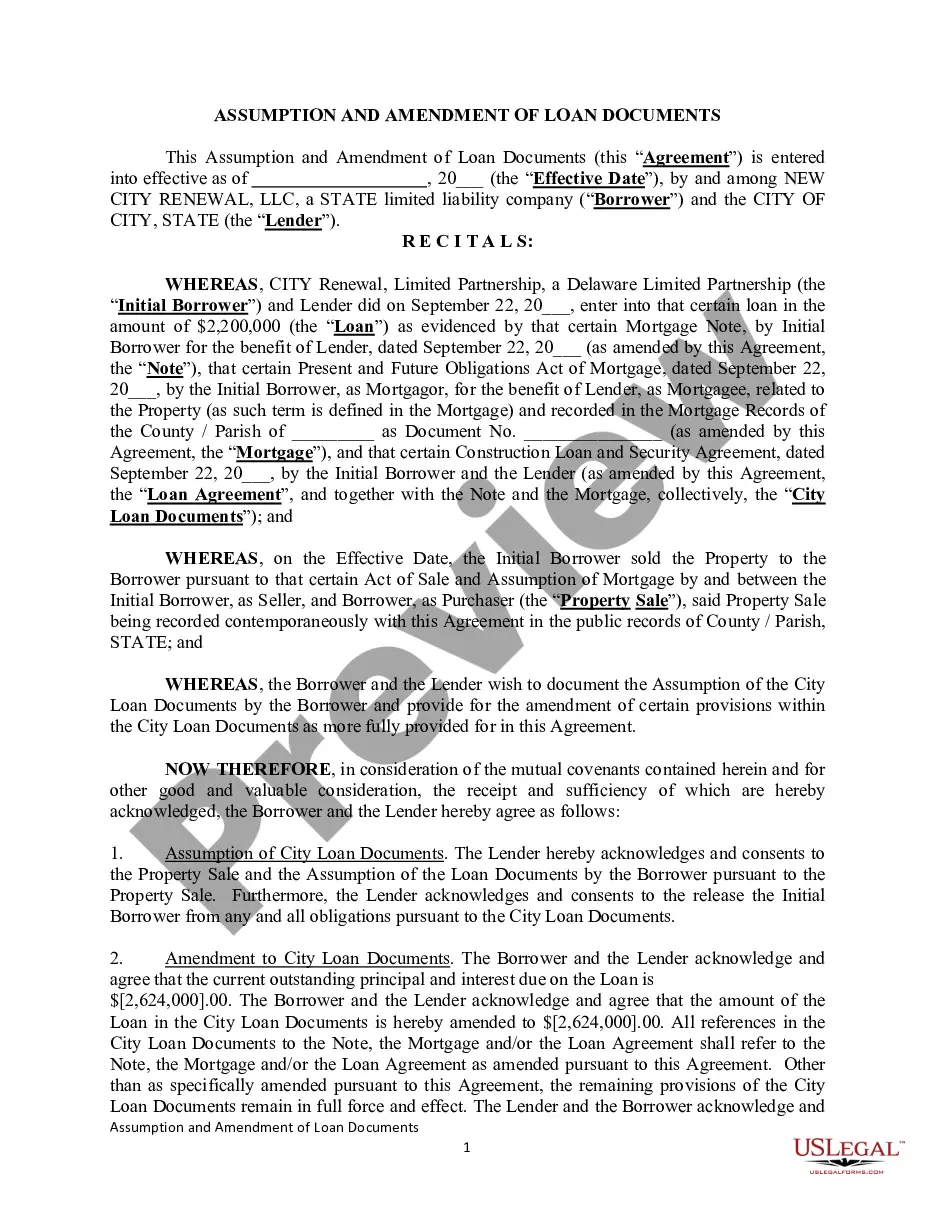

This form is an Assumption Agreement. The form provides that the grantee will assume a lien on property described in the agreement. The assumption will become effective on the date provided in the agreement.

Missouri Assumption Agreement of Loan Payments

Category:

State:

Multi-State

Control #:

US-00424

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Assumption Agreement Of Loan Payments?

You may invest numerous hours online looking for the legal document template that meets the state and federal standards you require. US Legal Forms provides thousands of legal forms that are reviewed by experts.

It is easy to obtain or print the Missouri Assumption Agreement of Loan Payments from my service. If you already have a US Legal Forms account, you can Log In and click the Acquire button. After that, you can complete, modify, print, or sign the Missouri Assumption Agreement of Loan Payments. Every legal document template you obtain is yours indefinitely.

To get another copy of any downloaded form, visit the My documents section and click the appropriate button. If this is your first time using the US Legal Forms website, follow the simple instructions below: First, ensure you have selected the correct document template for the county/city of your choice. Review the form details to make certain you have chosen the accurate document. If available, use the Review button to look through the document template as well.

Utilize professional and state-specific templates to address your business or personal needs.

- If you wish to find another version of the document, use the Search field to locate the template that suits your needs and specifications.

- Once you have discovered the template you desire, click Get now to proceed.

- Select the payment plan you prefer, enter your credentials, and create an account on US Legal Forms.

- Complete the payment. You may utilize your Visa or Mastercard or PayPal account to pay for the legal document.

- Choose the format of the document and download it to your device.

- Make modifications to your document if needed. You can complete, edit, sign, and print the Missouri Assumption Agreement of Loan Payments.

- Download and print thousands of document templates using the US Legal Forms site, which offers the largest collection of legal forms.

Form popularity

FAQ

In Missouri, assumption agreements themselves are usually not recorded in public land records. However, it is crucial to keep a copy of the Missouri Assumption Agreement of Loan Payments for your records. This agreement serves as proof of the terms agreed upon between the involved parties. If you want to ensure that your agreement is properly structured, US Legal Forms offers templates that can help streamline the process.

Typically, the assumption of a mortgage is not recorded in the same way that a property deed is. However, the Missouri Assumption Agreement of Loan Payments should be documented to ensure all parties have a clear understanding of their obligations. While the mortgage lender might not officially record the assumption, having a written agreement protects your rights and clarifies responsibilities. For complete peace of mind, you can consult US Legal Forms to access templates and guidance.

Yes, Missouri Assumption Agreements of Loan Payments are legally binding contracts. When you enter into an assumption agreement, both parties agree to the terms laid out, which can include payment schedules and obligations. It is essential to understand that once signed, this agreement holds legal weight, and both parties must adhere to its conditions. If you need assistance with drafting or reviewing such agreements, consider using US Legal Forms for reliable resources.

The purpose of an assumption agreement is to legally transfer the responsibility of a loan from one borrower to another. This allows the new borrower to take over the payments and obligations associated with the loan, as outlined in a Missouri Assumption Agreement of Loan Payments. This agreement protects the lender's interests and ensures clarity for all parties involved.

An assumption agreement template is a structured document that provides a framework for creating an assumption agreement. This template generally includes sections for borrower information, loan details, and terms of the assumption. Utilizing an assumption agreement template can simplify the process and ensure you include all necessary elements for a Missouri Assumption Agreement of Loan Payments.

A loan assumption is documented through a formal agreement signed by both the original borrower and the new borrower. The Missouri Assumption Agreement of Loan Payments will detail the terms of the assumption, including payment obligations and any necessary approvals from the lender. Proper documentation is essential to ensure that all parties are on the same page and legally protected.

A loan assumption agreement template is a pre-formatted document that outlines the terms and conditions under which a borrower can assume a loan. This template typically includes details like the loan amount, interest rate, payment schedule, and the responsibilities of both parties. Using a template can streamline the process of creating a Missouri Assumption Agreement of Loan Payments.

While it is not mandatory to hire a lawyer for a Missouri Assumption Agreement of Loan Payments, having legal guidance can be beneficial. A lawyer can help you understand the terms of the agreement and ensure that all necessary documents are in order. This can provide peace of mind and protect your interests during the process.

For a Missouri Assumption Agreement of Loan Payments, you'll typically need the original loan agreement, a request for assumption, and any required credit documentation. Lenders may also require a formal application to assess the new borrower's creditworthiness. It's wise to check with your lender for any additional specific documents they may need.