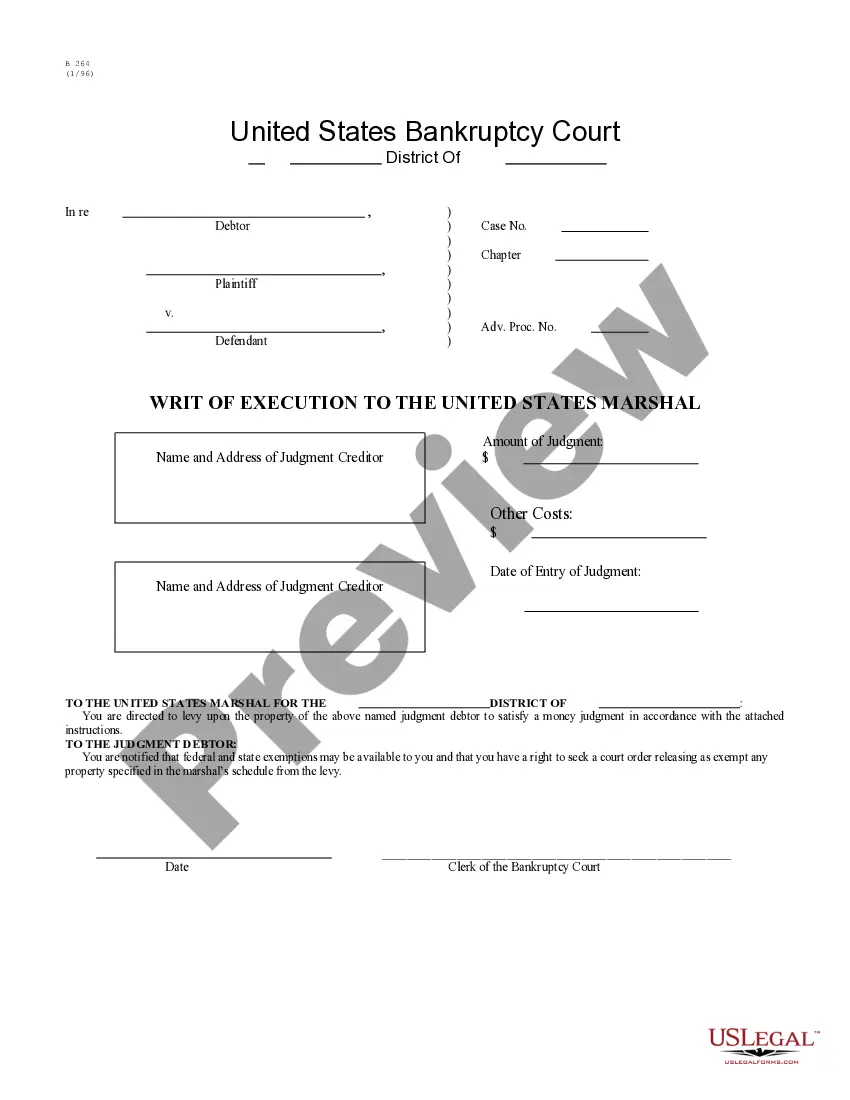

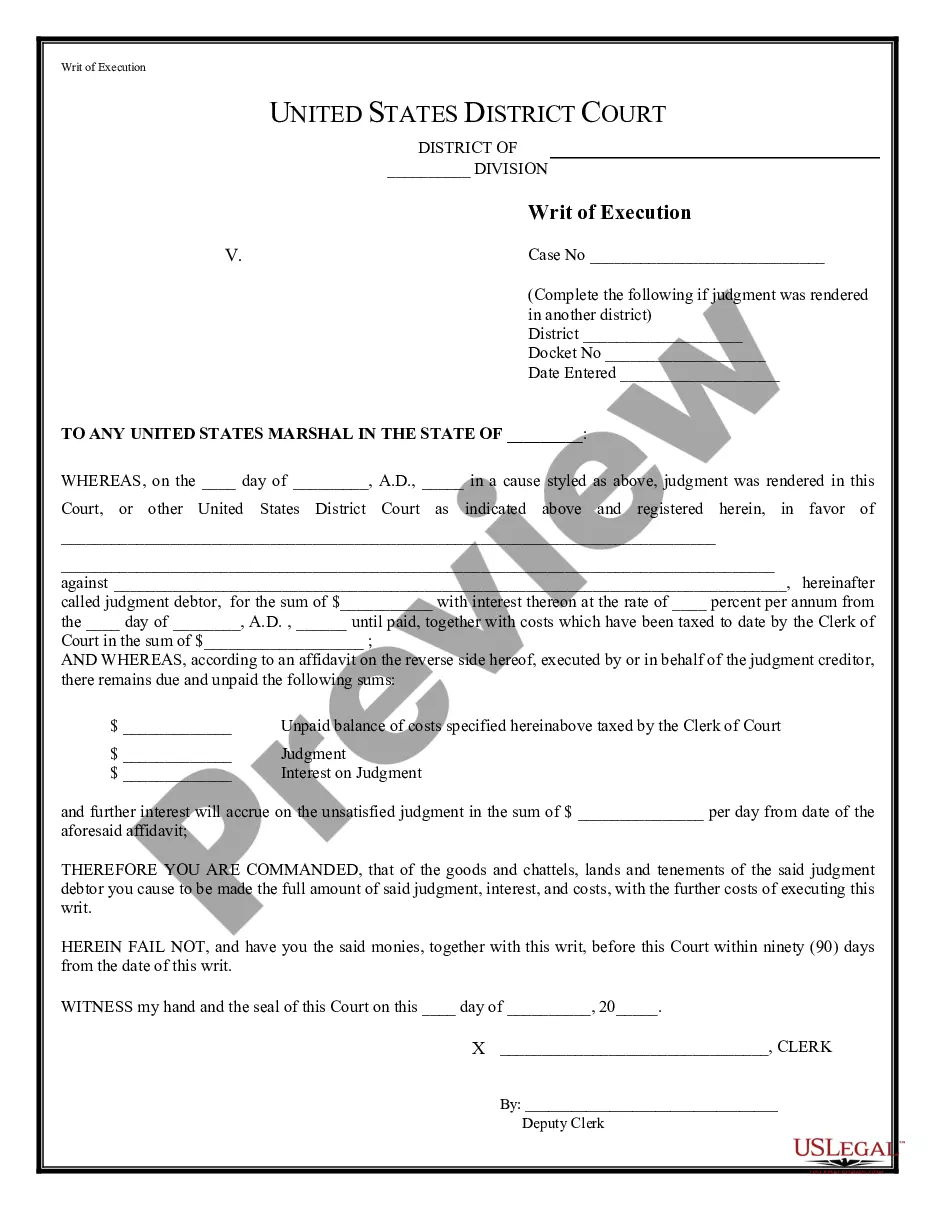

This form is a Suggestion for a Writ of Garnishment. Plaintiff obtained a judgment against defendant and in the process of collection, the plaintiff requests that garnishment be placed on the property of the defendant to satisfy the judgment. Therefore, the court orders that a writ of garnishment be granted in favor of plaintiff.

Wisconsin Suggestion for Writ of Garnishment

State:

Multi-State

Control #:

US-00987

Format:

Word;

Rich Text

Instant download

Description

Free preview

Form popularity

FAQ

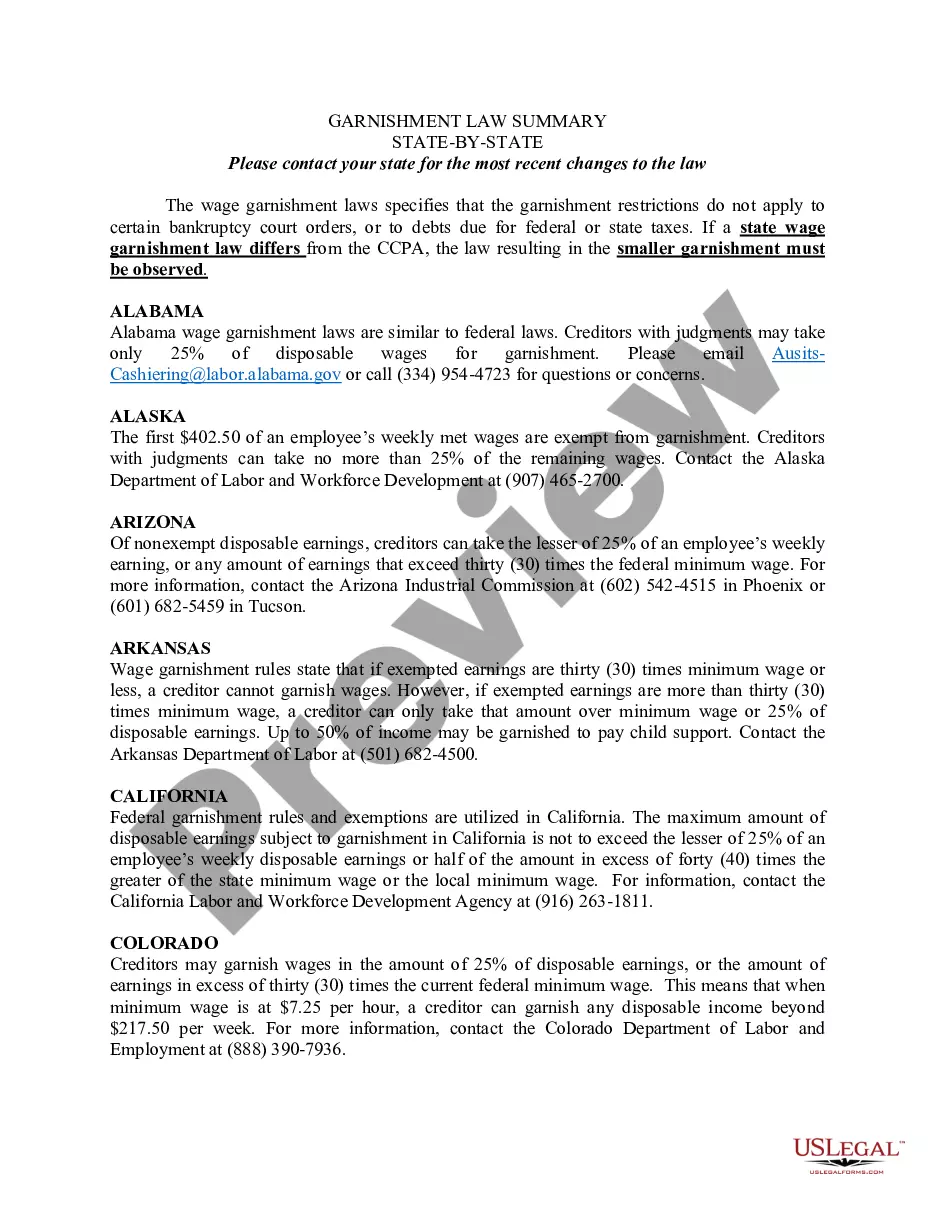

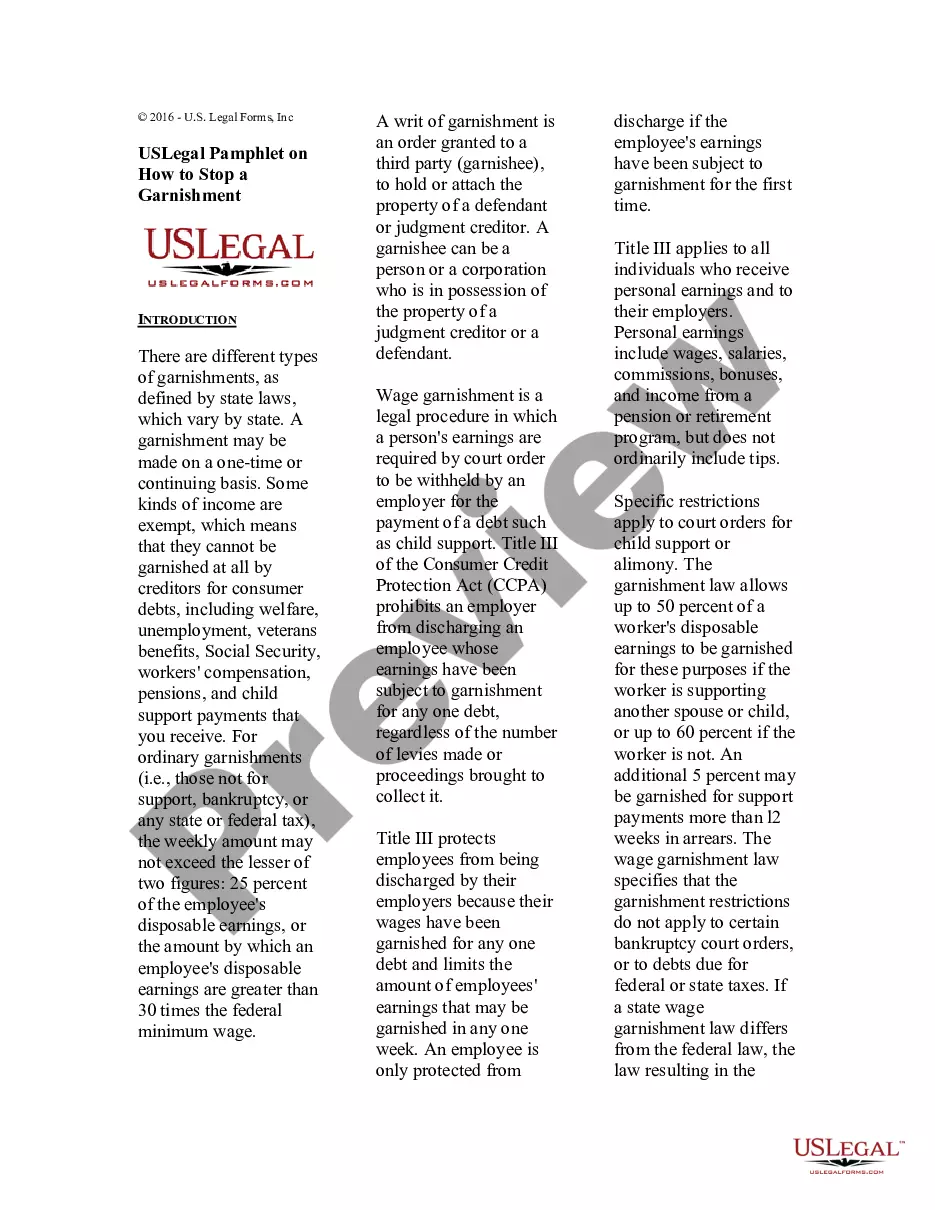

Collect evidence showing how detrimental the wage garnishment is to your financial stability or how you qualify for an exemption. In either case, the creditor may agree to a solution that doesn't involve a garnishment, such as an adjustment payment plan or a settlement for a lump sum.

(1) The creditor shall pay a $15 fee to the garnishee for each earnings garnishment or each stipulated extension of that earnings garnishment. This fee shall be included as a cost in the creditor's claim in the earnings garnishment.

By law, you are entitled to an exemption of not less than 80% of your disposable earnings. Your "disposable earnings" are those remaining after social security and federal and state income taxes are withheld.

Legal options available to stop or reduce wage garnishment include objecting to the garnishment order, filing a claim of exemption, negotiating a repayment plan with your creditor, or filing for bankruptcy. This article will discuss these options.

If your judgment has not been completely paid at the end of the 13 weeks and you wish to continue garnishing the debtor's wages, you may file and pay for a new garnishment action. Another option is for you and the debtor to agree in writing to extend the garnishment for another 13-week period.

By law, you are entitled to an exemption of not less than 80% of your disposable earnings. Your "disposable earnings" are those remaining after social security and federal and state income taxes are withheld.

Under Wisconsin law, most creditors can garnish the lesser of (subject to some exceptions?more below): 20% of your disposable earnings, or. the amount by which your disposable earnings exceed 30 times the federal minimum wage.

Act quickly to prevent wage garnishment You can file a Claim of Exemption any time after wage garnishment has started, but you'll only get wages back from the time after you submit the claim. If you act quickly, you can stop it before it even starts. By law, your employer cannot fire you for a single wage garnishment.