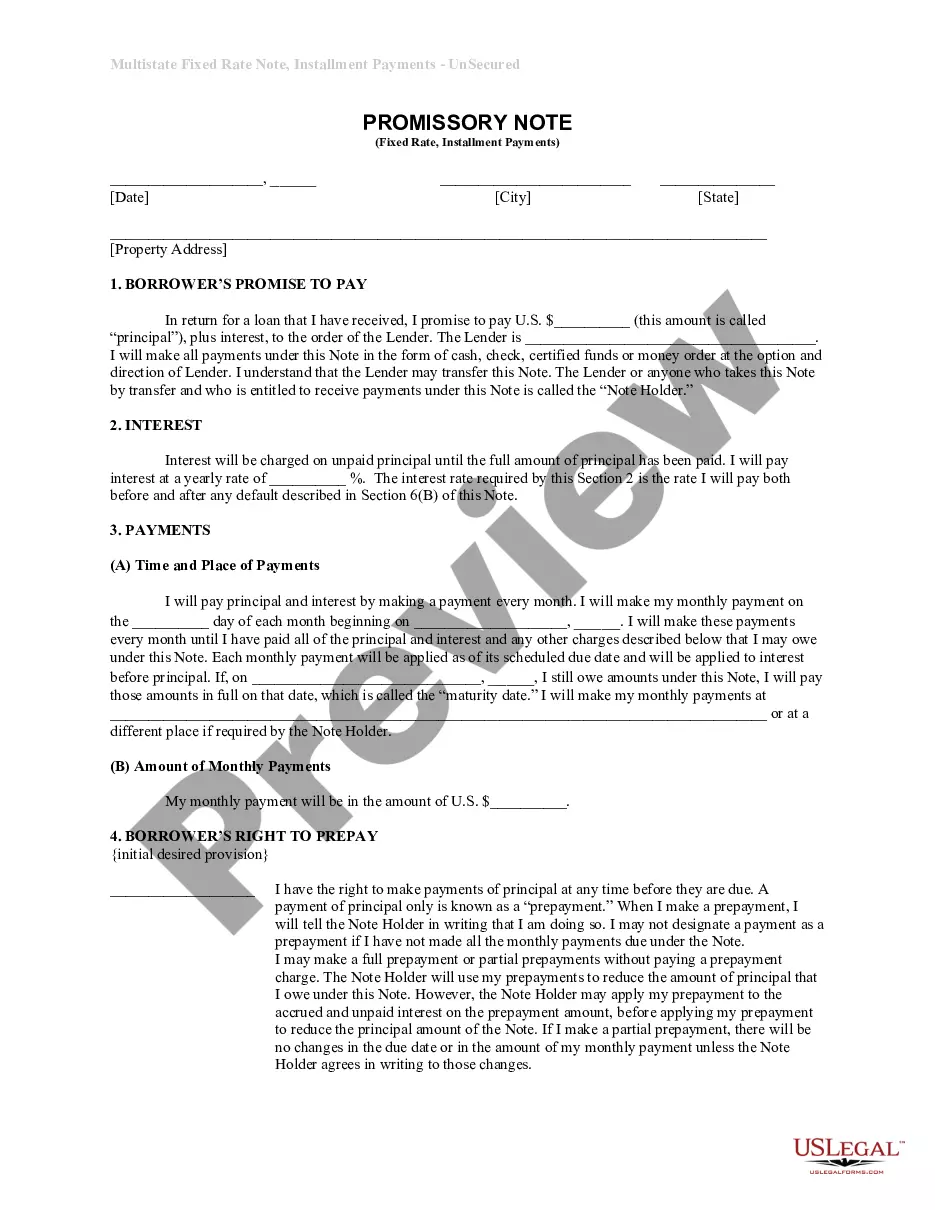

Louisiana Installments Fixed Rate Promissory Note Secured by Personal Property

About this form

The Louisiana Installments Fixed Rate Promissory Note Secured by Personal Property is a legal document that outlines a borrower's promise to repay a loan with fixed installment payments. It is specifically designed for loans that use personal property as collateral and differs from other promissory notes by requiring a separate security agreement. This form ensures both parties understand the terms of the loan, including payment schedules and interest rates.

What’s included in this form

- Borrower's promise to pay the principal amount plus interest.

- Details on the interest rate and payment schedule.

- Terms regarding late payments and potential penalties.

- Borrower's rights for early repayment.

- Conditions under which the lender can declare a default.

When to use this form

This form is suitable when an individual or entity borrows money and secures it with personal property, such as a vehicle or equipment. It is commonly used in small business loans or personal loans where traditional financing options may not be available. If you need a structured repayment plan while using your property as collateral, this form is appropriate.

Intended users of this form

- Individuals seeking a loan secured by personal property.

- Small business owners needing financing for operations or equipment.

- Lenders who require a formalized agreement to secure their investment.

- Borrowers who prefer a clear repayment structure and terms.

Instructions for completing this form

- Identify the parties involved, including the borrower and lender names and addresses.

- Specify the loan amount (principal) and interest rate.

- Outline the payment schedule, including the due date and amount of each payment.

- State the terms regarding late payments and prepayments, if applicable.

- Have all parties sign and date the document to make it legally binding.

Does this document require notarization?

This form does not typically require notarization unless specified by local law. However, always verify local regulations to ensure compliance, as some lenders may request notarization for added security.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Mistakes to watch out for

- Failing to clearly specify the loan amount, which can lead to disputes.

- Not outlining the payment schedule or interest rate accurately.

- Overlooking late payment penalties, leading to unexpected charges.

- Not obtaining necessary signatures, which invalidates the agreement.

Advantages of online completion

- Convenience: Easily fill out and download the form from anywhere.

- Editability: Customize the form to fit your specific loan terms.

- Reliability: Access templates created by licensed attorneys to ensure compliance with legal standards.

Legal use & context

- Provides a legally enforceable promise to repay the loan under specified terms.

- Secures the loan with personal property, reducing risk for the lender.

- Ensures both parties are clear on rights, obligations, and penalties regarding defaults.

Quick recap

- The Louisiana Installments Fixed Rate Promissory Note secures loans with personal property.

- It helps outline clear repayment terms to protect both borrowers and lenders.

- Understanding your rights and obligations under this form is essential for all parties involved.

Legal terms and meanings

- Principal: The original sum of money borrowed or the amount remaining unpaid.

- Collateral: An asset pledged by a borrower to secure a loan.

- Default: The failure to repay the loan amount or make scheduled payments on time.

- Interest: The cost of borrowing money, expressed as a percentage of the principal.

Looking for another form?

Form popularity

FAQ

You can use a template or create a promissory note online. But before you begin, you'll need to gather some information and make decisions about the way the loan will be structured. First, you'll need the names and addresses of both the lender (or "payee") and the borrower.

To write a promissory note for a personal loan, you will need to include the names of both parties, the principal balance, the APR, and any fees that are part of the agreement. The promissory note should also clearly explain what will happen if the borrower pays late or does not pay the loan back at all.

Navigate to the website: www.studentloans.gov. Click "Log In." Enter your FSA ID and Password. Click "Complete Master Promissory Note." Select the appropriate loan type. Enter Your Personal Information.

Promissory notes are ideal for individuals who do not qualify for traditional mortgages because they allow them to purchase a home by using the seller as the source of the loan and the purchased home as the source of the collateral.

"A promissory note is enforceable through an ordinary breach of contract claim." In other words, it's not required that the loan be secured; an unsecured loan is still enforceable as long as the promissory note is fully completed. Lender and borrower information.

Types of Property that can be used as collateral. Speak to them in person. Draft a Demand / Notice Letter. Write and send a Follow Up Letter. Enlisting a Professional Collection Agency. Filing a petition or complaint in court. Selling the Promissory Note. Final Tips.

Write the date of the writing of the promissory note at the top of the page. Write the amount of the note. Describe the note terms. Write the interest rate. State if the note is secured or unsecured. Include the names of both the lender and the borrower on the note, indicating which person is which.

Unlike a mortgage or deed of trust, the promissory note isn't recorded in the county land records. The lender holds the promissory note while the loan is outstanding. When the loan is paid off, the note is marked as "paid in full" and returned to the borrower.

To secure a promissory note means that you identify some specific property and attach it to the note. Then, if the borrower defaults on the loan, you will be able to repossess the collateral as compensation for the loan.