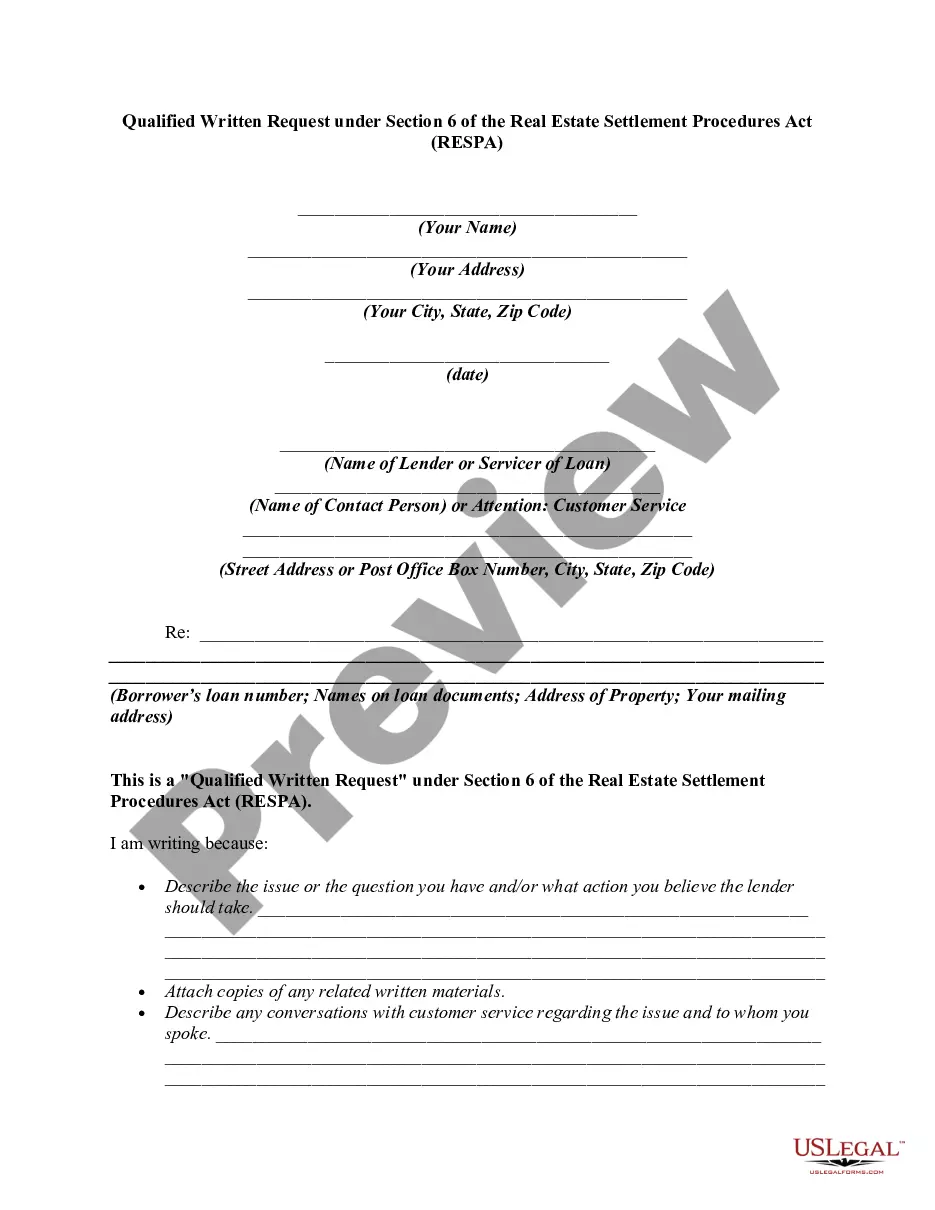

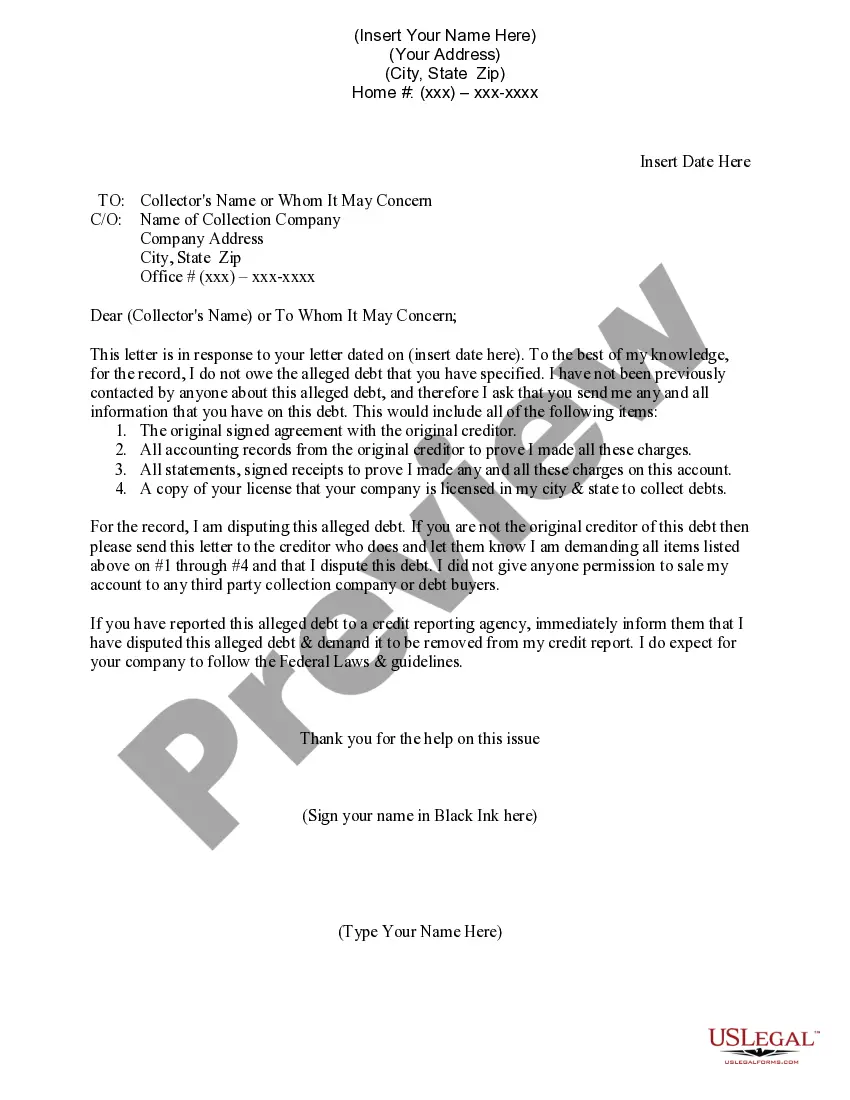

Maryland Qualified Written RESPA Request to Dispute or Validate Debt

Description

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Looking for another form?

How to fill out Qualified Written RESPA Request To Dispute Or Validate Debt?

Selecting the ideal legal document format can be a challenge.

Certainly, there are numerous templates accessible online, but how can you obtain the legal form you require.

Utilize the US Legal Forms website.

If you are a new customer of US Legal Forms, here are simple instructions for you to follow: First, make sure you have selected the correct form for your city/state. You can preview the form using the Preview button and review the form details to ensure it meets your needs.

- The service offers a vast selection of templates, such as the Maryland Qualified Written RESPA Request to Dispute or Validate Debt, that you can use for both business and personal purposes.

- All forms are reviewed by experts and comply with federal and state regulations.

- If you are currently registered, Log In to your account and click on the Download button to find the Maryland Qualified Written RESPA Request to Dispute or Validate Debt.

- Use your account to browse the legal forms you have previously purchased.

- Visit the My documents tab in your account to obtain another copy of the document you need.

Form popularity

FAQ

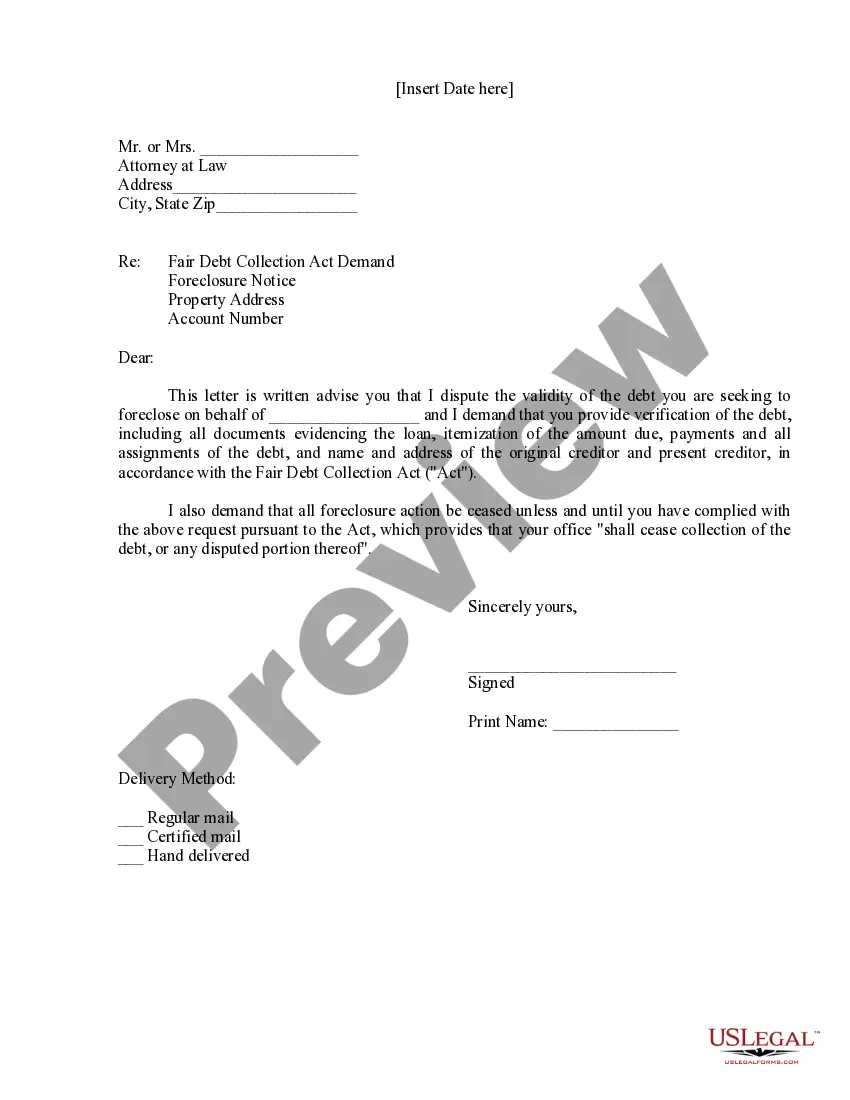

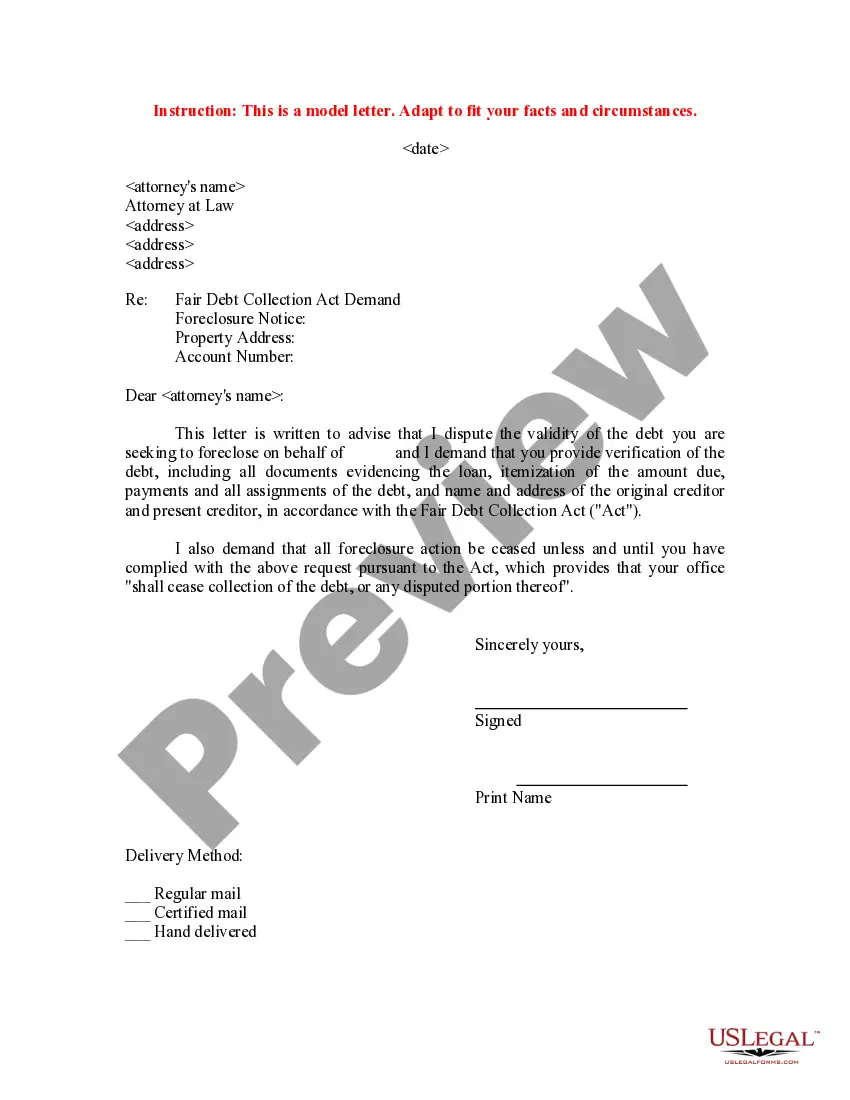

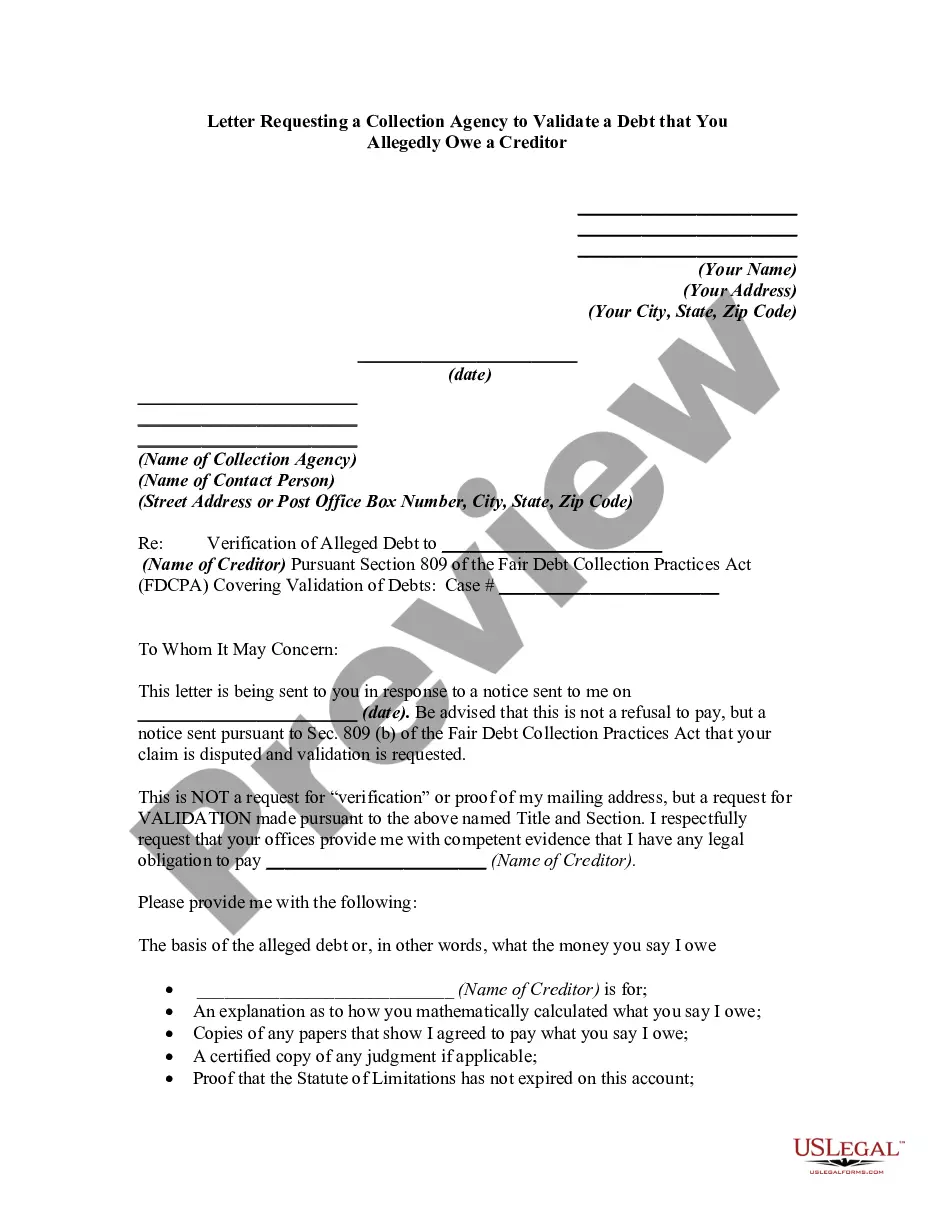

A Maryland validation of debt letter is a document that requests a creditor to provide evidence that a debt is valid and belongs to you. This letter is your right as a consumer to confirm the details surrounding the debt. It aids in preventing any errors or misunderstandings about your financial obligations. To facilitate this request, you may consider using US Legal Forms, which offers templates for a Maryland Qualified Written RESPA Request to Dispute or Validate Debt.

A debt validation letter in Maryland is a written request you send to a creditor to confirm that you owe the debt. It asks the creditor to provide verification of the debt's details and legitimacy. This process is important because it helps you ensure that the information in the debt is accurate. Using a Maryland Qualified Written RESPA Request to Dispute or Validate Debt can streamline this process, ensuring your rights are protected.

A lender must provide the required RESPA information to a buyer within 30 days of receiving a Maryland Qualified Written RESPA Request to Dispute or Validate Debt. This timeframe is crucial, as it ensures that borrowers receive the vital information they need to understand the status of their mortgage or debt. By complying with this regulation, lenders help foster transparency and trust. For those navigating these complexities, using US Legal Forms can streamline the process and ensure you submit accurate requests.

RESPA prohibits two significant practices that could harm consumers: kickbacks and unearned fees. Kickbacks refer to any payment made in exchange for referrals, which can inflate costs for borrowers. Additionally, RESPA ensures that consumers are not charged for services that were not provided. This protection is critical for anyone utilizing a Maryland Qualified Written RESPA Request to Dispute or Validate Debt.

In Maryland, a debt collector can legally pursue old debt for three years after the last payment or last acknowledgment of the debt. However, this time frame can vary based on the type of debt and individual circumstances. It’s important to understand your rights and consider using a Maryland Qualified Written RESPA Request to Dispute or Validate Debt if you believe the debt is no longer valid. Knowing these details can help you navigate your options effectively.

This statement must advise the borrower whether the lender intends to service the loan or transfer it to another lender. The statement must also contain information about the steps borrowers can take to resolve any complaints they may have.

Within five days (excluding legal public holidays, Saturdays, and Sundays) of a servicer receiving an information request from a borrower, the servicer shall provide to the borrower a written response acknowledging receipt of the information request.

Generally, a servicer acts promptly to provide the written notice required by § 1024.41(c)(2)(iii) if the servicer provides such written notice no later than five days (excluding legal public holidays, Saturdays, and Sundays) after offering the borrower a short-term payment forbearance program or short-term repayment

RESPA requires that borrowers receive disclosures at various times in the transaction process. Some disclosures spell out the costs associated with the settlement, outline lender servicing and escrow account practices and describe business relationships between settlement service providers.

The servicer must then, within 30 business days after receipt of the notice of error, conduct a reasonable investigation of the error(s) asserted by the borrower and either (1) correct the error(s) and send a written notice of correction to the borrower; or (b) send the borrower a written notice that no error occurred.