Louisiana Notice of Adverse Action - Non-Employment - Due to Credit Report

Description

How to fill out Notice Of Adverse Action - Non-Employment - Due To Credit Report?

Selecting the optimal legal document template can be a challenge. Obviously, numerous templates exist online, but how can you locate the legal form you require.

Use the US Legal Forms website. The service provides a plethora of templates, including the Louisiana Notice of Adverse Action - Non-Employment - Due to Credit Report, suitable for both business and personal purposes.

All of the forms are reviewed by experts and comply with federal and state regulations.

Once you are convinced that the form is suitable, click the Get Now button to obtain the form. Select the pricing plan you wish and enter the required information. Create your account and pay for your purchase using your PayPal account or Visa or Mastercard. Specify the file format and download the legal document template to your device. Complete, edit, and print, then sign the obtained Louisiana Notice of Adverse Action - Non-Employment - Due to Credit Report. US Legal Forms is the largest collection of legal forms where you can find various document templates. Use the service to download professionally created documents that comply with state requirements.

- If you are already registered, Log In to your account and click the Download button to obtain the Louisiana Notice of Adverse Action - Non-Employment - Due to Credit Report.

- Use your account to browse the legal forms you have previously purchased.

- Visit the My documents tab on your account and download another copy of the document you need.

- If you are a new user of US Legal Forms, here are some simple steps to follow.

- First, ensure you have selected the correct form for your city/region. You can preview the form using the Review button and read through the form information to confirm it is the right one for you.

- If the form does not meet your specifications, use the Search field to find the correct one.

Form popularity

FAQ

RS .9 addresses specific criminal offenses within Louisiana, particularly concerning the unlawful use of personal identifying information. Understanding this statute is particularly important for anyone dealing with issues related to credit reports or identity theft. If you receive a Louisiana Notice of Adverse Action - Non-Employment - Due to Credit Report due to identity misuse, this statute could be relevant to your legal concerns. Being aware of your rights under this law helps you respond appropriately to such challenges.

RS .1 pertains to specific legal provisions in Louisiana's Revised Statutes. This statute deals with laws relating to the unauthorized use of vehicles, emphasizing the importance of protecting personal property. If you encounter legal issues or need clarification on how this statute may relate to credit reports or your rights, the Louisiana Notice of Adverse Action - Non-Employment - Due to Credit Report can guide you. Understanding these laws helps you respond appropriately to legal concerns.

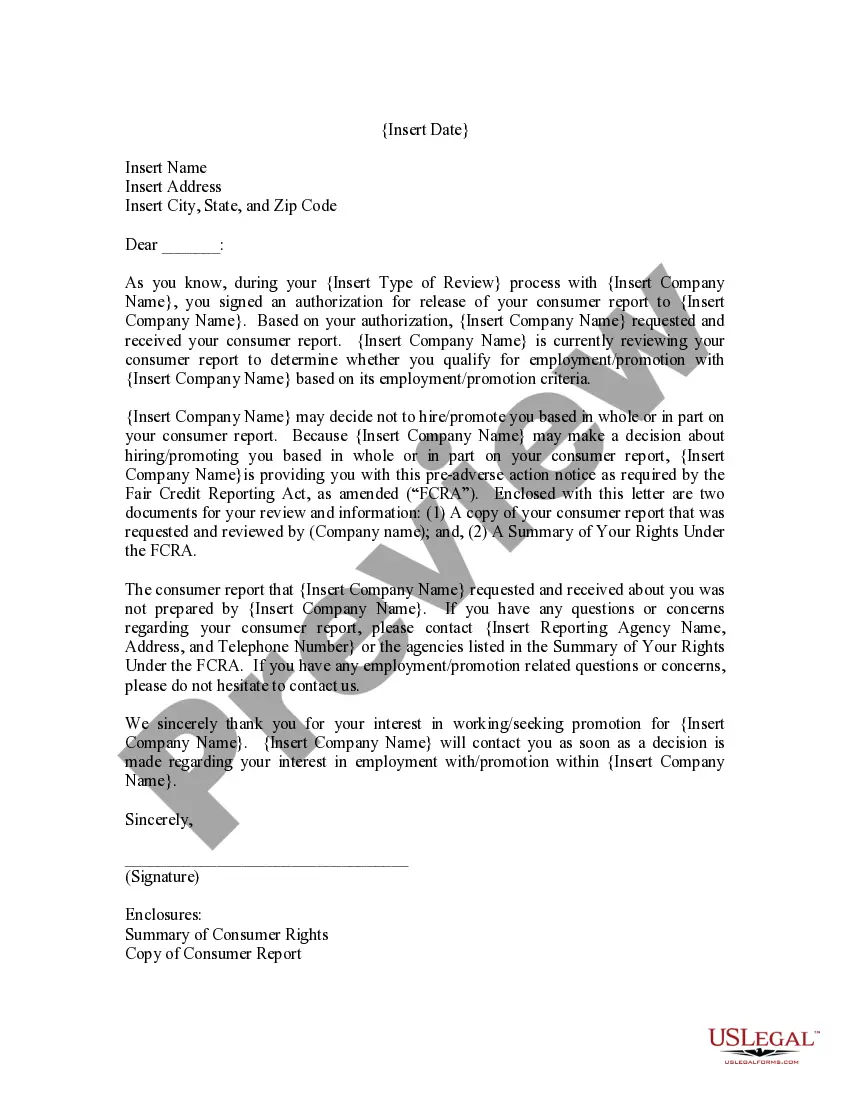

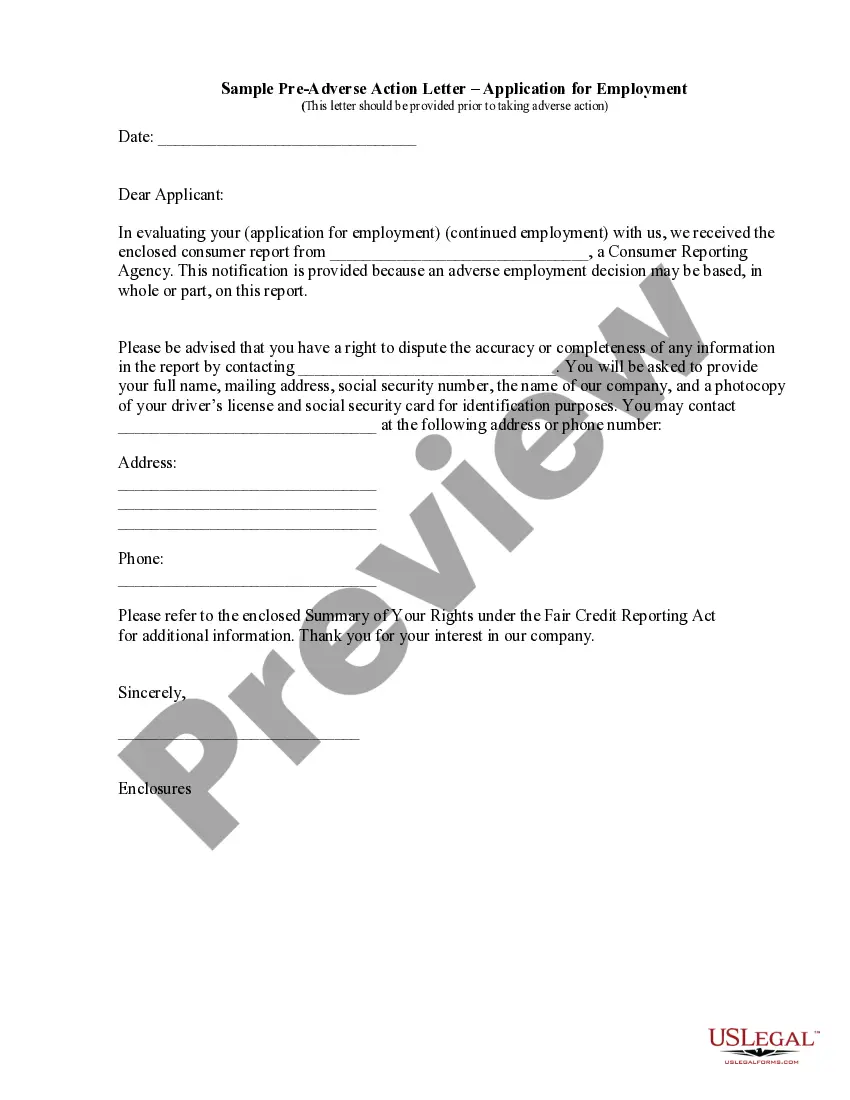

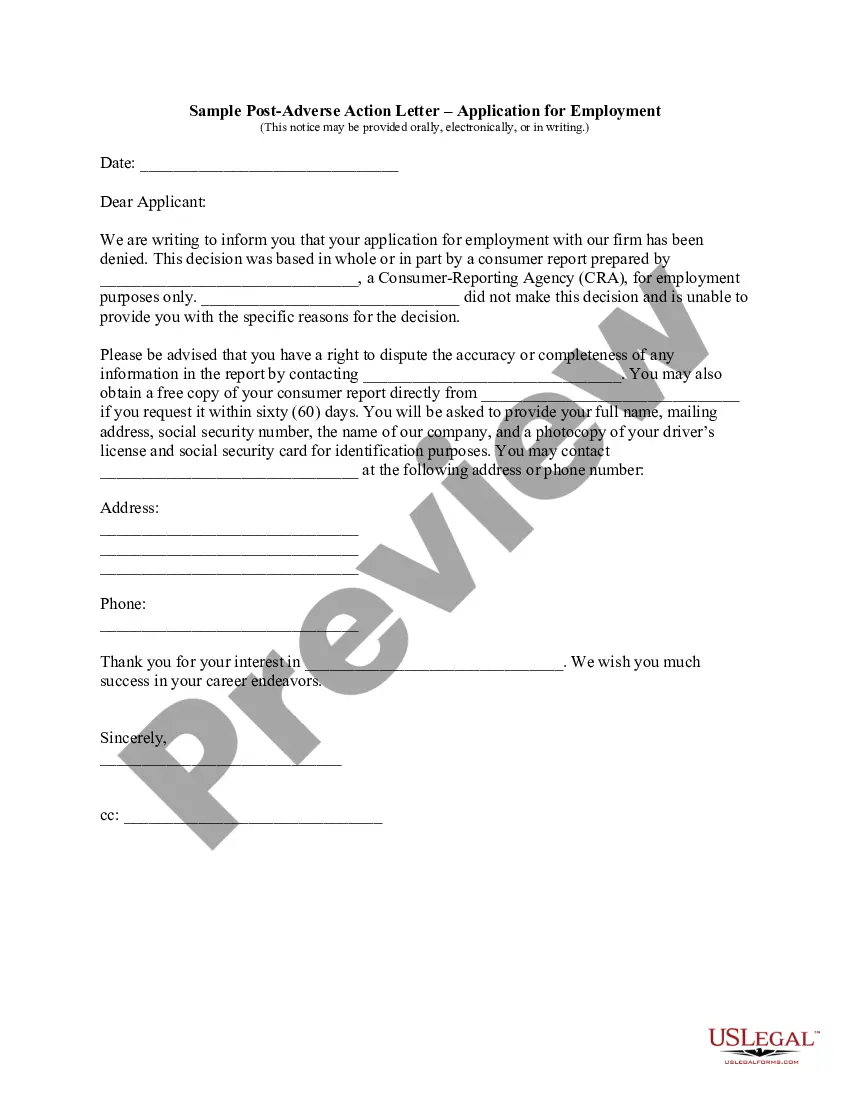

If you plan to take adverse action based on consumer report finding, you must send the tenant or employee a Pre-Adverse Action notice within 3 days of receiving the consumer report. Though this notice is typically mailed, it may also be communicated verbally or by e-mail.

Question: What is the processing time for a background request? If there is no record you should receive a response within 24 hrs. If fingerprints are requested the response will have to be handled manually and may take approximately 15-21 business days.

In the case of multiple applicants under the FCRA, the statute has been interpreted to require notice to all consumers against whom adverse action is taken if the action taken was based on information in a consumer report.

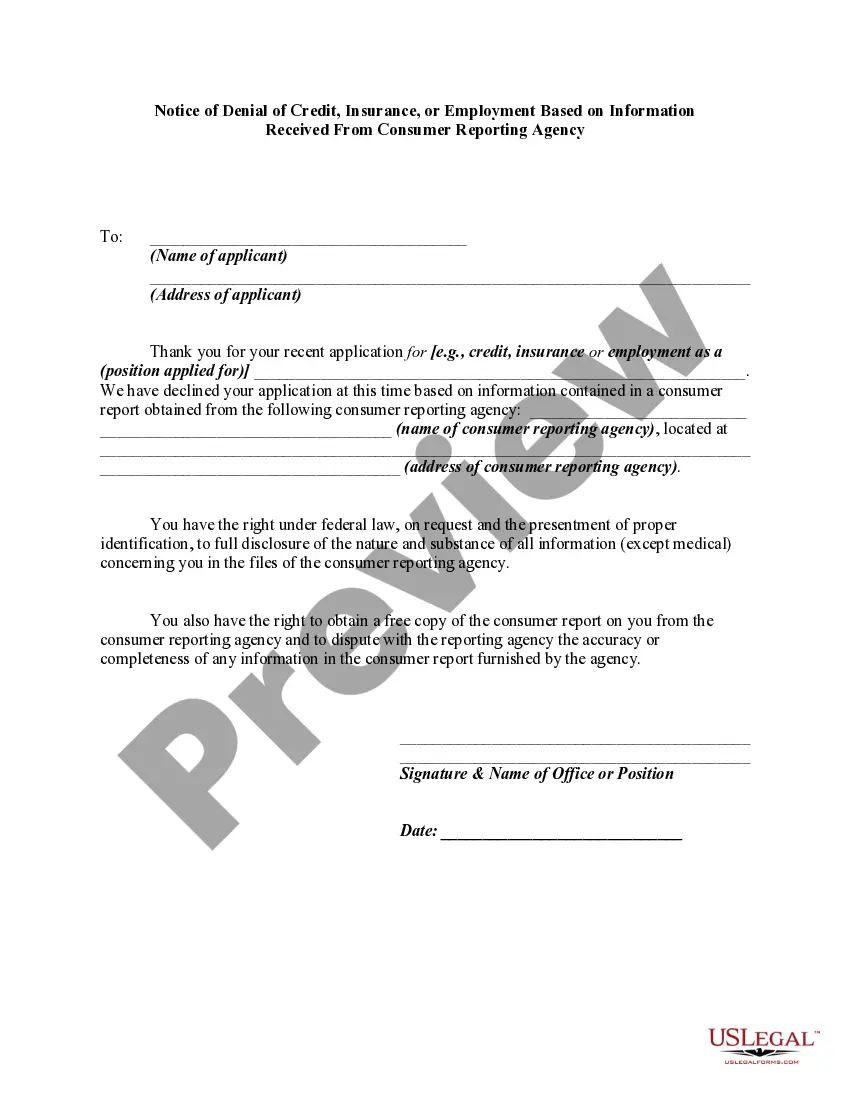

Updated April 29, 2022. An adverse action notice is sent to an individual when rejected based on information in a credit report or background check (consumer report). It is required when a person is denied employment, housing, credit, or insurance. Federal Laws Fair Credit Reporting Act (FCRA)

Louisiana's Fair Chance law builds off related Ban the Box laws, which prohibit employers from inquiring about criminal history or arrest records and from conducting a background check prior to an interview. Louisiana adopted a Ban the Box law in 2016, which applies to state and political subdivision employers.

In general, background checks typically cover seven years of criminal and court records, but can go back further depending on compliance laws and what is being searched.

If you deny a consumer credit based on information in a consumer report, you must provide an adverse action notice to the consumer. if you grant credit, but on less favorable terms based on information in a consumer report, you must provide a risk-based pricing notice.

It must include information about the credit bureau used, an explanation of the specific reasons for the adverse action, a notice of the consumer's right to a free credit report and to dispute its accuracy and the consumer's credit score.