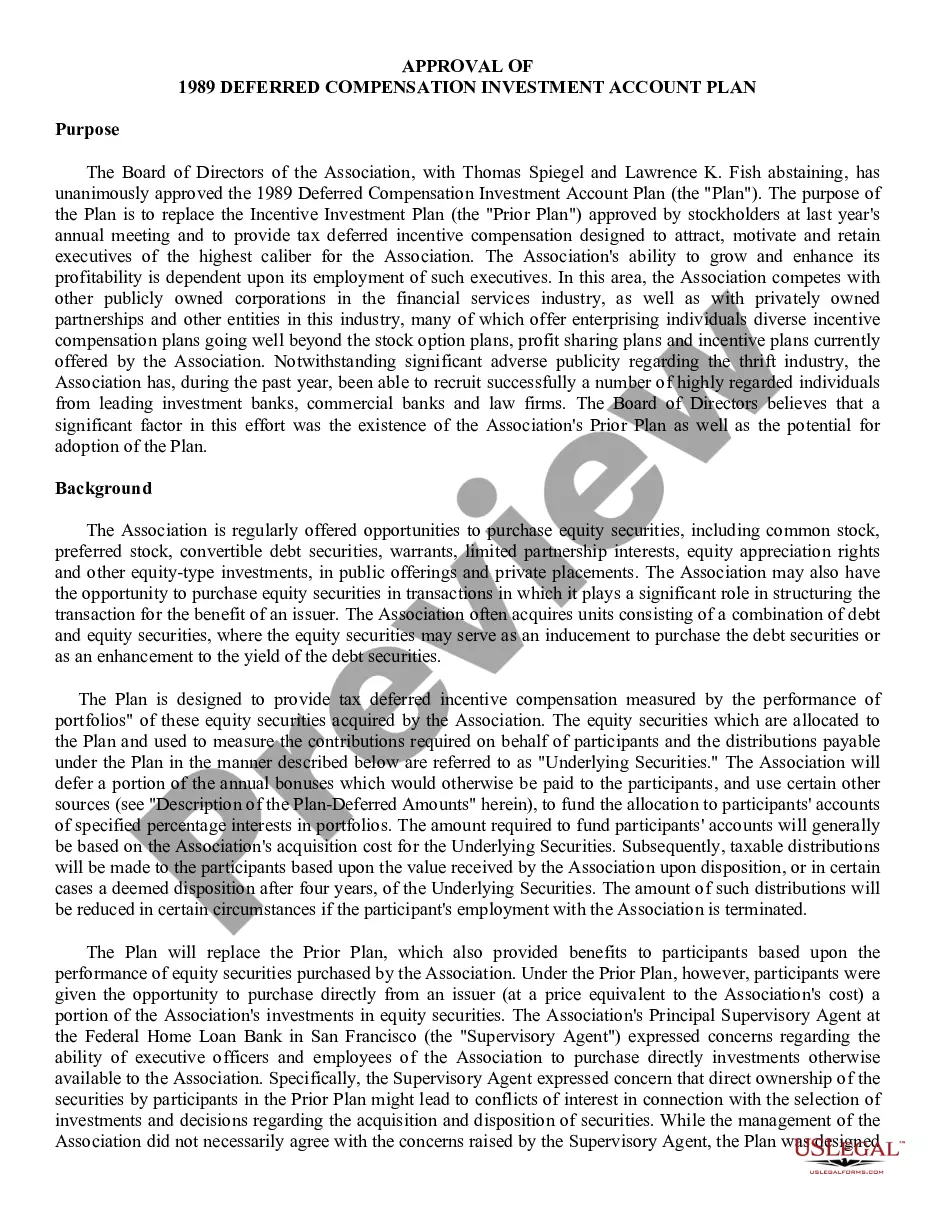

20-146 20-146 . . . Deferred Compensation Investment Account Plan under which Board of Directors of Savings and Loan Association allocates a portion of annual bonuses which would otherwise be paid to selected officers and employees to a separate account. The deferred compensation in such account is deemed, for purposes of Plan only, to represent specified percentages of Association's investments in certain portfolios of equity securities, and it is increased or decreased to same extent as performance of such securities

Maine Deferred Compensation Investment Account Plan

State:

Multi-State

Control #:

US-CC-20-146

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Deferred Compensation Investment Account Plan?

Choosing the right legitimate record design can be quite a have a problem. Of course, there are a lot of layouts accessible on the Internet, but how do you find the legitimate develop you want? Utilize the US Legal Forms web site. The service gives a large number of layouts, for example the Maine Deferred Compensation Investment Account Plan, which you can use for enterprise and personal needs. All the kinds are examined by pros and satisfy state and federal specifications.

If you are previously signed up, log in for your profile and click on the Down load key to have the Maine Deferred Compensation Investment Account Plan. Make use of your profile to look from the legitimate kinds you possess bought in the past. Check out the My Forms tab of your profile and get one more copy from the record you want.

If you are a brand new user of US Legal Forms, listed here are basic instructions for you to stick to:

- First, ensure you have chosen the right develop for your area/county. You are able to examine the shape using the Review key and read the shape information to make certain it will be the right one for you.

- If the develop does not satisfy your requirements, utilize the Seach field to discover the proper develop.

- When you are certain that the shape is proper, click on the Buy now key to have the develop.

- Select the pricing program you desire and enter in the required details. Create your profile and pay for the transaction with your PayPal profile or charge card.

- Opt for the submit structure and obtain the legitimate record design for your system.

- Comprehensive, modify and print out and signal the obtained Maine Deferred Compensation Investment Account Plan.

US Legal Forms is the largest catalogue of legitimate kinds that you can find different record layouts. Utilize the service to obtain appropriately-made papers that stick to status specifications.

Form popularity

FAQ

The 457 plan is a retirement savings plan and you generally cannot withdraw money while you are still employed. When you leave employment, you may withdraw funds; leave them in place; transfer them to a 457, 403(b) or 401(k) of a new employer; or roll them into an Individual Retirement Account (IRA).

457(b) Assets can be withdrawn without penalty at any age upon separation from service from the plan sponsor, or age 70½ if still working.

Investing your deferred compensation Your plan might offer you several options for the benchmark?often, major stock and bond indexes, the 10-year US Treasury note, the company's stock price, or the mutual fund choices in the company 401(k) plan.

Deferred compensation has the potential to increase capital gains over time when offered as an investment account or a stock option. Rather than simply receiving the amount that was initially deferred, a 401(k) and other deferred compensation plans can increase in value before retirement.

The 457 plan is an IRS-sanctioned, tax-advantaged employee retirement plan. The plan is offered only to public service employees and employees at tax-exempt organizations. Participants are allowed to contribute up to 100% of their salaries up to a dollar limit for the year.

You can take penalty-free withdrawals from your 457 account at any age after you leave your job. Most other types of retirement-savings plans assess a 10% penalty if you withdraw money before age 55 or 59½, depending on when you leave your job.

You can take out small or large sums anytime, or you can set up automatic, periodic payments. If your plan allows it, you may be able to have direct deposit which allows for fast transfer of funds. Unlike a check, direct deposit typically doesn't include a hold on the funds from your account.

You can request a loan by logging in to your DCP account, completing a Loan Application Form, or calling the Service Center at 844-523-2457.