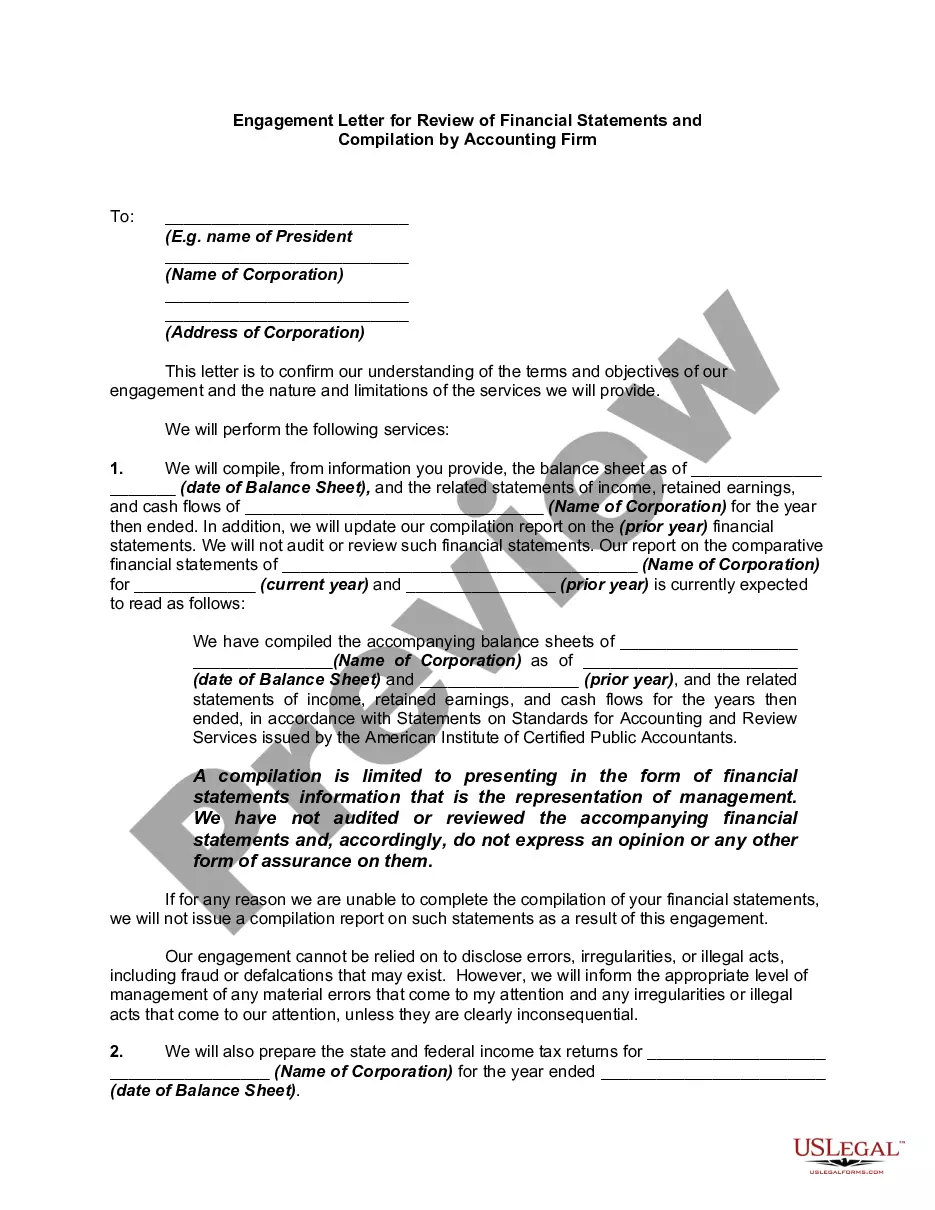

In a compilation engagement, the accountant presents in the form of financial statements information that is the representation of management (owners) without undertaking to express any assurance on the statements. In other words, using management's records, the accountant creates financial statements without gathering evidence or opining about the validity of those underlying records. Because compiled financial statements provide the reader no assurance regarding the statements, they represent the lowest level of financial statement service accountants can provide to their clients. Accordingly, standards governing compilation engagements require that financial statements presented by the accountant to the client or third parties must at least be compiled.

Louisiana Report from Review of Financial Statements and Compilation by Accounting Firm

Description

How to fill out Report From Review Of Financial Statements And Compilation By Accounting Firm?

If you need to finalize, retrieve, or print valid document templates, utilize US Legal Forms, the top choice for legal forms available online.

Employ the site’s user-friendly search feature to find the documents you require.

A diverse range of templates for business and personal purposes are sorted by categories and states, or keywords. Use US Legal Forms to access the Louisiana Report from Review of Financial Statements and Compilation by Accounting Firm in just a few clicks.

Every legal document template you purchase is yours indefinitely. You have access to every form you downloaded in your account. Go to the My documents section and select a form to print or download again.

Be proactive and download and print the Louisiana Report from Review of Financial Statements and Compilation by Accounting Firm with US Legal Forms. There are millions of professional and state-specific forms available for your business or personal needs.

- If you are already a US Legal Forms member, sign in to your account and click the Download button to obtain the Louisiana Report from Review of Financial Statements and Compilation by Accounting Firm.

- You can also find forms you previously downloaded in the My documents tab of your account.

- If you are using US Legal Forms for the first time, follow the steps below.

- Step 1. Ensure you have chosen the correct form for your specific city/state.

- Step 2. Utilize the Preview option to review the form’s details. Remember to read the description.

- Step 3. If you are not satisfied with the form, use the Search field at the top of the screen to find other versions of the legal form template.

- Step 4. Once you have found the form you desire, click on the Get now button. Select your preferred pricing plan and enter your information to register for an account.

- Step 5. Process the transaction. You can use your credit card or PayPal account to complete the transaction.

- Step 6. Choose the format of the legal form and download it to your device.

- Step 7. Fill out, edit, and print or sign the Louisiana Report from Review of Financial Statements and Compilation by Accounting Firm.

Form popularity

FAQ

Audited financial statements are verified by an independent accountant to ensure their accuracy and adherence to accounting standards. In contrast, financial statements refer to reports that reflect a company’s financial position but may not undergo any external verification. The Louisiana Report from Review of Financial Statements and Compilation by Accounting Firm provides compilation services that offer a substantial overview without full audits. By using uslegalforms, you can easily obtain the necessary documentation and guidance for your financial reporting needs.

The difference primarily involves the depth of evaluation and assurance level. A compilation involves an accountant compiling data with no assurance, while a review requires analytical procedures that provide limited assurance. Understanding these differences is essential, especially for businesses in Louisiana, where a Louisiana Report from Review of Financial Statements and Compilation by Accounting Firm can guide the selection of the most suitable financial service.

A review is an assessment performed by a CPA firm that includes analytical procedures on financial statements. This process allows the firm to express limited assurance about the reliability of the statements without undertaking a full audit. Companies in Louisiana benefit from having a clear Louisiana Report from Review of Financial Statements and Compilation by Accounting Firm, which helps in presenting their financial status transparently.

The key difference lies in the level of assurance provided. Compiled financial statements summarize information without verification, while reviewed financial statements involve some analytical procedures to validate the data. This distinction is critical for businesses in Louisiana, as it influences stakeholders' perceptions, which can be clarified through a Louisiana Report from Review of Financial Statements and Compilation by Accounting Firm.

Certified Public Accountants (CPAs) are typically responsible for reviewing financial statements. They utilize their expertise to conduct a review that includes various analytical procedures designed to assess the financial health of an organization. Clients often seek a CPA from an accredited firm for a Louisiana Report from Review of Financial Statements and Compilation by Accounting Firm to ensure professional standards are met.

Audited financial statements undergo a comprehensive examination, while reviewed financial statements are evaluated with less rigor. Audits provide a high level of assurance due to extensive verification of data, whereas reviews involve limited assurance through analytical procedures. For businesses in Louisiana, the chosen approach can impact their financial credibility, especially when reviewing the Louisiana Report from Review of Financial Statements and Compilation by Accounting Firm.

No, a compilation is not the same as a review. While both services involve an accounting firm's assessment of financial statements, a compilation is generally less detailed than a review. In a compilation, the accountant summarizes the financial data without providing any assurance about the accuracy, whereas a review involves additional analytical procedures and provides some level of assurance. Therefore, to understand the implications, consider obtaining a Louisiana Report from Review of Financial Statements and Compilation by Accounting Firm.

Yes, a CPA is required to be independent when conducting a review of financial statements. This independence is essential to maintain objectivity and credibility in the process. By ensuring independence, the CPA enhances the reliability of the Louisiana Report from Review of Financial Statements and Compilation by Accounting Firm, fostering trust among stakeholders.

A CPA performs a review of an entity's financial statements to provide limited assurance that no material modifications are needed for the statements to be in accordance with applicable financial reporting frameworks. The CPA engages in specific inquiry and analytical procedures, helping stakeholders make informed decisions. To ensure quality and compliance, consider obtaining a Louisiana Report from Review of Financial Statements and Compilation by Accounting Firm.

When performing a review of financial statements, the CPA is required to obtain a fundamental understanding of the organization’s internal controls and financial reporting framework. This understanding guides the CPA in conducting inquiries and analytical procedures designed to identify potential issues. Ultimately, the CPA will provide a Louisiana Report from Review of Financial Statements and Compilation by Accounting Firm that can serve as a valuable tool for decision-makers.