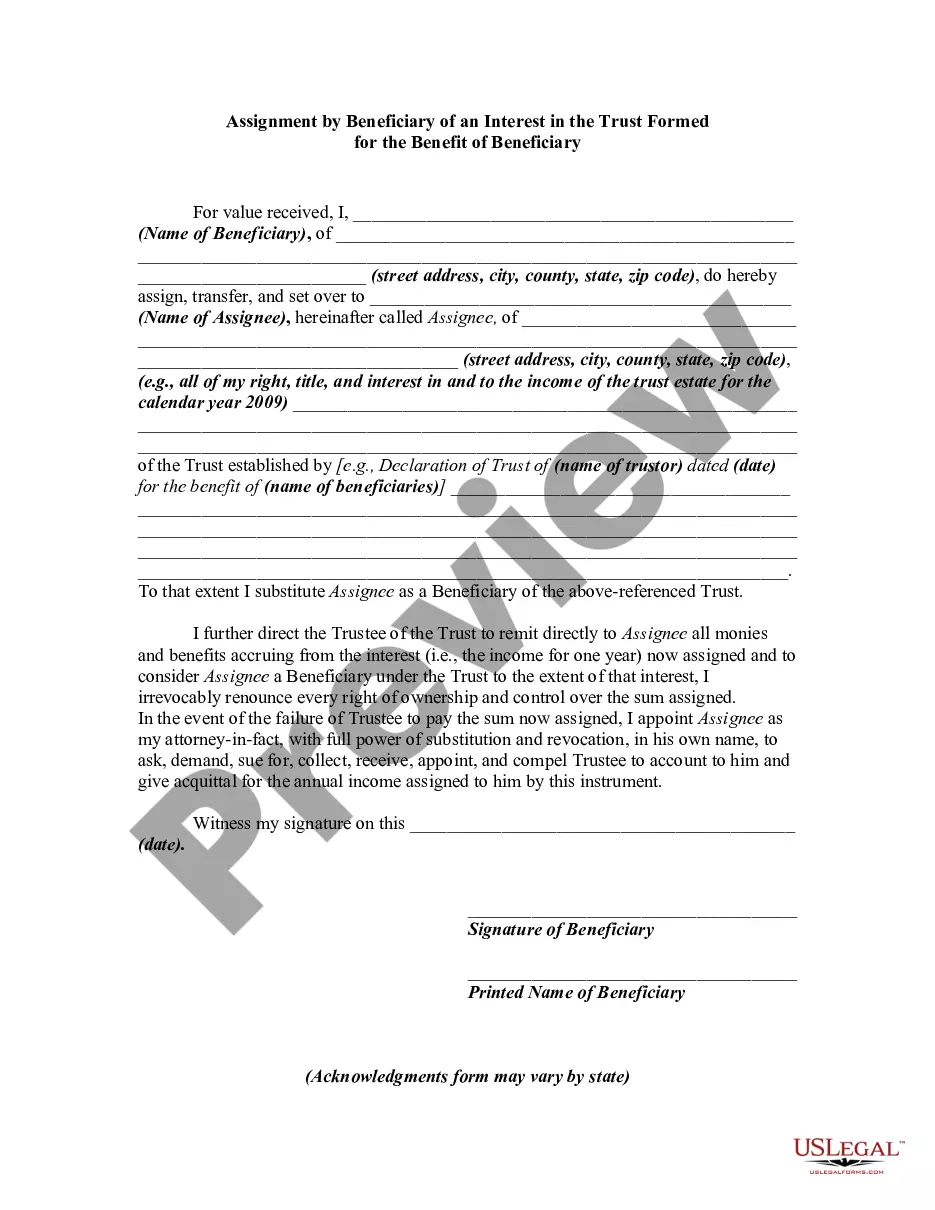

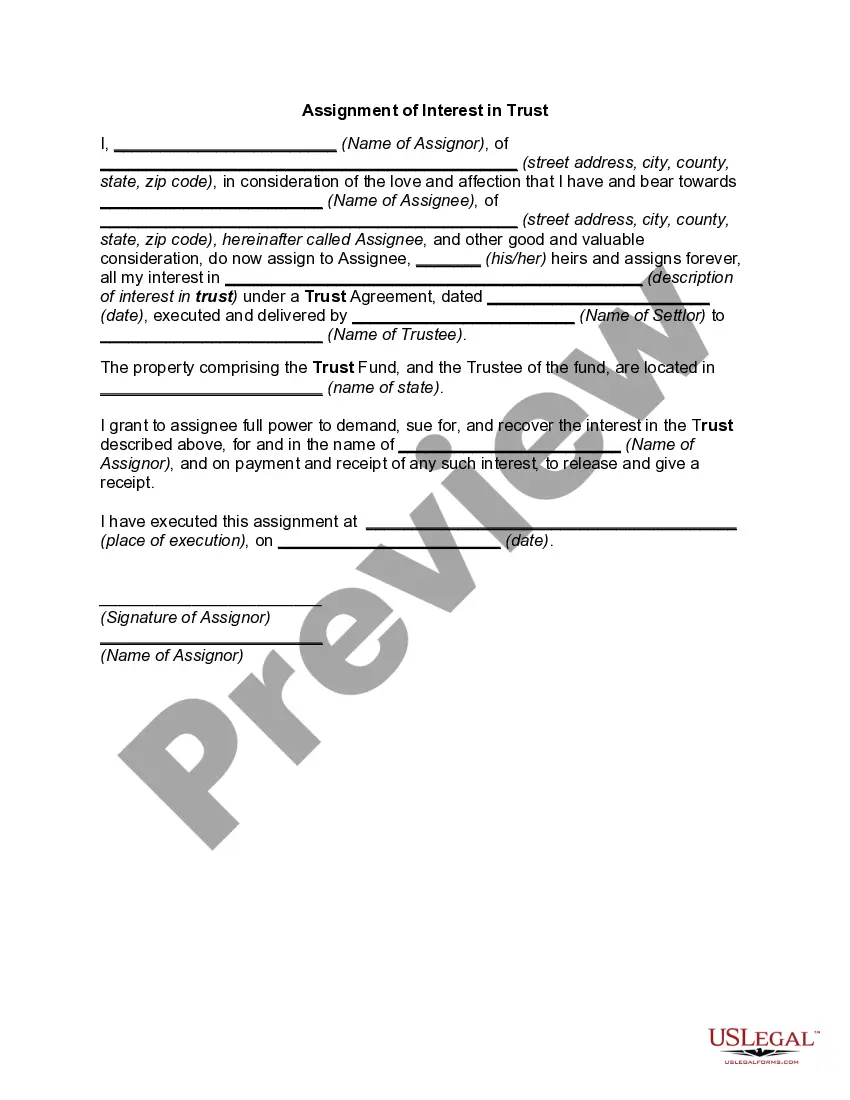

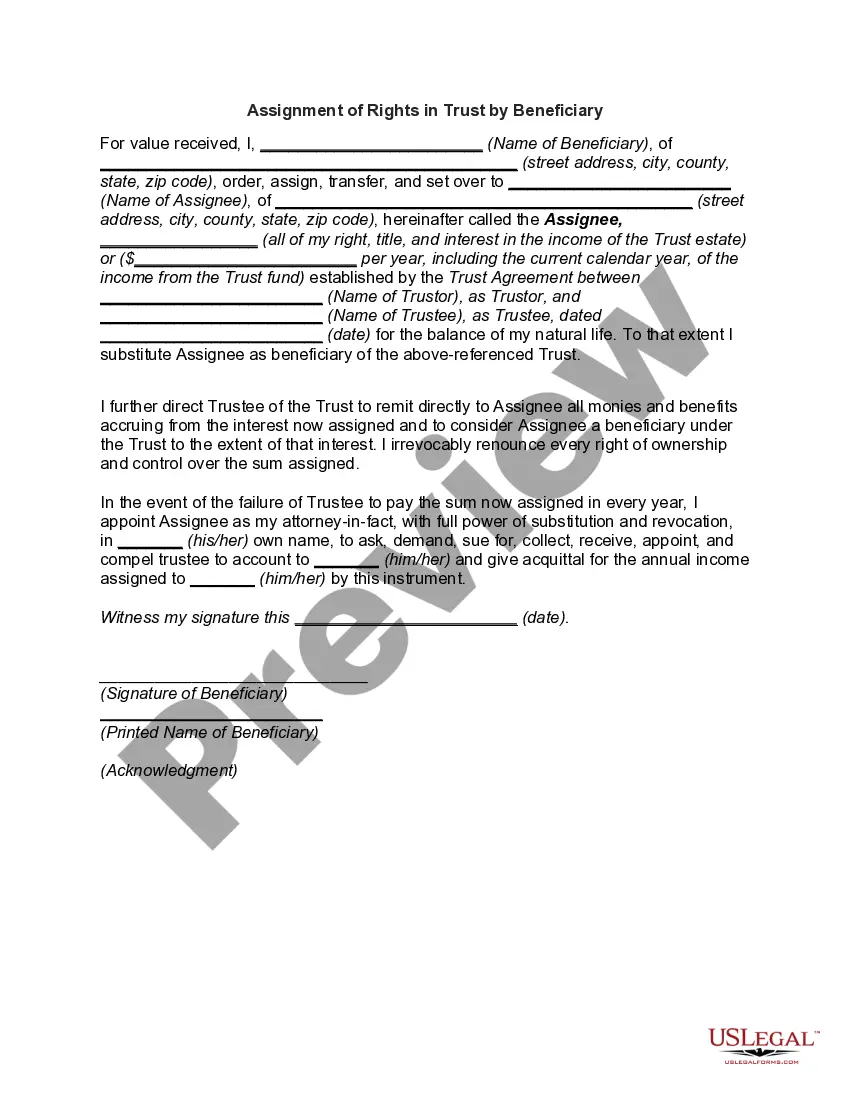

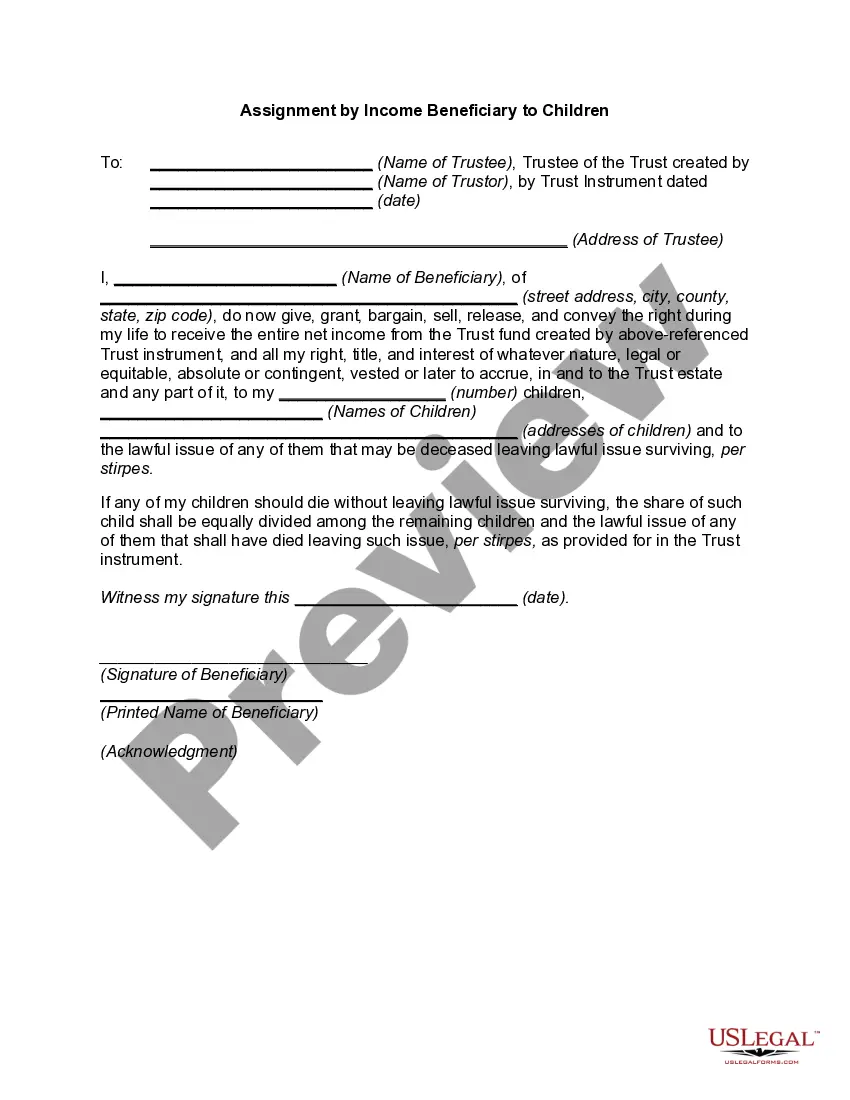

An assignment by a beneficiary of a portion of his or her interest in a trust is usually regarded as a transfer of a right, title, or estate in property rather than a chose in action (like an account receivable). As a general rule, the essentials of such an assignment or transfer are the same as those for any transfer of real or personal property. This form is a generic example that may be referred to when preparing such a form for your particular state. It is for illustrative purposes only. Local laws should be consulted to determine any specific requirements for such a form in a particular jurisdiction.

Minnesota Assignment by Beneficiary of a Percentage of the Income of a Trust

Instant download

Description

Free preview

How to fill out Assignment By Beneficiary Of A Percentage Of The Income Of A Trust?

You might spend numerous hours online looking for the authentic document template that fulfills the state and federal requirements you have.

US Legal Forms offers thousands of authentic forms that are reviewed by experts.

You can either acquire or generate the Minnesota Assignment by Beneficiary of a Percentage of the Income of a Trust through my services.

If available, use the Review button to look through the document template as well. If you want to find another version of the form, utilize the Search field to locate the template that suits your needs and requirements. Once you have located the template you desire, click Purchase now to proceed. Choose the pricing plan you prefer, enter your details, and register for a free account on US Legal Forms. Complete the transaction. You can use your credit card or PayPal account to pay for the legitimate document. Select the format of the document and download it to your device. Make changes to the document if necessary. You can complete, modify, sign, and generate the Minnesota Assignment by Beneficiary of a Percentage of the Income of a Trust. Obtain and create thousands of document templates using the US Legal Forms website, which provides the largest selection of legitimate forms. Utilize professional and state-specific templates to address your business or personal needs.

- If you already possess a US Legal Forms account, you can Log In and then click the Acquire button.

- Following that, you can complete, modify, generate, or sign the Minnesota Assignment by Beneficiary of a Percentage of the Income of a Trust.

- Each authentic document template you acquire is yours forever.

- To obtain another copy of the purchased form, visit the My documents tab and click the corresponding button.

- If you are visiting the US Legal Forms website for the first time, follow the straightforward instructions below.

- First, ensure that you have selected the correct document template for your region/area of interest.

- Review the form information to verify that you have chosen the appropriate template.

Form popularity

FAQ

Yes, beneficiaries in Minnesota have the right to request access to the trust document and relevant information. This access allows beneficiaries to understand how the trust operates and what they may expect in terms of distributions. If you are engaging in a Minnesota Assignment by Beneficiary of a Percentage of the Income of a Trust, you should feel confident in asserting your right to review the trust details.

In Minnesota, trust beneficiaries have the right to receive information about the trust, including annual accountings and details about distributions. Beneficiaries can request a copy of the trust document to understand their rights and benefits. If you're involved in a Minnesota Assignment by Beneficiary of a Percentage of the Income of a Trust, knowing your rights can empower you to make informed decisions regarding your inheritance.

To obtain proof of a trust, you typically need a copy of the trust document itself. This document outlines the terms, beneficiaries, and trustee information. If you require verification for a Minnesota Assignment by Beneficiary of a Percentage of the Income of a Trust, you may need to request this document from the trustee. Additionally, understanding the specifics of your trust can help you navigate this process more effectively.

The distribution of income from a trust involves allocating earnings generated by the trust's assets to the beneficiaries. This distribution can depend on the trust's terms and the type of trust established. It's crucial to understand how these distributions work, especially if you’re exploring a Minnesota Assignment by Beneficiary of a Percentage of the Income of a Trust. Consulting with a financial advisor can help clarify your specific situation.

In Minnesota, trusts are generally not recorded like property deeds. Instead, a trust exists as a private agreement among the involved parties. However, it's important to maintain proper documentation regarding the trust's assets and distributions. If you're considering a Minnesota Assignment by Beneficiary of a Percentage of the Income of a Trust, make sure to consult legal advice to ensure all records are accurately kept.

To allocate trust income effectively, determine the percentage of income designated for each beneficiary. In instances where beneficiaries have set agreements, such as a Minnesota Assignment by Beneficiary of a Percentage of the Income of a Trust, these percentages can reflect specific financial needs or desires. It's crucial to document these allocations formally to avoid any disputes in the future. Using platforms like uslegalforms can help ensure that your trust documents clearly outline these allocations, providing peace of mind to both the grantor and beneficiaries.

To report a beneficiary's income from a trust, you typically need to collect relevant documents such as the trust's financial statements and Schedule K-1. The Minnesota Assignment by Beneficiary of a Percentage of the Income of a Trust allows beneficiaries to manage their income shares. Ensure you file the necessary forms with the IRS and state tax authorities to properly report this income. If you need assistance, the US Legal Forms platform provides detailed resources to guide you through the reporting process.

In Minnesota, beneficiaries generally have the right to request a copy of the trust document. This right allows beneficiaries to understand their entitlements and the terms of the trust. The Minnesota Assignment by Beneficiary of a Percentage of the Income of a Trust may specify what information beneficiaries have access to. It is beneficial for beneficiaries to communicate with the trustee or legal representative for transparency.

Yes, income from a trust is typically taxable to the beneficiary receiving it. Beneficiaries must report trust income on their tax returns for the year they receive it. The Minnesota Assignment by Beneficiary of a Percentage of the Income of a Trust provides an essential framework for understanding how this income is treated tax-wise. Consulting with a tax advisor can help beneficiaries navigate their tax responsibilities.

Beneficiary income of a trust refers to the earnings generated by trust assets that are distributed to named beneficiaries. This income can come from interest, dividends, or any gains realized from the trust's investments. Understanding the concept of Minnesota Assignment by Beneficiary of a Percentage of the Income of a Trust can clarify how this income is defined and distributed. It is advisable to review the trust document to grasp the specifics.