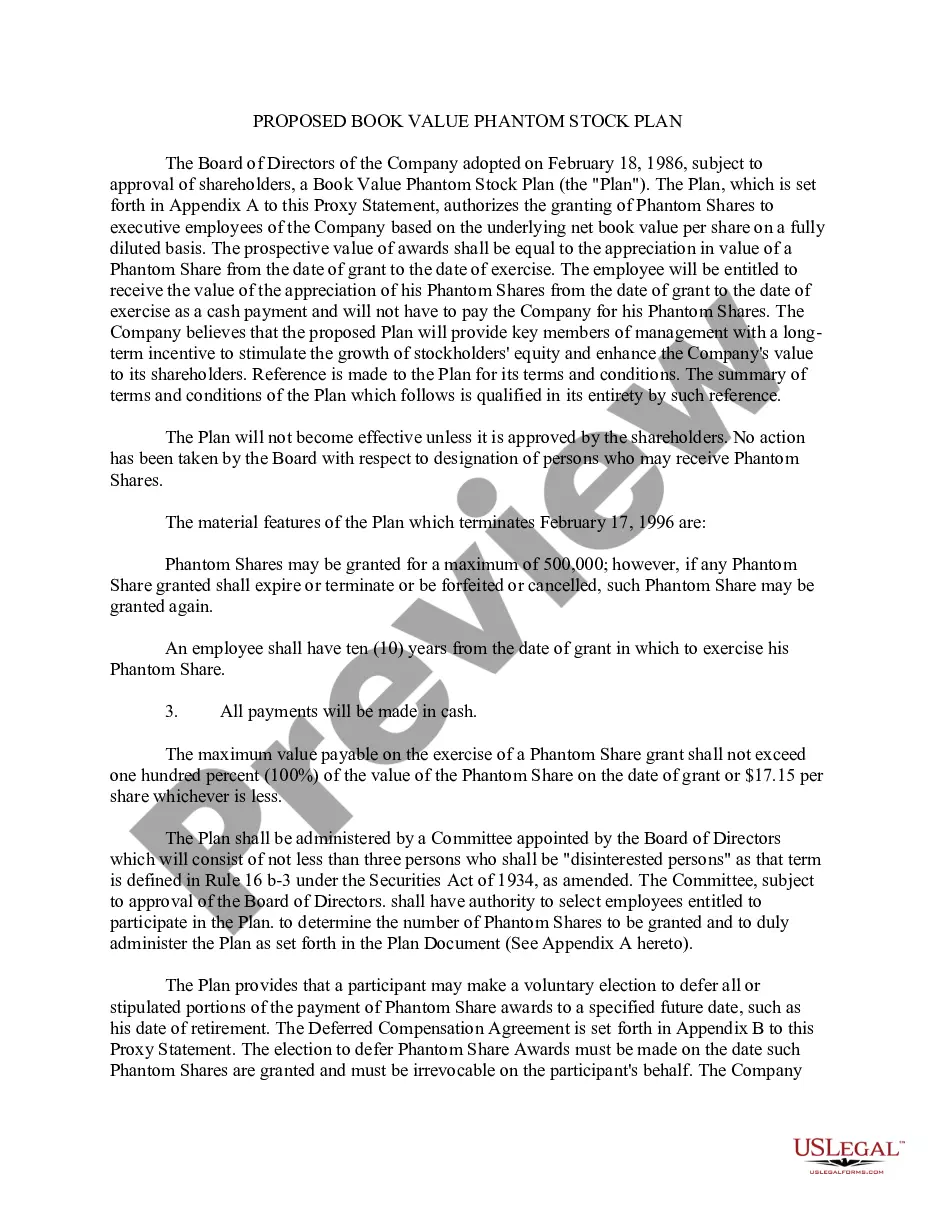

20-162A 20-162A . . . Book Value Phantom Stock Plan under which Committee of Board of Directors may, from time to time, grant quantity of phantom shares to selected employees, each share being equivalent to one share of corporation common stock. Phantom shares may be exercised at any time within ten years of date of grant (subject to certain limitations in event of termination of employment) Upon exercise, employee is paid cash equal to increase in underlying net book value per share on fully diluted basis of shares between date of grant and date of exercise

Kansas Book Value Phantom Stock Plan of First Florida Banks, Inc.

State:

Multi-State

Control #:

US-CC-20-162A

Format:

Word;

Rich Text

Instant download

Description

Free preview

How to fill out Book Value Phantom Stock Plan Of First Florida Banks, Inc.?

US Legal Forms - one of many biggest libraries of lawful types in the United States - provides an array of lawful document layouts you are able to acquire or printing. While using site, you may get a large number of types for organization and person purposes, categorized by types, claims, or keywords and phrases.You will discover the most recent types of types just like the Kansas Book Value Phantom Stock Plan of First Florida Banks, Inc. in seconds.

If you already possess a membership, log in and acquire Kansas Book Value Phantom Stock Plan of First Florida Banks, Inc. from your US Legal Forms catalogue. The Acquire button can look on every kind you see. You have accessibility to all formerly delivered electronically types from the My Forms tab of your profile.

If you would like use US Legal Forms initially, allow me to share simple directions to help you began:

- Be sure you have selected the correct kind to your city/county. Select the Review button to check the form`s content. See the kind outline to actually have chosen the correct kind.

- When the kind does not suit your specifications, utilize the Look for industry near the top of the monitor to discover the one which does.

- Should you be pleased with the shape, verify your decision by clicking the Buy now button. Then, select the costs strategy you favor and provide your qualifications to sign up for an profile.

- Procedure the transaction. Use your credit card or PayPal profile to finish the transaction.

- Choose the structure and acquire the shape on your device.

- Make adjustments. Load, modify and printing and sign the delivered electronically Kansas Book Value Phantom Stock Plan of First Florida Banks, Inc..

Every template you added to your money does not have an expiration date and is also yours forever. So, if you wish to acquire or printing yet another version, just visit the My Forms segment and click around the kind you need.

Gain access to the Kansas Book Value Phantom Stock Plan of First Florida Banks, Inc. with US Legal Forms, by far the most comprehensive catalogue of lawful document layouts. Use a large number of specialist and state-particular layouts that meet up with your small business or person needs and specifications.

Form popularity

FAQ

A cash payment from Company A as the difference between the current common share price and phantom stock issue price: ($70 ? $50) x 500 = $10,000; or. A cash payment from Company A equal to the current common share price: $50 x 500 = $25,000.

Phantom shares are usually paid out when the company gets acquired or IPOes. The phantom shares are paid out in cash for their corresponding value.

Payments from phantom stock plans are subject to typical income taxes, not capital gains taxes. In turn, companies can deduct phantom plan payouts the year the employee reports the income. Employers must ensure their plans follow federal laws in section 409A of the Internal Revenue Code (IRC).

The answer involves two variables: (a) the presumed value of the company, and (b) the number of shares to be used in the plan. Once these two answers are known, the phantom share price is calculated as the former (the value) divided by the latter (the number of shares).

The answer involves two variables: (a) the presumed value of the company, and (b) the number of shares to be used in the plan. Once these two answers are known, the phantom share price is calculated as the former (the value) divided by the latter (the number of shares).

The plan may provide for a single payment, or it may provide for installment payments over a period of time after the phantom stock vests. In some cases, the employer may let the employee elect to receive the payout in the form of an equivalent amount of stock.

Phantom stock plans are considered ?liability awards? for accounting purposes (assuming they will be settled in cash rather than stock). As such, the sponsoring company must recognize the plan expense ratably over the vesting period. Varying accrual schedules can be found in the market.

Phantom shares are only paid out if the employee meets certain terms. If an employee leaves the company before those terms are met, the phantom stocks disappear. If the company had used actual stock, those would have to be repurchased, which would make things more complicated and potentially, more expensive.