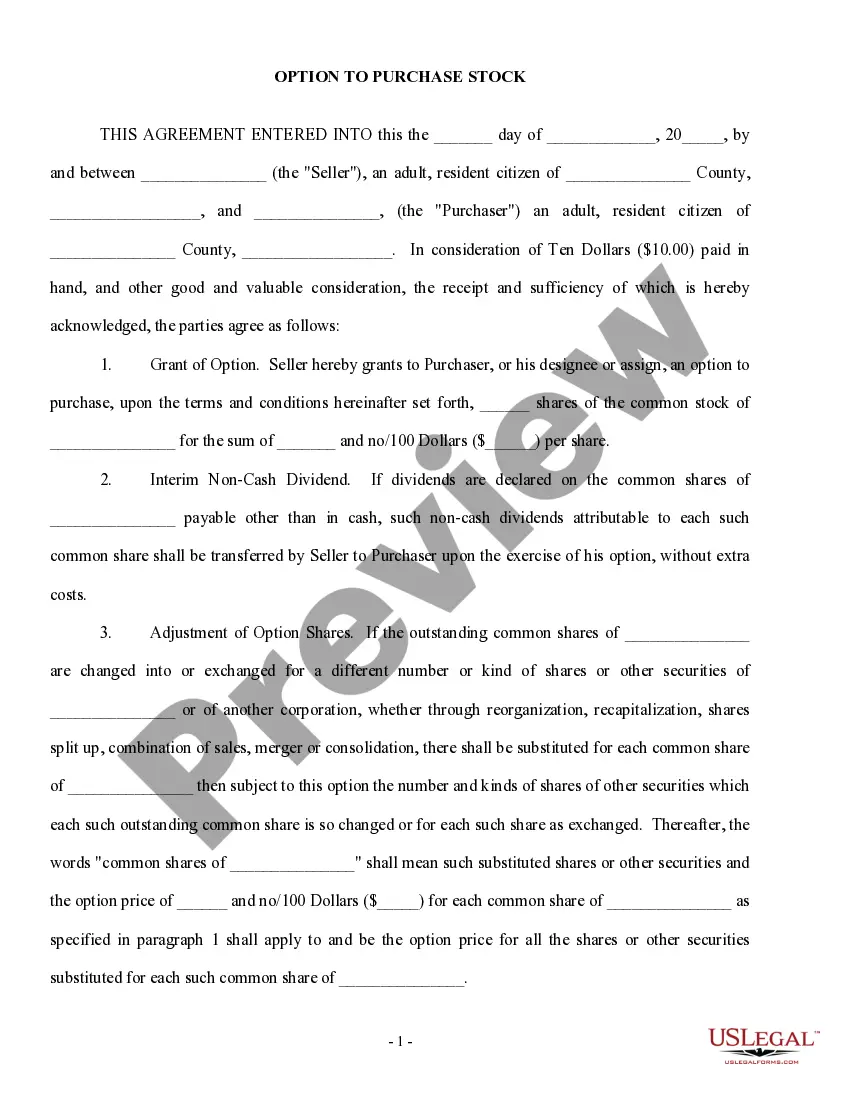

Massachusetts Option to Purchase Stock - Short Form

Description

How to fill out Option To Purchase Stock - Short Form?

You can devote several hours online looking for the legal document template that fulfills the state and federal requirements you seek.

US Legal Forms offers thousands of legal templates that are reviewed by professionals.

You may obtain or create the Massachusetts Option to Purchase Stock - Short Form from the service.

In order to find another version of the form, utilize the Search field to locate the template that suits your needs and criteria.

- If you already have a US Legal Forms account, you can Log In and click on the Download option.

- Then, you can complete, modify, print, or sign the Massachusetts Option to Purchase Stock - Short Form.

- Each legal document template you purchase is yours indefinitely.

- To get another copy of a purchased form, visit the My documents tab and select the relevant option.

- If you are using the US Legal Forms site for the first time, follow the simple directions below.

- First, ensure that you have selected the correct document template for the state/city of your selection.

- Read the form description to confirm that you have chosen the right document.

Form popularity

FAQ

Tiered partnership arrangements are ownership structures where one pass-through entity, a lower-tier entity, is owned by one or more other taxable entities, an upper-tier entity, allowing limited liability, asset protection, and tax advantages for owners.

Stock options don't last forever. Typically, there's a vesting schedule that lasts anywhere from one to four years, though some employees may have up to 10 years. And if you leave the company for whatever reason, whether it's because of a layoff, resignation, or retirement, you may only have 90 days to use them.

The excess of the fair market value of the stock at the date the option was exercised over the amount paid for the stock is taxed as compensation at the time the stock is sold. Any additional profit is taxed as capital gain.

Massachusetts Securities Corporation means any Domestic Subsidiary that is classified as a security corporation by the Massachusetts Department of Revenue pursuant to Massachusetts General Law c. 63, § 38B, or any successor statute.

Background. Under the employee stock option rules in the Income Tax Act, employees who exercise stock options must pay tax on the difference between the value of the stock and the exercise price paid. Provided certain conditions are met, an employee can claim an offsetting deduction equal to 50% of the taxable benefit.

An employee is not taxed when he is granted or exercises an ISO. When the stock received on the exercise of the option and held for the required period, one year, is sold the employee realizes capital gain income.

If you've held the stock or option for less than one year, your sale will result in a short-term gain or loss, which will either add to or reduce your ordinary income. Options sold after a one year or longer holding period are considered long-term capital gains or losses.

Short-term trades with options By short we mean not just a few hours, like intraday trading, but a few days. The well-known advantage of the decline in the time value is not the focus of this trade, but the change in the implied volatility and the movement of the underlying in the desired direction.

Stock options, both vested and unvested, are considered assets in a divorce that can be divided between the spouses. The most common way to divide stock options is for the divorcing employee to retain the stock options and award the nonemployee spouse other marital assets of equivalent value as an offset.

When you exercise an option, you purchase shares of the company's stock directly from the company. The grant price (also commonly referred to as the exercise price) is the amount you pay to the company for each share. This price is set by the company at the time the stock option grant is made (grant date).