Missouri Assignment of Accounts Receivable

Description

How to fill out Assignment Of Accounts Receivable?

US Legal Forms - one of the largest collections of legal documents in the United States - provides a variety of legal document templates that you can download or print.

By using the website, you can access thousands of forms for business and personal purposes, organized by categories, states, or keywords. You can find the most recent documents, such as the Missouri Assignment of Accounts Receivable, in moments.

If you have a monthly subscription, Log In to download the Missouri Assignment of Accounts Receivable from the US Legal Forms library. The Download button will appear on every form you view. You can access all your previously saved forms in the My documents tab of your account.

Process the purchase. Use your Visa or Mastercard or PayPal account to complete the transaction.

Choose the format and download the form to your device.

- Make sure you have selected the correct form for your city/county.

- Click the Preview button to review the form's content.

- Check the form details to ensure you have chosen the right one.

- If the form does not meet your requirements, use the Search field at the top of the screen to find one that does.

- If you are satisfied with the form, confirm your selection by clicking the Buy now button.

- Then, select the pricing plan you prefer and provide your credentials to register for an account.

Form popularity

FAQ

The accounts receivable process involves tracking and managing customer invoices until payment is received. Initially, businesses issue invoices to customers for products or services rendered. After sending the invoices, the business monitors payments and follows up as necessary. Understanding the Missouri Assignment of Accounts Receivable can enhance your management of unpaid bills.

In the assignment of receivables, various elements come into play, including the agreement terms, the rights transferred, and any associated fees. This process typically outlines how and when payments are expected, as well as the responsibilities of both parties. Businesses in Missouri can utilize platforms like uslegalforms to ensure they have the necessary documentation and compliance for their assignment of accounts receivable.

In Missouri, the statute of limitations on a promissory note is generally five years. This means that a creditor has five years to bring a legal claim for the repayment of the note. Understanding this timeframe is crucial for businesses, particularly when dealing with Missouri Assignment of Accounts Receivable, as it affects their ability to collect owed amounts.

Factoring involves selling accounts receivable to a third party at a discount, while assignment of accounts receivable may simply transfer the receivable to another entity without the same level of discount. Essentially, factoring provides immediate funds based on the value of the receivables, whereas assignment may involve a more straightforward transfer of the debt owed. Understanding these distinctions helps businesses in Missouri make informed financial decisions.

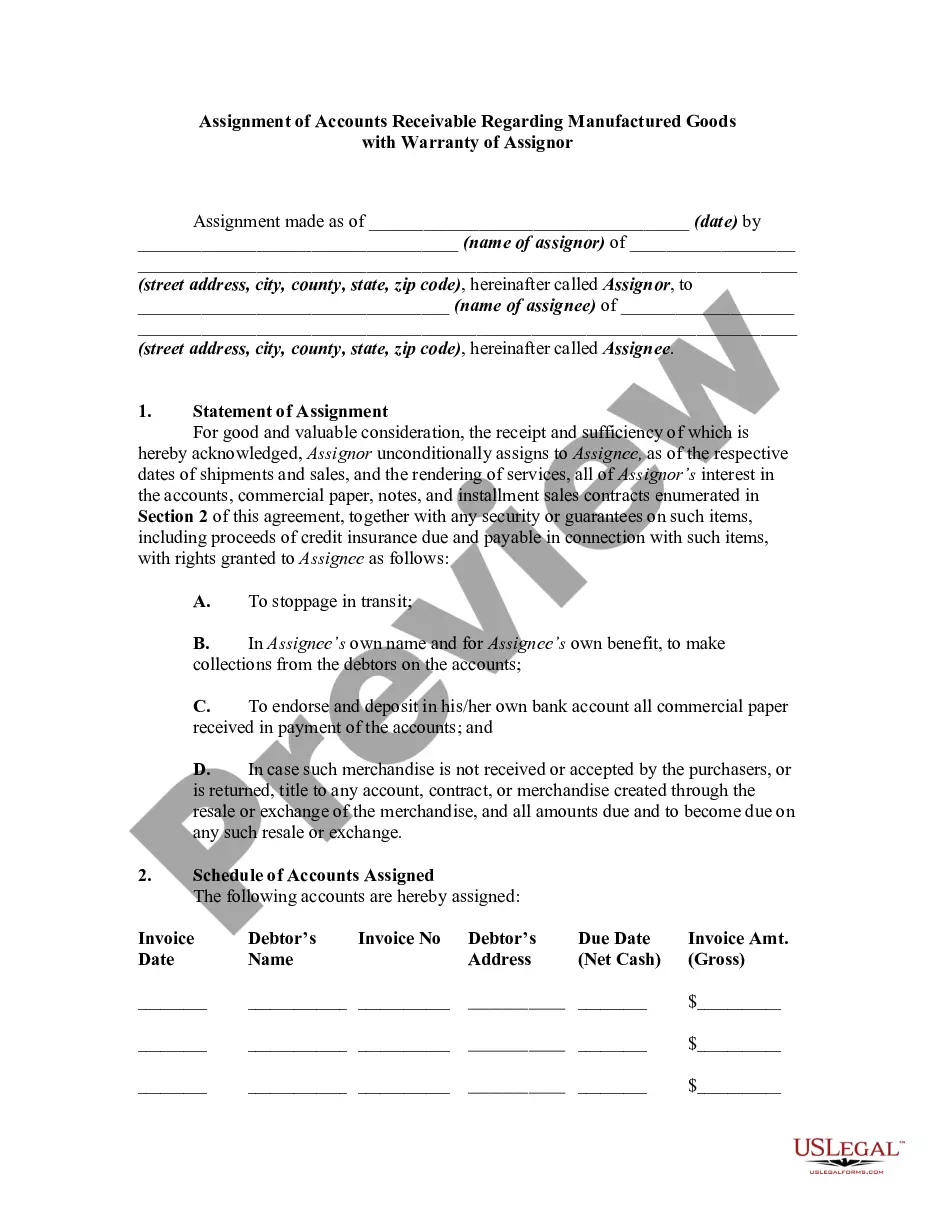

What is the Assignment of Accounts Receivable? Under an assignment of accounts receivable arrangement, a lender pays a borrower in exchange for the borrower assigning certain of its receivable accounts to the lender. If the borrower does not repay the loan, the lender has the right to collect the assigned receivables.

The purpose of assigning accounts receivable is to provide collateral in order to obtain a loan. To illustrate, let's assume that a corporation receives a special order from a new customer whose credit rating is superb. However, the customer pays for its purchases 90 days after it receives the goods.

Follow these tips to ensure efficient and effective accounts receivable management.Use Electronic Billing & Payment.Outline Clear Billing Procedures.Set Credit & Collection Policies and Stick to Them.Be Proactive.Set up Automations.Make It Easy for Customers.Use the Right KPIs.Involve All Teams in the Process.06-May-2021

Pledging, or assigning, accounts receivable means that you essentially use your accounts receivable as collateral to obtain cash. The lender has the receivables as security, but you, as the business owner, are still responsible for the collection of the debts from your credit customers.

Assignment of accounts receivable is a lending agreement whereby the borrower assigns accounts receivable to the lending institution. In exchange for this assignment of accounts receivable, the borrower receives a loan for a percentage, which could be as high as 100%, of the accounts receivable.

Pledging, or assigning, accounts receivable means that you essentially use your accounts receivable as collateral to obtain cash. The lender has the receivables as security, but you, as the business owner, are still responsible for the collection of the debts from your credit customers.