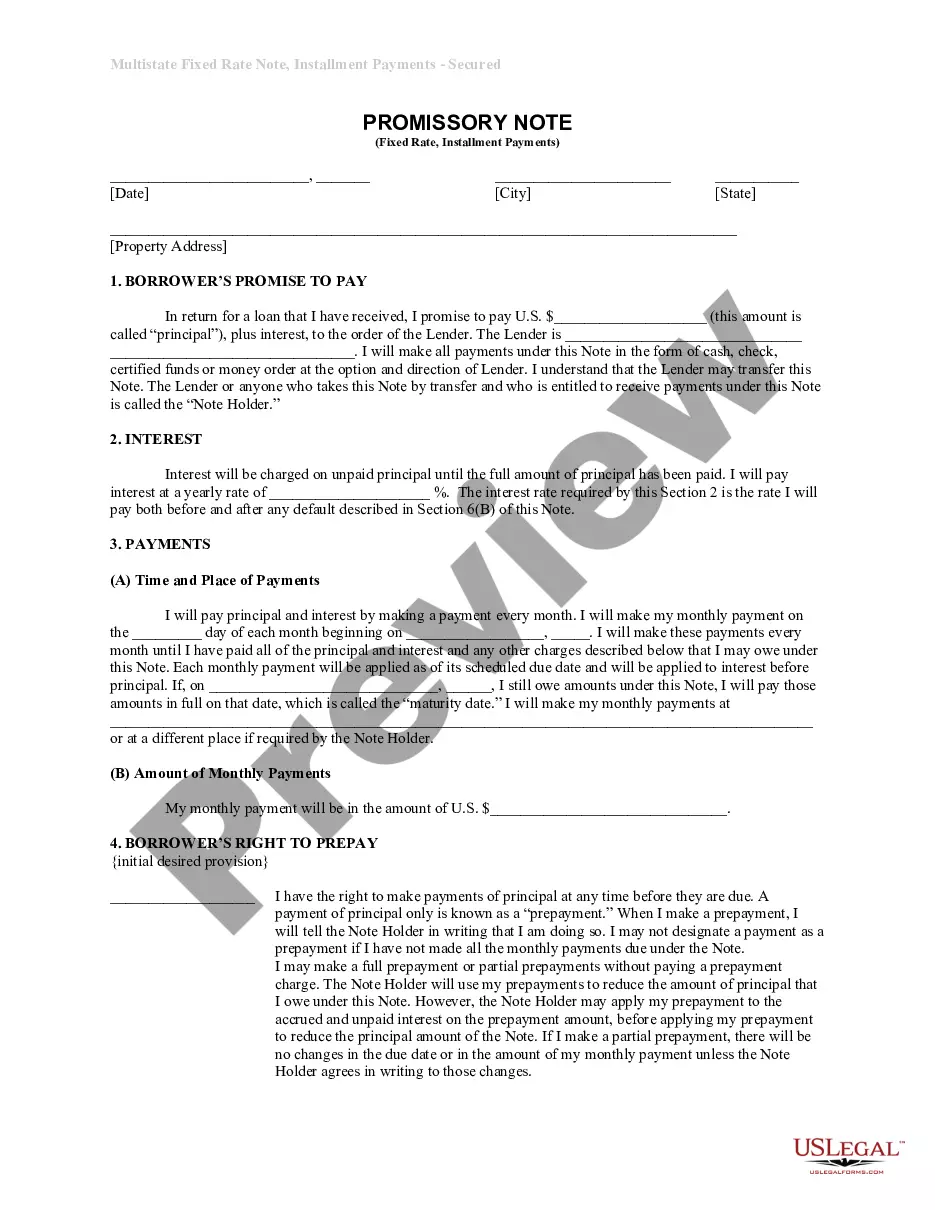

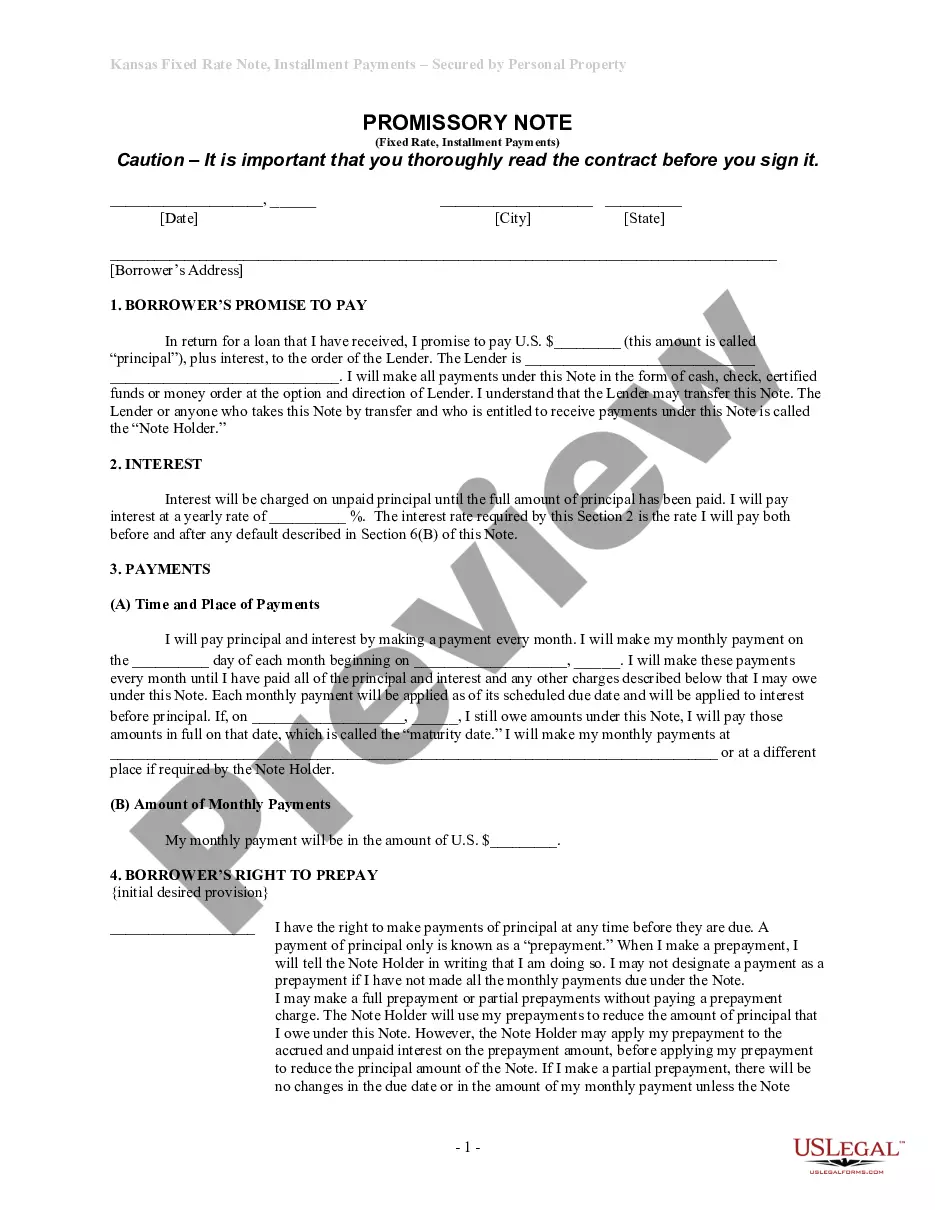

Kansas Unsecured Installment Payment Promissory Note for Fixed Rate

About this form

The Kansas Unsecured Installment Payment Promissory Note for Fixed Rate is a legal document that outlines a borrower's promise to repay a loan in regular installments. Unlike secured notes, this promissory note is unsecured, meaning it does not require collateral. It features a fixed interest rate and specifies the terms of repayment, making it a reliable option for personal loans or informal agreements between individuals.

Key components of this form

- Borrower's promise to pay back the principal and interest to the lender.

- Details of the interest rate and how it applies to unpaid principal.

- Schedule and amount of monthly payments.

- Borrower's right to prepay the loan, including any applicable penalties.

- Consequences of late payments and default.

- Procedure for delivering notices between the borrower and lender.

Situations where this form applies

This form is typically used when an individual or entity borrows money from another individual or entity without providing collateral. It is ideal for personal loans, financial agreements between friends or family, or any situation where an unsecured loan is appropriate. You should consider using this document to clarify repayment terms and to protect the interests of both parties involved in the loan.

Who this form is for

Individuals who should consider using this form include:

- Borrowers seeking an unsecured personal loan.

- Lenders who want a clear repayment agreement with fixed terms.

- Parties involved in informal lending transactions.

- Anyone looking to document a loan for personal records or legal purposes.

How to prepare this document

- Provide the date and the location (city and state) of the agreement.

- Enter details about the borrower(s) and their address.

- Specify the principal amount being borrowed and the annual interest rate.

- Fill in the monthly payment amount and schedule starting date.

- Review and sign the document to ensure all parties are acknowledged.

Does this form need to be notarized?

This form does not typically require notarization to be legally valid. However, some jurisdictions or document types may still require it. US Legal Forms provides secure online notarization powered by Notarize, available 24/7 for added convenience.

Get your form ready online

Our built-in tools help you complete, sign, share, and store your documents in one place.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Make edits, fill in missing information, and update formatting in US Legal Forms—just like you would in MS Word.

Download a copy, print it, send it by email, or mail it via USPS—whatever works best for your next step.

Sign and collect signatures with our SignNow integration. Send to multiple recipients, set reminders, and more. Go Premium to unlock E-Sign.

If this form requires notarization, complete it online through a secure video call—no need to meet a notary in person or wait for an appointment.

We protect your documents and personal data by following strict security and privacy standards.

Typical mistakes to avoid

- Failing to include the correct interest rate or payment schedule.

- Not providing a clear definition of late payment penalties.

- Omitting the borrower's right to prepay the loan and any conditions attached.

- Neglecting to sign the document by all involved parties.

Advantages of online completion

- Convenient access to a legally vetted form that can be downloaded and filled out at home.

- Editability allows users to customize terms according to their specific agreement.

- Reliable documentation for both the lender and borrower to avoid misunderstandings.

Quick recap

- This form serves as a legally binding agreement between a borrower and lender.

- Clear terms of repayment help prevent future disputes.

- Understanding borrower rights, including prepayment options and default consequences, is essential.

- Always ensure that all parties review and sign the document for it to be effective.

Looking for another form?

Form popularity

FAQ

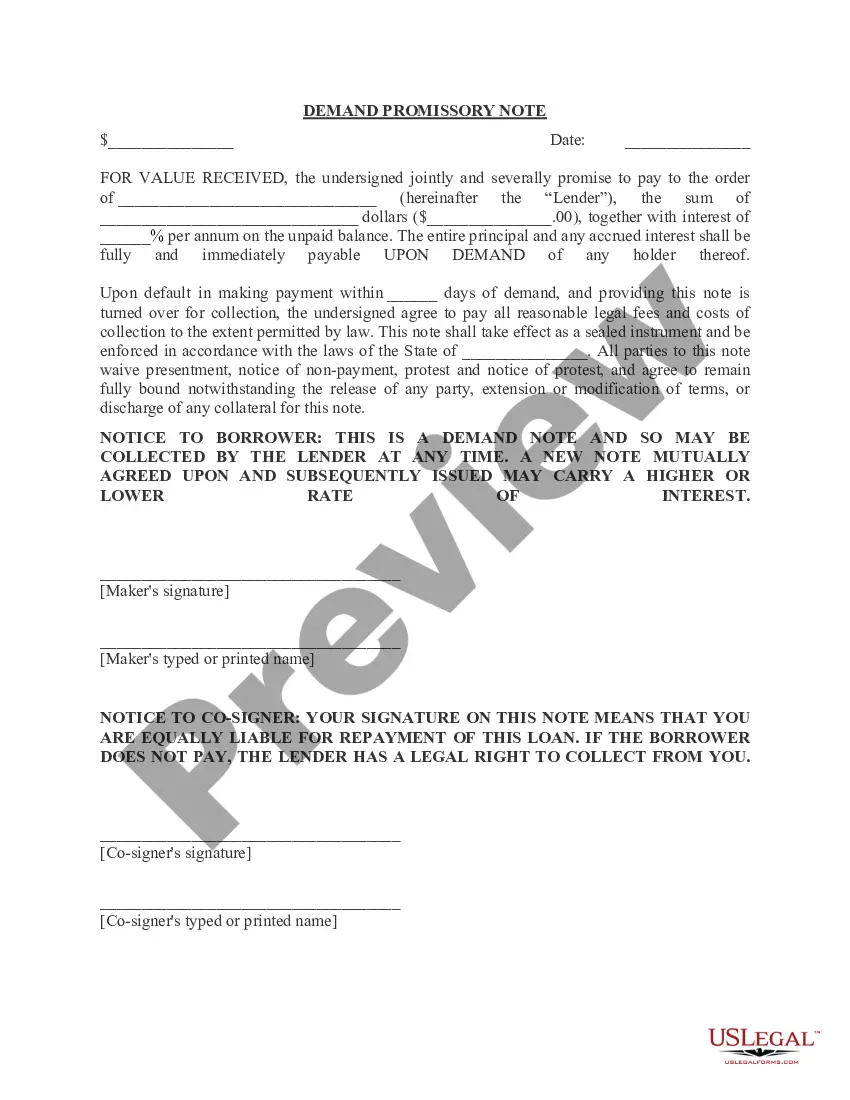

Writing the Promissory Note Terms You don't have to write a promissory note from scratch. You can use a template or create a promissory note online.

A simple promissory note might be for a lump sum repayment on a certain date. For example, you lend your friend $1,000 and he agrees to repay you by December 1. The full amount is due on that date, and there is no payment schedule involved.

Secured or unsecured? Generally, promissory notes are unsecured which means it is more like a formal IOU. However, lenders can request some security for the loan. For personal secured promissory notes, a house or car is often used as collateral.

Write the date of the writing of the promissory note at the top of the page. Write the amount of the note. Describe the note terms. Write the interest rate. State if the note is secured or unsecured. Include the names of both the lender and the borrower on the note, indicating which person is which.

Unsecured Promissory Notes An unsecured promissory note is an obligation for payment without any property securing the payment.A short-term unsecured promissory note is the type most often used when a relatively small amount of money is borrowed from a friend or relative.

Navigate to the website: www.studentloans.gov. Click "Log In." Enter your FSA ID and Password. Click "Complete Master Promissory Note." Select the appropriate loan type. Enter Your Personal Information.

In order for a promissory note to be valid, both the lender and the borrower must sign the documentation. If you are a co-signer for the loan, you are required to sign the promissory note. Being a co-signer requires you to repay the loan amount in the instance that the borrower defaults on payment.

Use our promissory note if you prefer a standard basic contract. Do I have to charge the Borrower interest? No, the Lender can choose whether or not to charge interest.However, there may be tax consequences to the Lender or Borrower if interest is charged but it is not a reasonable rate.

A promissory note basically includes the name of both parties (lender and borrower), date of the loan, the amount, the date the loan will be repaid in full, frequency of loan payments, the interest rate charged on the loan payments, and any security agreement.