Kentucky Challenge to Credit Report of Experian, TransUnion, and/or Equifax

Description

How to fill out Challenge To Credit Report Of Experian, TransUnion, And/or Equifax?

Are you presently inside a position the place you will need documents for possibly enterprise or person uses nearly every day? There are a variety of legitimate record layouts available on the net, but discovering versions you can depend on isn`t effortless. US Legal Forms provides a large number of form layouts, much like the Kentucky Challenge to Credit Report of Experian, TransUnion, and/or Equifax, that are written to fulfill federal and state specifications.

If you are previously acquainted with US Legal Forms web site and have your account, basically log in. After that, you can obtain the Kentucky Challenge to Credit Report of Experian, TransUnion, and/or Equifax design.

Should you not provide an accounts and wish to begin to use US Legal Forms, abide by these steps:

- Find the form you want and make sure it is for your right area/region.

- Use the Preview option to review the shape.

- Read the information to actually have selected the right form.

- In the event the form isn`t what you are looking for, take advantage of the Search area to find the form that meets your needs and specifications.

- If you obtain the right form, click Buy now.

- Select the rates program you need, fill in the necessary information and facts to make your account, and purchase your order making use of your PayPal or bank card.

- Pick a convenient paper structure and obtain your backup.

Find every one of the record layouts you may have bought in the My Forms menus. You can get a further backup of Kentucky Challenge to Credit Report of Experian, TransUnion, and/or Equifax any time, if necessary. Just click the necessary form to obtain or produce the record design.

Use US Legal Forms, the most substantial assortment of legitimate varieties, to save time as well as steer clear of faults. The assistance provides expertly produced legitimate record layouts which you can use for a selection of uses. Create your account on US Legal Forms and begin generating your daily life easier.

Form popularity

FAQ

The law was passed in 1970 and amended twice. It is primarily aimed at the three major credit reporting agencies ? Experian, Equifax and TransUnion ? because of the widespread use of the information those bureaus collect and sell.

To freeze your credit, you have to contact each of the three credit bureaus individually. Placing a credit freeze is free for you and your children, as is lifting it when applying for new credit.

In general, under the Fair Credit Reporting Act, furnishers who furnish information about consumers to consumer reporting agencies must: Provide complete and accurate information to the credit reporting agencies. Investigate consumer disputes received from credit reporting agencies.

The FCRA ensures the information in your credit report is accurate and up to date, and that no one accesses your credit report without having a legitimate reason for doing so, called a ?permissible purpose,? as listed in 15 U.S.C. 1681b.

Information is being gathered about consumers all the time: In addition to the three major consumer credit bureaus (Experian, TransUnion and Equifax), there are other organizations that may collect and use your information.

An Equifax credit score isn't used by lenders or creditors to assess a consumers' creditworthiness. Instead, many lenders use FICO Scores® to help determine a potential borrower's creditworthiness. FICO uses credit scores from the three reporting agencies, including Equifax and Transunion, to determine their score.

Which entities are not subject to regulations under the FCRA? A background-screening company is sometimes hired by a company where you are applying for a job. While these companies are able to look at various aspects of your life, including financial transactions, they are not entirely bound by all FCRA regulations.

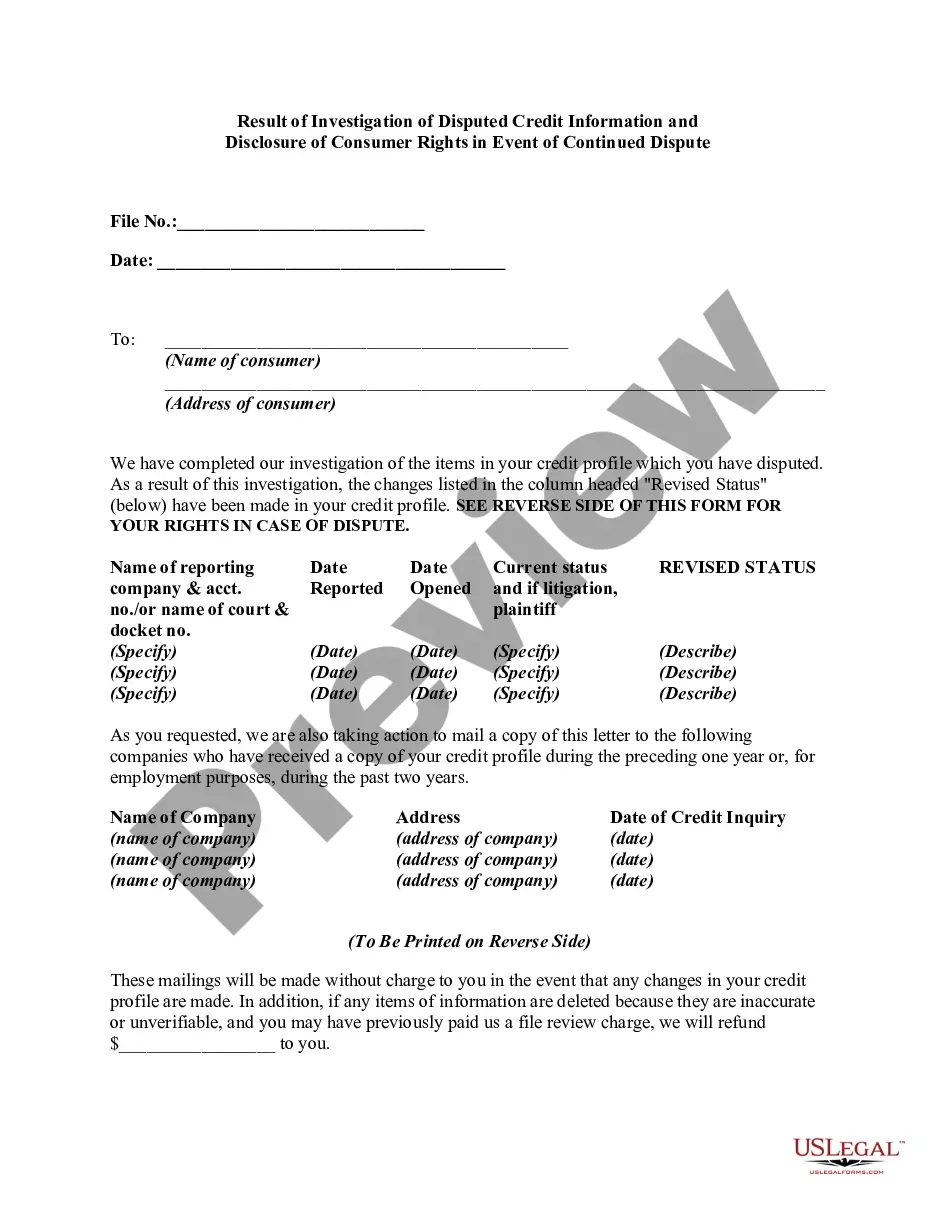

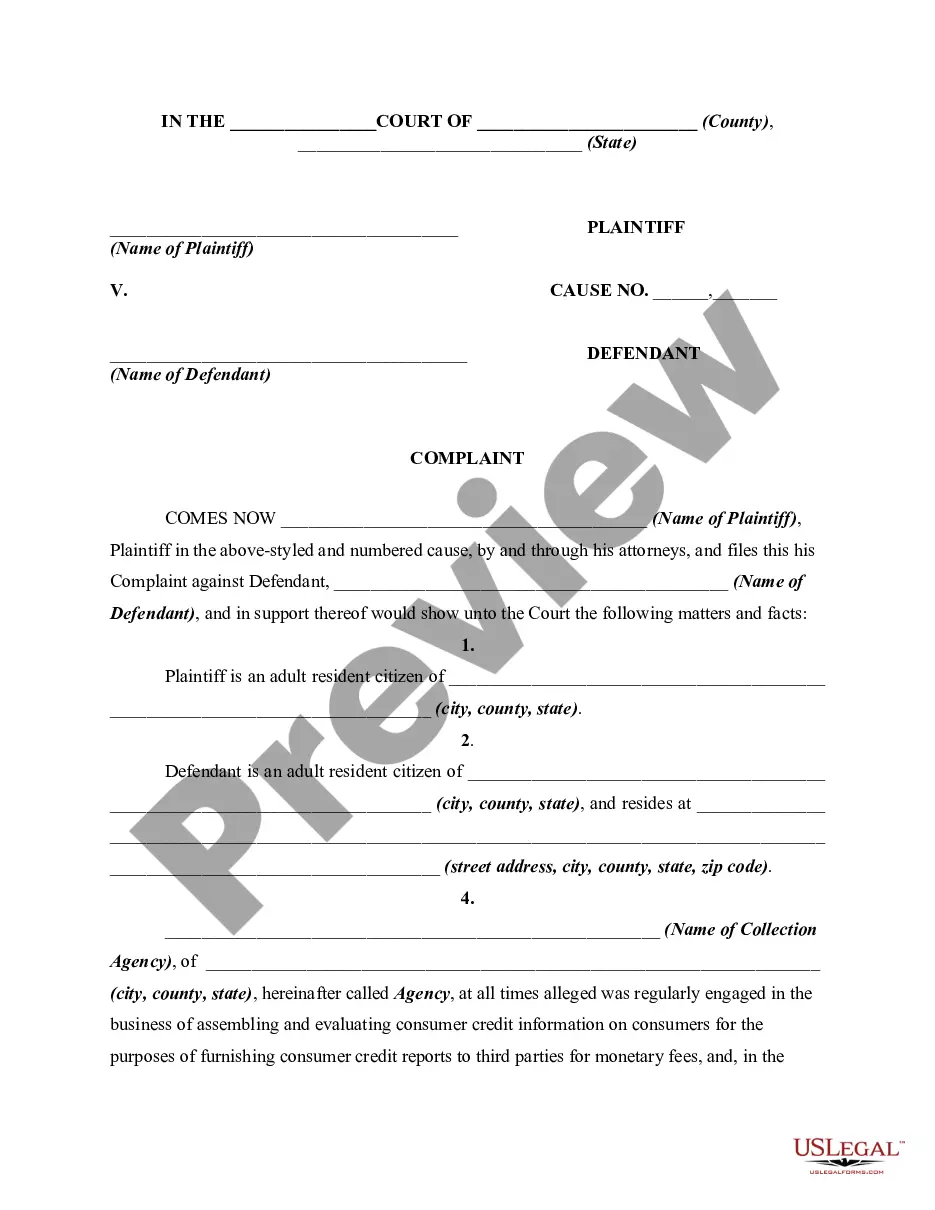

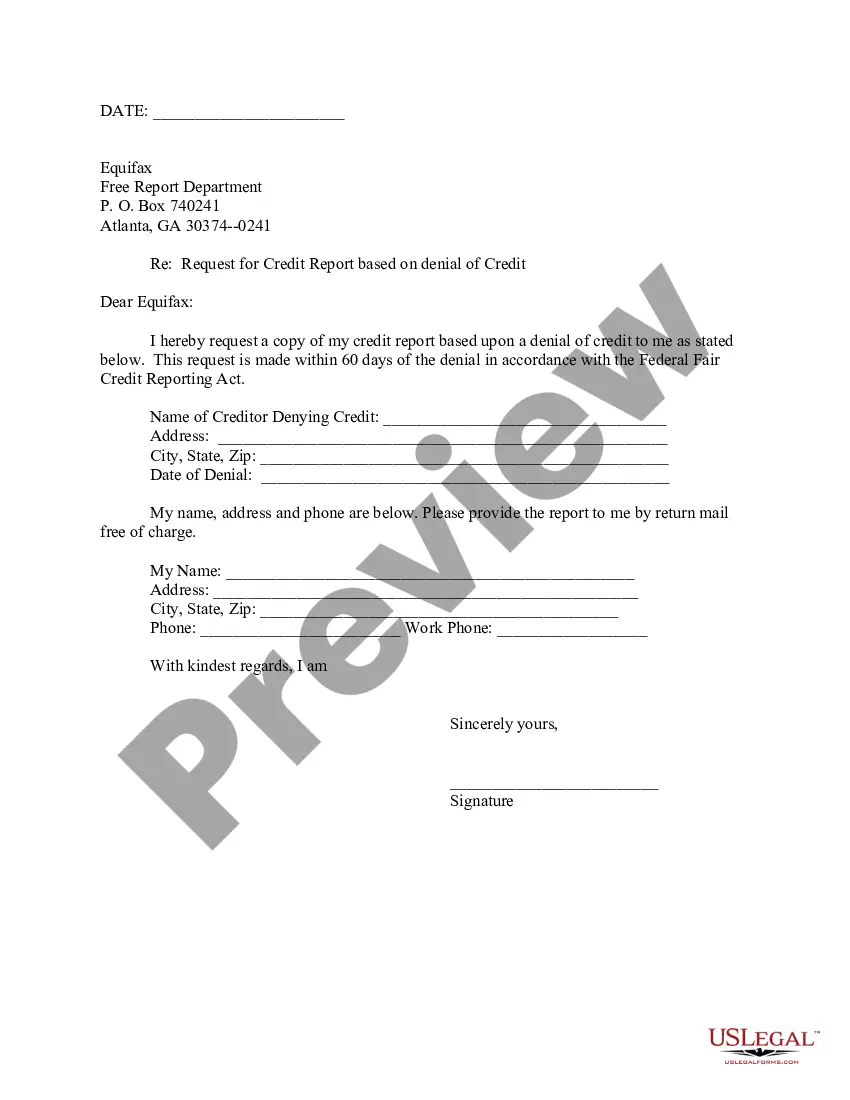

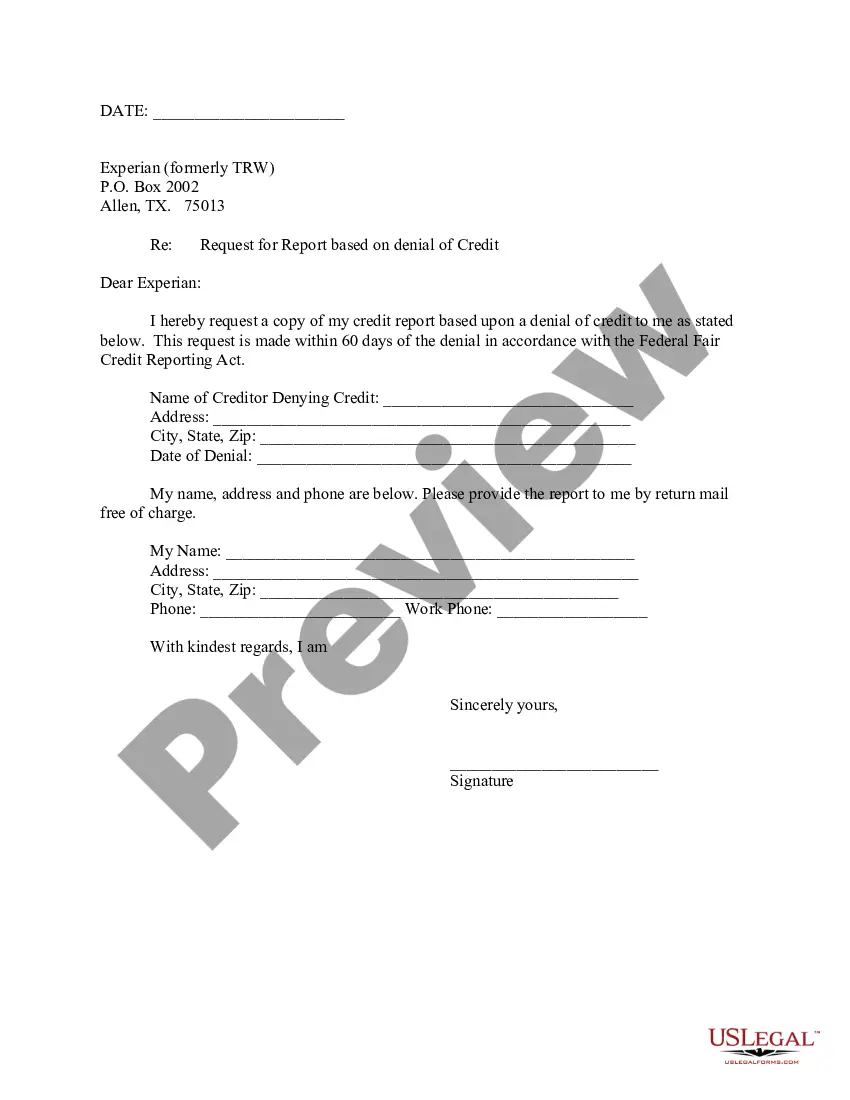

If you identify an error on your credit report, you should start by disputing that information with the credit reporting company (Experian, Equifax, and/or Transunion). You should explain in writing what you think is wrong, why, and include copies of documents that support your dispute.

Common violations of the FCRA include: Failure to update reports after completion of bankruptcy is just one example. Agencies might also report old debts as new and report a financial account as active when it was closed by the consumer. Creditors give reporting agencies inaccurate financial information about you.

The Act (Title VI of the Consumer Credit Protection Act) protects information collected by consumer reporting agencies such as credit bureaus, medical information companies and tenant screening services. Information in a consumer report cannot be provided to anyone who does not have a purpose specified in the Act.