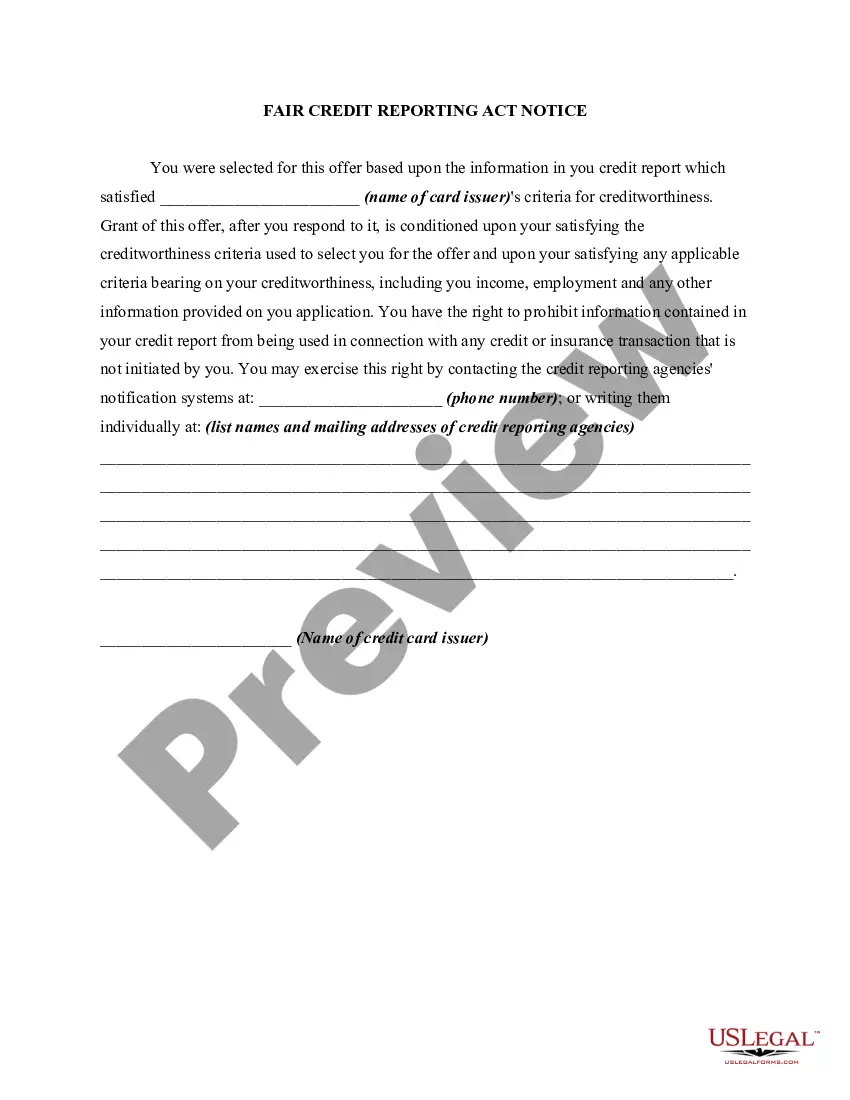

Whenever credit for personal, family, or household purposes involving a consumer is denied or the charge for the credit is increased either wholly or partly because of information obtained from a person other than a credit reporting agency bearing on the consumer's creditworthiness, credit standing, credit capacity, character, general reputation, personal characteristics, or mode of living, certain requirements must be met. The user of such information, when the adverse action is communicated to the consumer, must clearly and accurately disclose the consumer's right to make a written request for disclosure of the information. If such a request is made and is received within 60 days after the consumer learned of the adverse action, the user, within a reasonable period of time, must disclose to the consumer the nature of the information.

Louisiana Notice of Increase in Charge for Credit Based on Information Received From Person Other Than Consumer Reporting Agency

Description

How to fill out Notice Of Increase In Charge For Credit Based On Information Received From Person Other Than Consumer Reporting Agency?

Choosing the right legitimate document web template might be a struggle. Of course, there are a variety of layouts available on the Internet, but how would you get the legitimate form you require? Make use of the US Legal Forms site. The services delivers a huge number of layouts, including the Louisiana Notice of Increase in Charge for Credit Based on Information Received From Person Other Than Consumer Reporting Agency, that you can use for company and personal requirements. Every one of the varieties are examined by experts and fulfill state and federal demands.

When you are currently listed, log in to your accounts and click on the Obtain switch to find the Louisiana Notice of Increase in Charge for Credit Based on Information Received From Person Other Than Consumer Reporting Agency. Use your accounts to appear through the legitimate varieties you have purchased previously. Proceed to the My Forms tab of your accounts and obtain one more copy from the document you require.

When you are a whole new end user of US Legal Forms, listed here are basic instructions for you to comply with:

- Initially, make certain you have chosen the appropriate form for your metropolis/state. You can examine the shape making use of the Preview switch and browse the shape outline to make certain this is basically the best for you.

- In the event the form does not fulfill your requirements, take advantage of the Seach field to get the correct form.

- Once you are certain that the shape is suitable, go through the Acquire now switch to find the form.

- Pick the pricing strategy you would like and enter the needed info. Build your accounts and pay money for an order using your PayPal accounts or Visa or Mastercard.

- Choose the submit formatting and down load the legitimate document web template to your gadget.

- Full, revise and print out and indicator the attained Louisiana Notice of Increase in Charge for Credit Based on Information Received From Person Other Than Consumer Reporting Agency.

US Legal Forms will be the biggest local library of legitimate varieties in which you can find a variety of document layouts. Make use of the company to down load expertly-produced files that comply with state demands.

Form popularity

FAQ

Some examples of violations include: failing to report that a debt was discharged in bankruptcy. reporting old debts as new or re-aged.

A consumer reporting agency is any person that (1) for monetary fees, dues, or on a cooperative nonprofit basis regularly engages in whole or in part in the practice of assembling or evaluating consumer credit information, or other information on consumers, for the purpose of furnishing consumer reports to third ...

The Truth in Lending Act, or TILA, also known as regulation Z, requires lenders to disclose information about all charges and fees associated with a loan. This 1968 federal law was created to promote honesty and clarity by requiring lenders to disclose terms and costs of consumer credit.

The Fair Credit Reporting Act (FCRA) If compliance with the FCRA is not met, employers may face significant fines and penalties. In addition to fines, employers can also be sued by job applicants or employees who were subject to non-compliant background checks.

The Act (Title VI of the Consumer Credit Protection Act) protects information collected by consumer reporting agencies such as credit bureaus, medical information companies and tenant screening services. Information in a consumer report cannot be provided to anyone who does not have a purpose specified in the Act.

Any consumer who is denied credit, insurance, or employment on the whole or partial basis of information provided by a credit reporting agency shall be entitled to a copy of his credit report without charge, provided that he requests such report in writing from the agency within sixty days of being denied credit by a ...

Violations of the FCRA can carry fines, including damages if any are incurred. Enforcement of the FCRA falls to the Federal Trade Commission (FTC) and the Consumer Financial Protection Bureau (CFPB).

The Fair Credit Reporting Act (FCRA) , 15 U.S.C. § 1681 et seq., governs access to consumer credit report records and promotes accuracy, fairness, and the privacy of personal information assembled by Credit Reporting Agencies (CRAs).