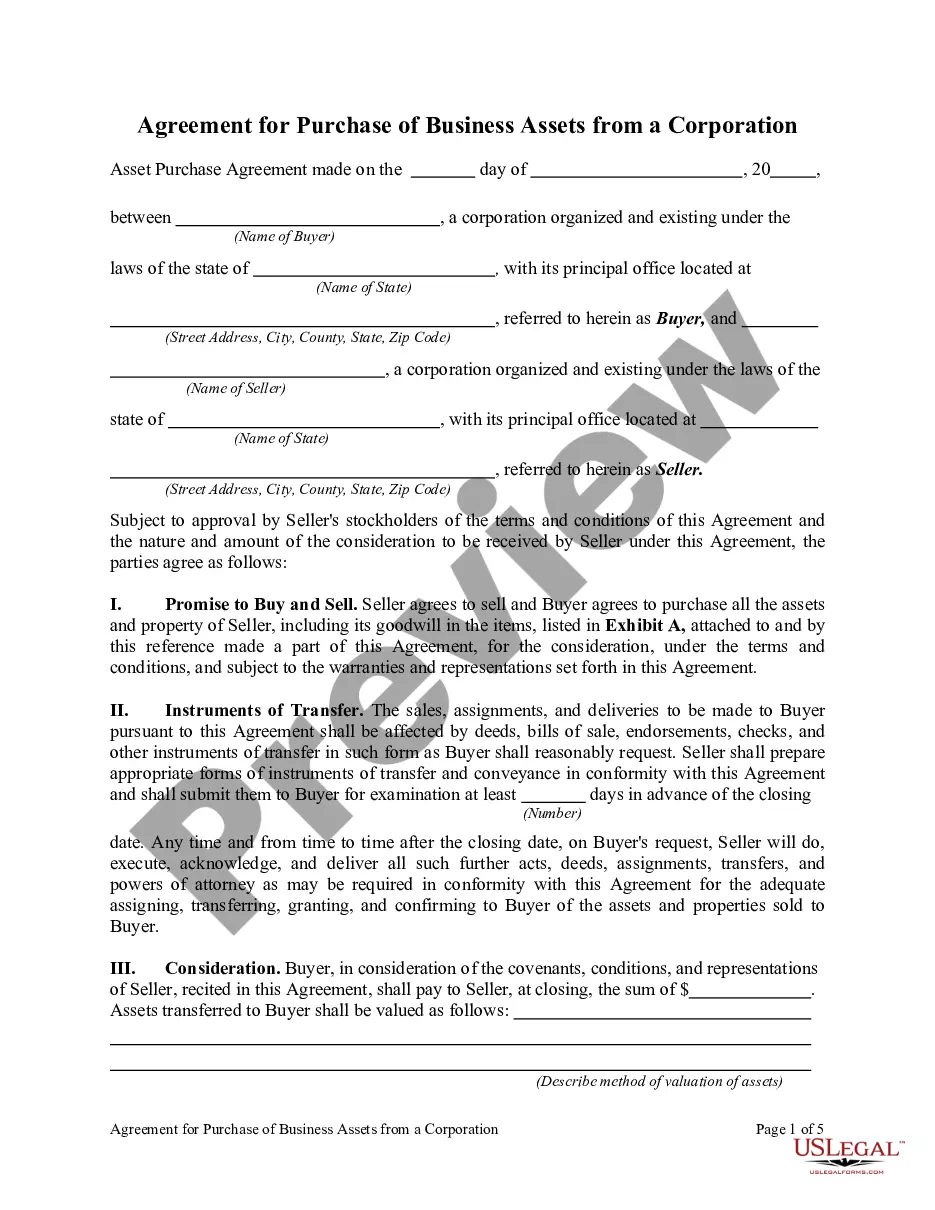

Maine Agreement for Purchase of Business Assets from a Corporation

Description

How to fill out Agreement For Purchase Of Business Assets From A Corporation?

US Legal Forms - one of the most extensive repositories of legal documents in the United States - provides a selection of legal form templates that you can download or print.

By utilizing the website, you can access thousands of forms for business and personal purposes, organized by categories, states, or keywords.

You can find the latest forms such as the Maine Agreement for Purchase of Business Assets from a Corporation in mere moments.

Click the Preview button to review the contents of the form. Check the form description to confirm that you have selected the correct form.

If the form does not meet your needs, use the Search field at the top of the screen to find one that does.

- If you have an account, Log In to download the Maine Agreement for Purchase of Business Assets from a Corporation from the US Legal Forms repository.

- The Download button will appear on every form you view.

- You can access all previously saved forms in the My documents section of your account.

- If you're using US Legal Forms for the first time, here are simple steps to help you get started.

- Ensure you have selected the correct form for your city/state.

Form popularity

FAQ

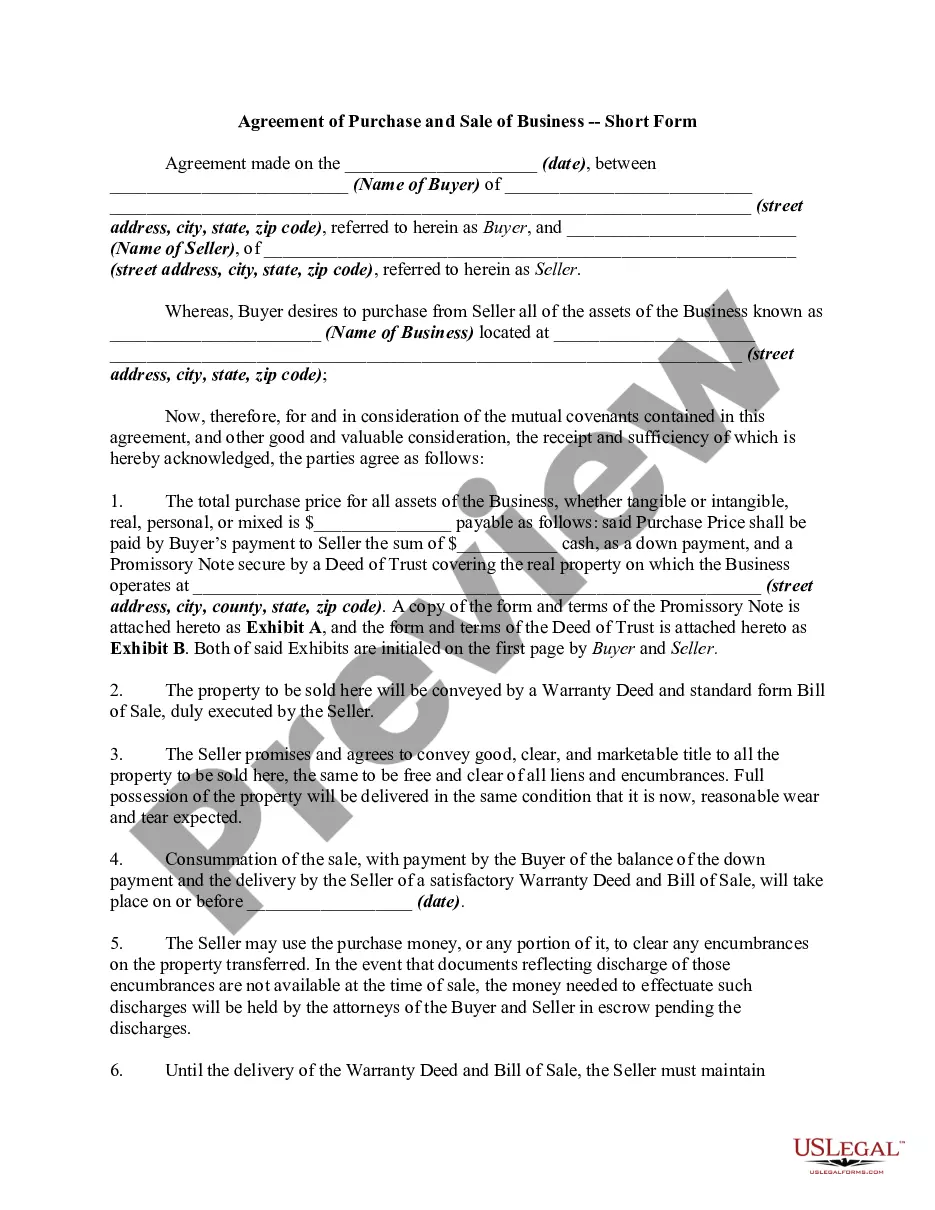

Provisions of an APA may include payment of purchase price, monthly installments, liens and encumbrances on the assets, condition precedent for the closing, etc. An APA differs from a stock purchase agreement (SPA) under which company shares, title to assets, and title to liabilities are also sold.

The bill of sale is typically delivered as an ancillary document in an asset purchase to transfer title to tangible personal property. It does not cover intangible property (such as intellectual property rights or contract rights) or real property.

Simply put, Recitals are used to explain those matters of fact which are necessary to make a proposed transaction intelligible. Recitals are like a quick start guide to an APA, acquisition contract, or merger agreement.

The asset purchase agreement is often drafted up towards the end of the negotiation stage, so that the parties can have a final record of their agreement. The document essentially operates as a contract, creating legally binding duties on each of the parties involved.

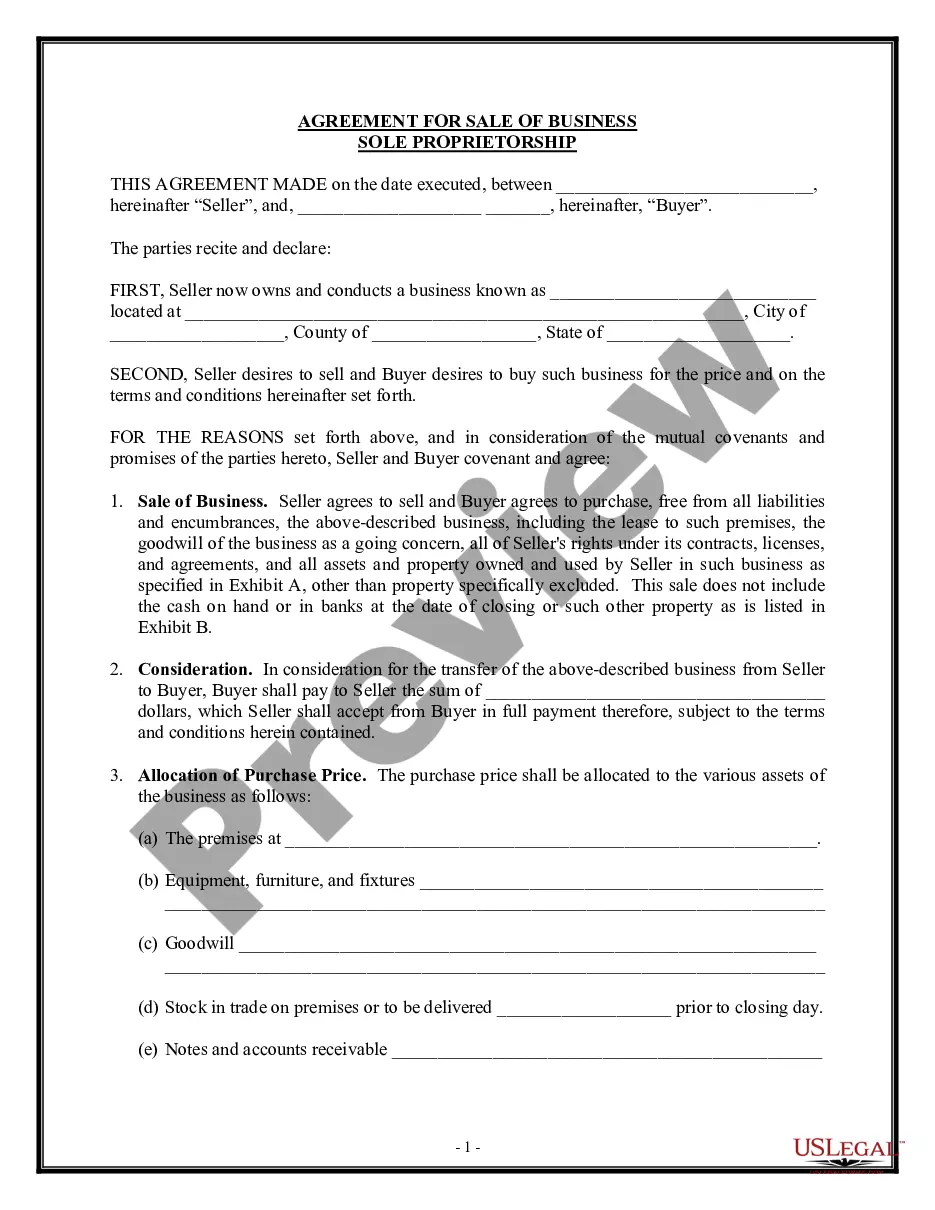

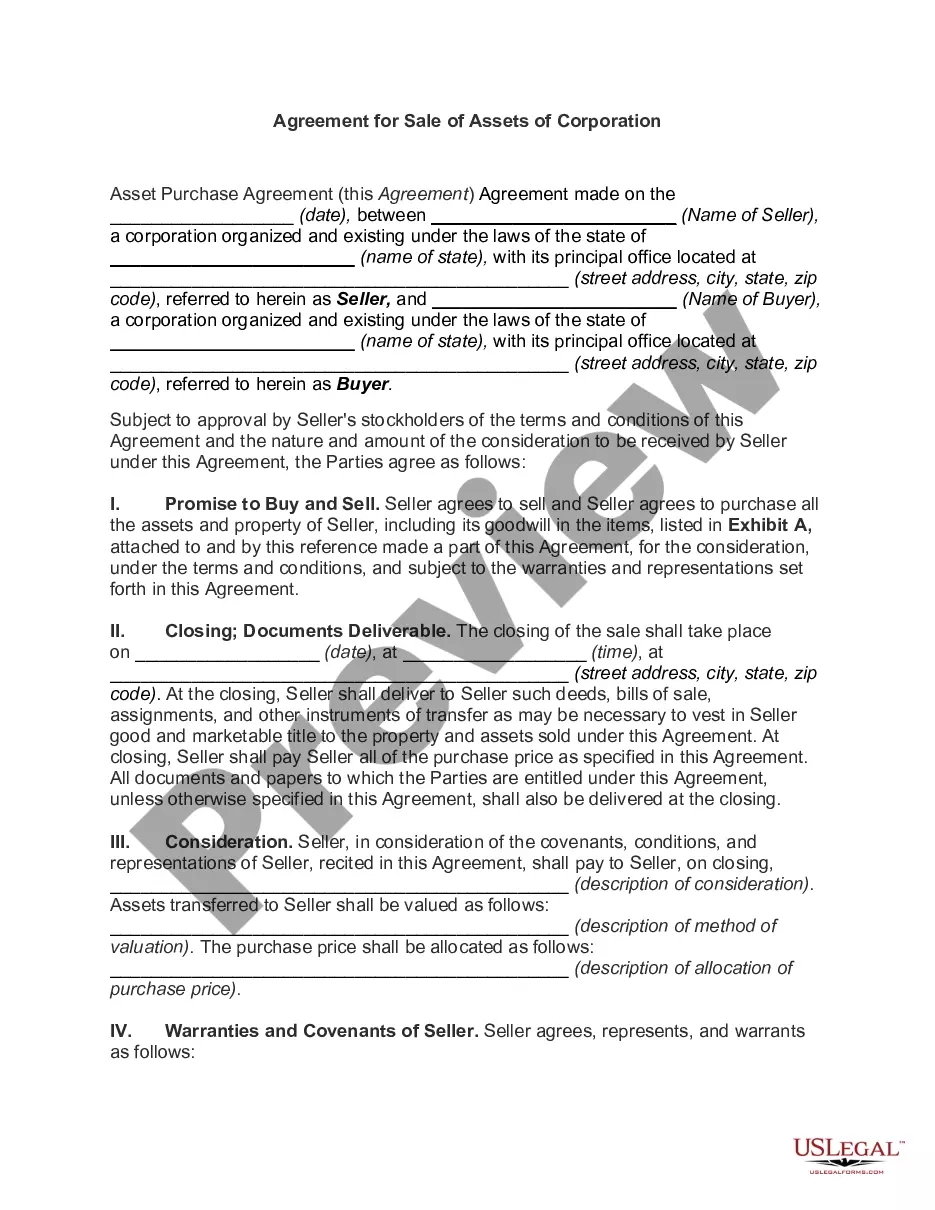

An asset purchase agreement is an agreement between a buyer and a seller to purchase property, like business assets or real property, either on their own or as part of a merger-acquisition.

In an asset purchase, the buyer will only buy certain assets of the seller's company. The seller will continue to own the assets that were not included in the purchase agreement with the buyer. The transfer of ownership of certain assets may need to be confirmed with filings, such as titles to transfer real estate.

Parts of an Asset Purchase AgreementRecitals. The opening paragraph of an asset purchase agreement includes the buyer and seller's name and address as well as the date of signing.Definitions.Purchase Price and Allocation.Closing Terms.Warranties.Covenants.Indemnification.Governance.More items...

The recitals give background information about the parties, about the context of the agreement and an introduction to the agreement itself. There are several kinds of whereas clauses: Party-related recitals: one or more whereas clauses can reflect the relevant business activities of each party.

An asset purchase involves the purchase of the selling company's assets -- including facilities, vehicles, equipment, and stock or inventory. A stock purchase involves the purchase of the selling company's stock only.

While buyer's counsel typically prepares the first draft of an asset purchase agreement, there may be circumstances (such as an auction) when seller's counsel prepares the first draft.