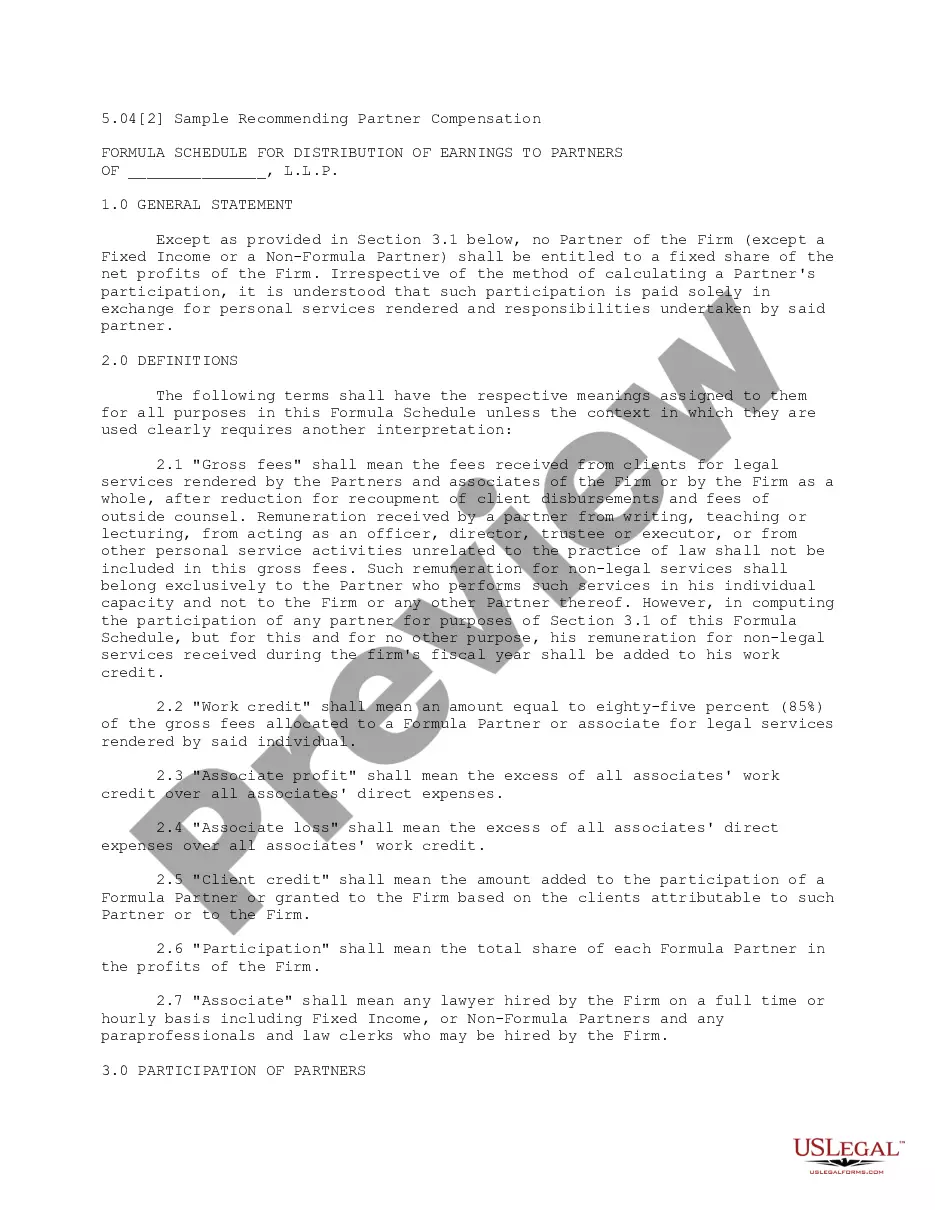

This Formula System for Distribution of Earnings to Partners provides a list of provisions to conside when making partner distribution recommendations. Some of the factors to consider are: Collections on each partner's matters, acquisition and development of new clients, profitablity of matters worked on, training of associates and paralegals, contributions to the firm's marketing practices, and others.

Minnesota Formula System for Distribution of Earnings to Partners

Category:

State:

Multi-State

Control #:

US-L05041A

Format:

Word;

PDF;

Rich Text

Instant download

Description

Free preview

How to fill out Formula System For Distribution Of Earnings To Partners?

Discovering the right legitimate document web template can be a battle. Of course, there are plenty of themes available on the net, but how will you find the legitimate type you require? Make use of the US Legal Forms site. The support gives 1000s of themes, including the Minnesota Formula System for Distribution of Earnings to Partners, that can be used for organization and personal requirements. Each of the forms are checked out by experts and fulfill state and federal needs.

Should you be already registered, log in for your account and click the Down load button to obtain the Minnesota Formula System for Distribution of Earnings to Partners. Make use of your account to search throughout the legitimate forms you possess bought formerly. Proceed to the My Forms tab of your account and get yet another version from the document you require.

Should you be a whole new user of US Legal Forms, listed below are simple guidelines for you to stick to:

- Very first, make certain you have chosen the proper type for your area/region. You can look over the form making use of the Preview button and browse the form information to make certain this is the right one for you.

- If the type does not fulfill your needs, make use of the Seach field to obtain the correct type.

- When you are positive that the form is suitable, click on the Purchase now button to obtain the type.

- Opt for the costs program you want and enter the essential info. Make your account and pay for an order making use of your PayPal account or Visa or Mastercard.

- Pick the submit format and obtain the legitimate document web template for your system.

- Complete, modify and print out and sign the obtained Minnesota Formula System for Distribution of Earnings to Partners.

US Legal Forms is the greatest local library of legitimate forms that you can find a variety of document themes. Make use of the service to obtain professionally-produced files that stick to condition needs.

Form popularity

FAQ

Each partner reports their share of the partnership's income or loss on their personal tax return. Partners are not employees and shouldn't be issued a Form W-2. The partnership must furnish copies of Schedule K-1 (Form 1065) to the partner. For deadlines, see About Form 1065, U.S. Return of Partnership Income.

The net income for a partnership is divided between the partners as called for in the partnership agreement. The income summary account is closed to the respective partner capital accounts. The respective drawings accounts are closed to the partner capital accounts.

Partnership accounting is the same as accounting for a proprietorship except there are separate capital and drawing accounts for each partner. The fundamental accounting equation (Assets = Liabilities + Owner's Equity) remains unchanged except that total owners' equity is the sum of the partners' capital accounts.

Partnerships are considered pass-through entities. That means that any income or losses are passed through the partnership to the individual owners, who are then responsible to account for that income or loss on their income tax returns.

A partnership that has taxable Minnesota gross income must file Form M3, Partnership Return, if it's required to file one of the following federal tax forms: Form 1065, U.S. Return of Partnership Income. Form 1065-B, U.S. Return of Income for Electing Large Partnerships.

If the partnership had income, debit the income section for its balance and credit each partner's capital account based on his or her share of the income. If the partnership realized a loss, credit the income section and debit each partner's capital account based on his or her share of the loss.

This means that the partnership itself is not subject to tax: any profits are instead taxable on the partners. Generally, for tax purposes each partner is treated as receiving their share of the income and expenses of the partnership as they arise.

The partnership or S corporation must withhold 9.85% of a nonresident individual's Minnesota income, less any allowable credits that are passed through to the individual.