup industry at the top of the monitor to locate other versions of the legal develop template.

- Step 4. Once you have found the shape you require, select the Get now option. Select the rates plan you like and add your accreditations to sign up on an bank account.

- Step 5. Approach the financial transaction. You can use your charge card or PayPal bank account to accomplish the financial transaction.

- Step 6. Choose the formatting of the legal develop and obtain it on the product.

- Step 7. Full, edit and print or indication the Mississippi Construction Loan Financing Term Sheet.

Every single legal record template you purchase is the one you have permanently. You might have acces to every single develop you acquired in your acccount. Go through the My Forms portion and select a develop to print or obtain once again.

Compete and obtain, and print the Mississippi Construction Loan Financing Term Sheet with US Legal Forms. There are thousands of skilled and condition-particular types you can utilize for your enterprise or person requirements.

Form popularity

FAQ

As mentioned, construction loans are short-term loans, usually no longer than a year in length. On the other hand, traditional mortgages are long-term loans, with terms typically ranging from 15 ? 30 years.

This includes the term, loan size, interest rate, and other financial matters common to debt. Risk mitigation preferences. The lender will often require specific conditions be met or specific information be provided on a recurring, timely manner.

Step 1: Multiply the loan amount by the Avg. % Outstanding to calculate the average loan balance for the entirety of the construction term: $1,500,000 * 50% = $750,000. Step 3: Divide the annual interest by 12 to get the average monthly interest payment: $30,000/12 = $2,500.

In general, construction loans have higher interest rates than longer-term mortgage loans used to purchase homes. The money borrowed through a construction loan is typically provided in a series of advances as the construction progresses.

Cons to doing a construction loan would be that payments on the construction loan begin once funds start being disbursed to the builder. With a traditional mortgage, payments don't begin until settlement. Another con is that the interest rates on construction loans are typically higher than on traditional mortgages.

Unlike traditional mortgages, which carry fixed rates, construction loans usually have variable rates that fluctuate with the prime rate. That means your monthly payment can also change, moving upward or downward based on rate changes. Construction loan rates are also typically higher than traditional mortgage rates.

Construction loans are usually taken out by builders or a homebuyer custom-building their own home. They are short-term loans, usually for a period of only one year.

Assuming that you're making the standard FHA down payment of 3.5 percent, the minimum credit score for a construction loan is 580. Otherwise, you can apply for a new construction FHA loan with a credit score as low as 500, but in that case, you'll need to make a 10 percent down payment.