This form is an Assumption Agreement. The form provides that the grantee will assume a lien on property described in the agreement. The assumption will become effective on the date provided in the agreement.

Maryland Assumption Agreement of Loan Payments

Category:

State:

Multi-State

Control #:

US-00424

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Assumption Agreement Of Loan Payments?

If you wish to total, obtain, or print authorized document templates, use US Legal Forms, the most important collection of authorized forms, which can be found online. Use the site`s simple and practical research to find the files you want. A variety of templates for organization and specific functions are categorized by groups and claims, or key phrases. Use US Legal Forms to find the Maryland Assumption Agreement of Loan Payments within a couple of click throughs.

In case you are presently a US Legal Forms buyer, log in to your account and click on the Down load option to have the Maryland Assumption Agreement of Loan Payments. Also you can accessibility forms you previously delivered electronically within the My Forms tab of your account.

If you work with US Legal Forms initially, follow the instructions beneath:

- Step 1. Ensure you have chosen the shape to the proper area/country.

- Step 2. Make use of the Review solution to check out the form`s content. Never forget about to read the outline.

- Step 3. In case you are not happy using the kind, take advantage of the Look for industry on top of the display screen to get other types of the authorized kind design.

- Step 4. Once you have discovered the shape you want, click on the Buy now option. Choose the pricing program you favor and put your qualifications to register for the account.

- Step 5. Process the deal. You can utilize your bank card or PayPal account to finish the deal.

- Step 6. Select the format of the authorized kind and obtain it in your gadget.

- Step 7. Total, edit and print or sign the Maryland Assumption Agreement of Loan Payments.

Every authorized document design you get is your own permanently. You may have acces to each and every kind you delivered electronically in your acccount. Click the My Forms portion and choose a kind to print or obtain once again.

Remain competitive and obtain, and print the Maryland Assumption Agreement of Loan Payments with US Legal Forms. There are millions of professional and state-specific forms you can utilize for your organization or specific requires.

Form popularity

FAQ

In real estate transactions, an assumption agreement allows a third party to ?assume? or take over the loan of the property's seller. Mortgages may be assumed when the house is sold, a divorcing spouse is awarded the property in a settlement or when someone inherits property.

"Assume" means the buyer takes on liability, and the seller is no longer primarily liable. "Subject to" means the seller is not released from responsibility. The word "assumption" is used when a buyer assumes personal liability for an existing debt.

An assumable mortgage is a home loan that can be transferred from the original borrower to the next homeowner. The interest rate and payment period stay the same. For example, if a 30-year mortgage is three years old, the person assuming the loan has 27 years to pay it off.

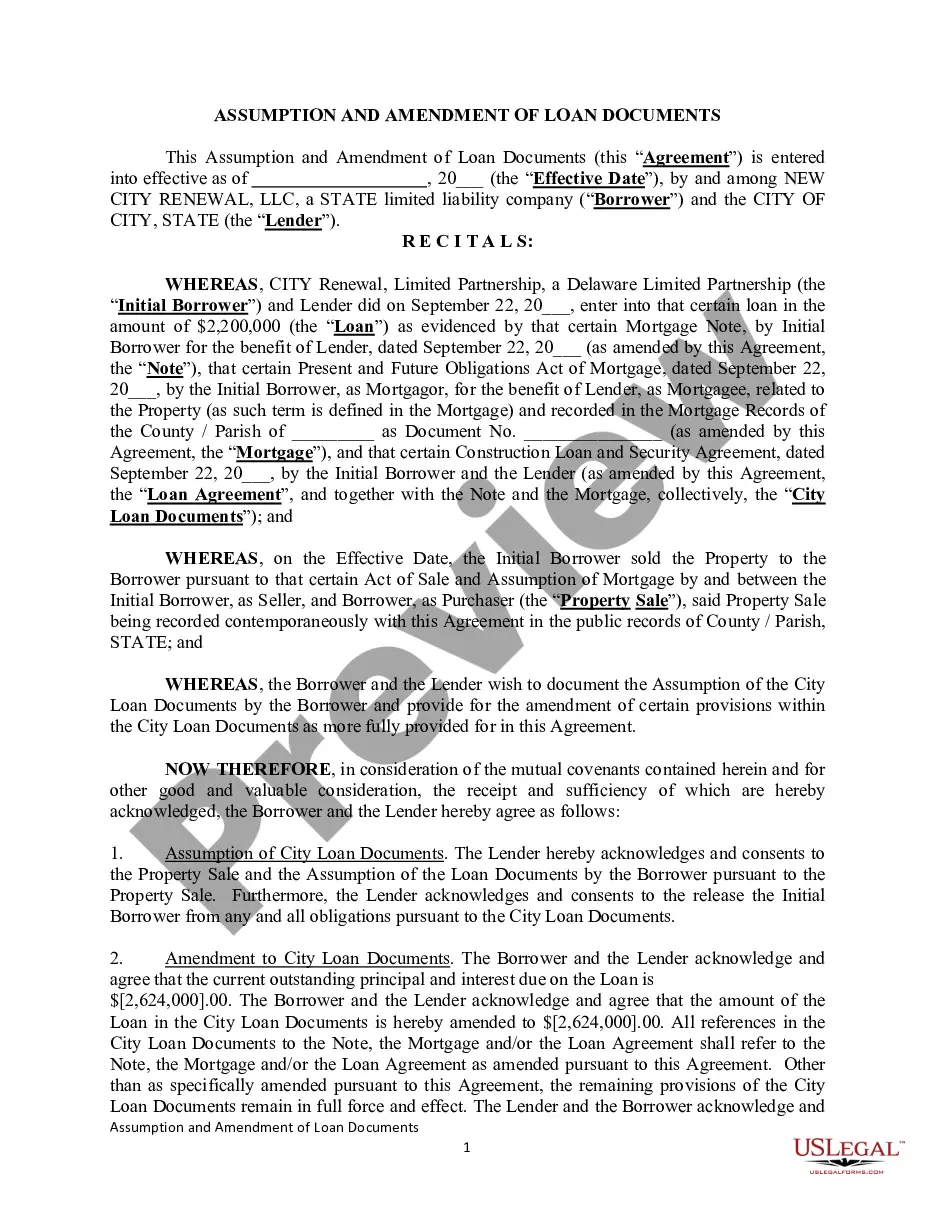

Assumption of Obligations. New Borrower covenants, promises, and agrees that New Borrower, jointly and severally if more than one, will unconditionally assume and be bound by all terms, provisions, and covenants of the Assumed Loan Documents as if New Borrower had been the original maker of the Assumed Loan Documents.

Updated March 7, 2022. In real estate transactions, an assumption agreement allows a third party to ?assume? or take over the loan of the property's seller. Mortgages may be assumed when the house is sold, a divorcing spouse is awarded the property in a settlement or when someone inherits property.

Assumable refers to when one party takes over the obligation of another. In terms of an assumable mortgage, the buyer assumes the existing mortgage of the seller. When the mortgage is assumed, the seller is often no longer responsible for the debt.

How long does the assumption process take? Assumption TypeProcessing TimeStandard Assumption60 ? 90 DaysAssumption Due to Divorce60 ? 90 DaysAssumption After Death30 ? 60 Days

A loan assumption agreement is an agreement between a lender, original borrower, and a new borrower, where the new borrower agrees to assume responsibility for the debt owed by original borrower.