Indiana Proposal to adopt plan of dissolution and liquidation

Description

How to fill out Proposal To Adopt Plan Of Dissolution And Liquidation?

US Legal Forms - among the greatest libraries of lawful forms in the United States - delivers an array of lawful document themes you may down load or print. Using the site, you can find thousands of forms for enterprise and individual uses, sorted by groups, suggests, or keywords.You will find the most recent variations of forms much like the Indiana Proposal to adopt plan of dissolution and liquidation in seconds.

If you already possess a subscription, log in and down load Indiana Proposal to adopt plan of dissolution and liquidation from your US Legal Forms local library. The Acquire switch will show up on each and every form you see. You have accessibility to all previously acquired forms within the My Forms tab of the account.

If you would like use US Legal Forms initially, listed below are basic instructions to help you began:

- Be sure you have picked out the right form to your area/area. Click the Review switch to check the form`s articles. See the form explanation to ensure that you have selected the appropriate form.

- If the form doesn`t match your specifications, utilize the Research discipline on top of the monitor to discover the one which does.

- When you are happy with the shape, verify your option by visiting the Purchase now switch. Then, opt for the pricing strategy you like and give your references to sign up on an account.

- Approach the purchase. Make use of charge card or PayPal account to finish the purchase.

- Select the format and down load the shape on your product.

- Make adjustments. Load, revise and print and sign the acquired Indiana Proposal to adopt plan of dissolution and liquidation.

Each web template you added to your bank account does not have an expiry particular date and is your own property forever. So, if you want to down load or print an additional version, just check out the My Forms portion and click on around the form you want.

Gain access to the Indiana Proposal to adopt plan of dissolution and liquidation with US Legal Forms, probably the most extensive local library of lawful document themes. Use thousands of professional and express-certain themes that fulfill your organization or individual requires and specifications.

Form popularity

FAQ

Once a company is dissolved, it no longer exists as a legal entity and cannot conduct business or enter into contracts. Dissolution may also trigger a number of certain legal obligations, such as the distribution of remaining assets to creditors or shareholders. It also might involve the filing of final tax returns.

Dissolution doesn't always end up with liquidation. It is based on their capital balances. The final distribution of cash to the partners shall be made based on their profit and loss sharing agreement.

Dissolution, or the process of dissolving a company, will occur after a liquidation as the business must be struck off the Companies House register. This can only happen once the assets have been sold and distributed amongst creditors and shareholders.

Foreign Entity Registration in Indiana; Failure to Register.

What are the differences between liquidation and dissolution? Dissolving a company through the process of dissolution often takes place when a company is solvent, but is no longer trading. Liquidation however, occurs due to a company having financial difficulties and therefore being unable to keep up with their debts.

To dissolve an Indiana Corporation that has not yet conducted business, file Form 39035, Articles of Dissolution Prior to Issuing Shares or Commencing Business. Submit one original and one copy to the SOS by mail, express mail, or in person.

Dissolving a company is a formal way of closing it. Dissolution refers to the process of 'striking off' (removing) a company from the Companies House register. It can be the most straightforward way of shutting a company down once its directors have decided it should no longer trade.

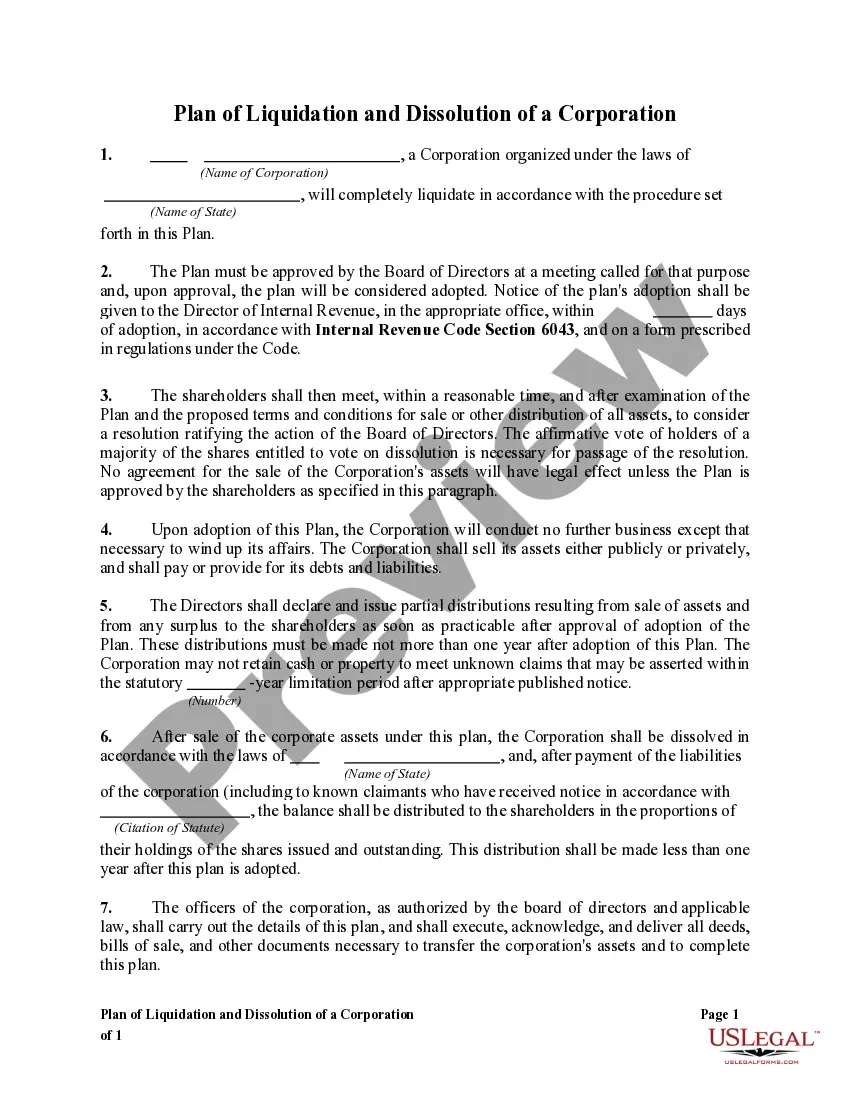

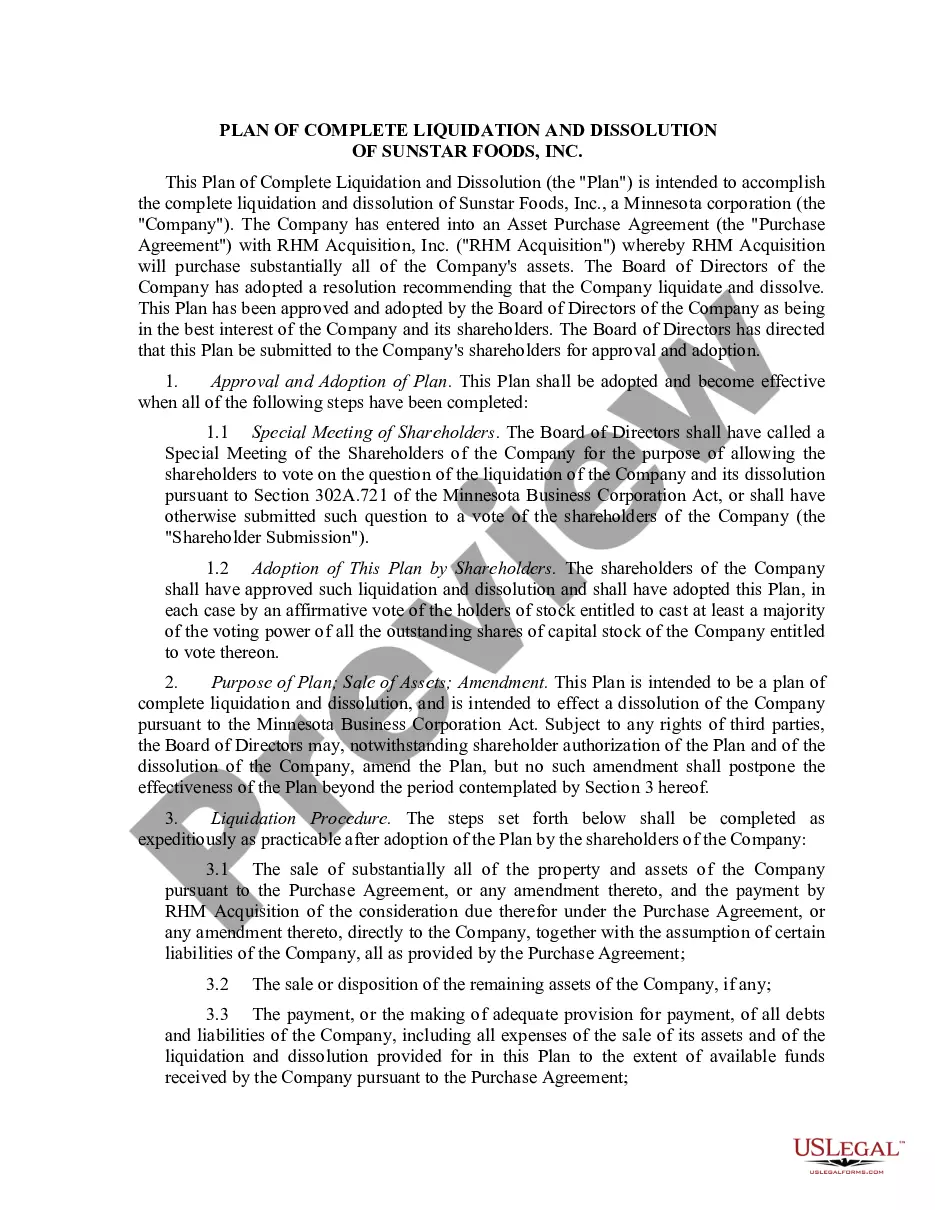

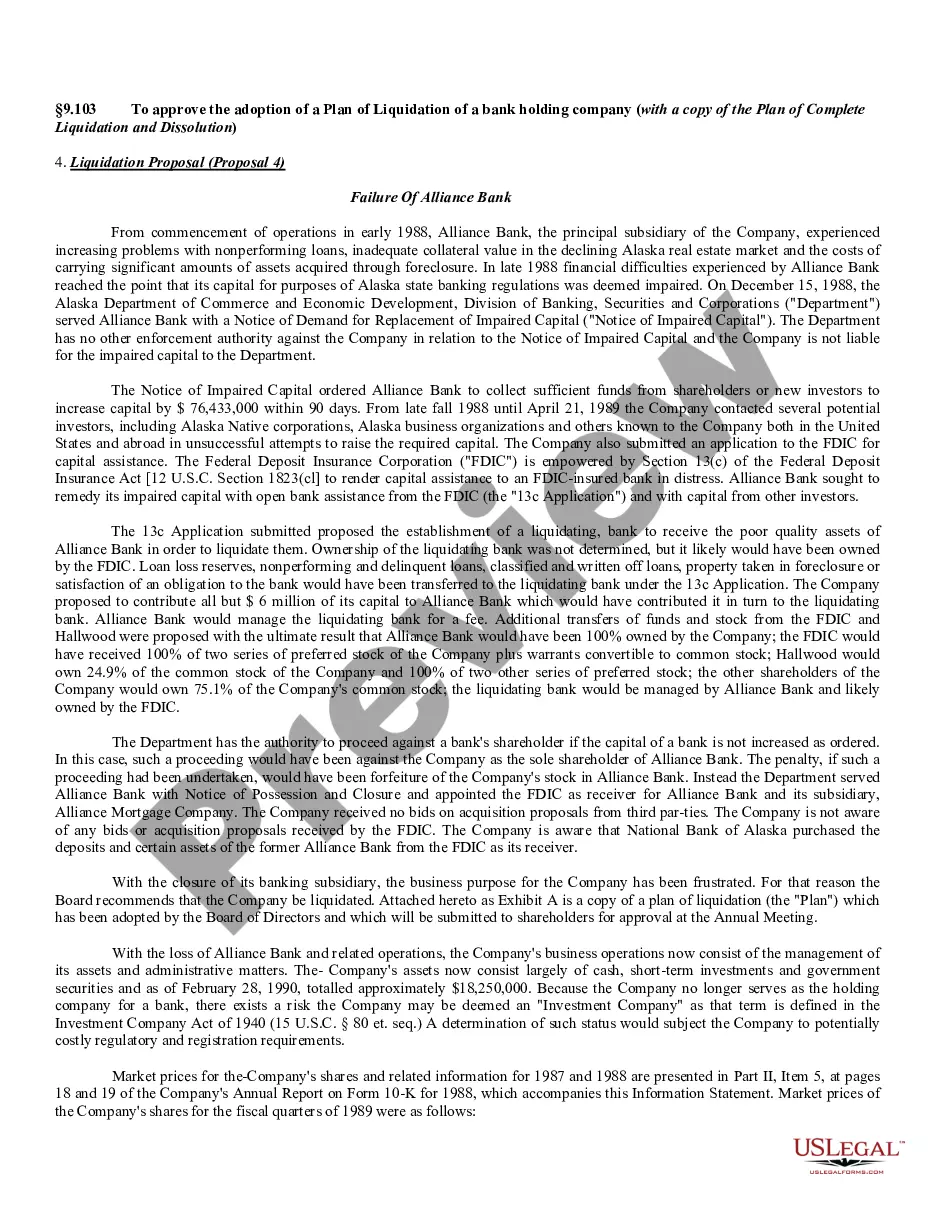

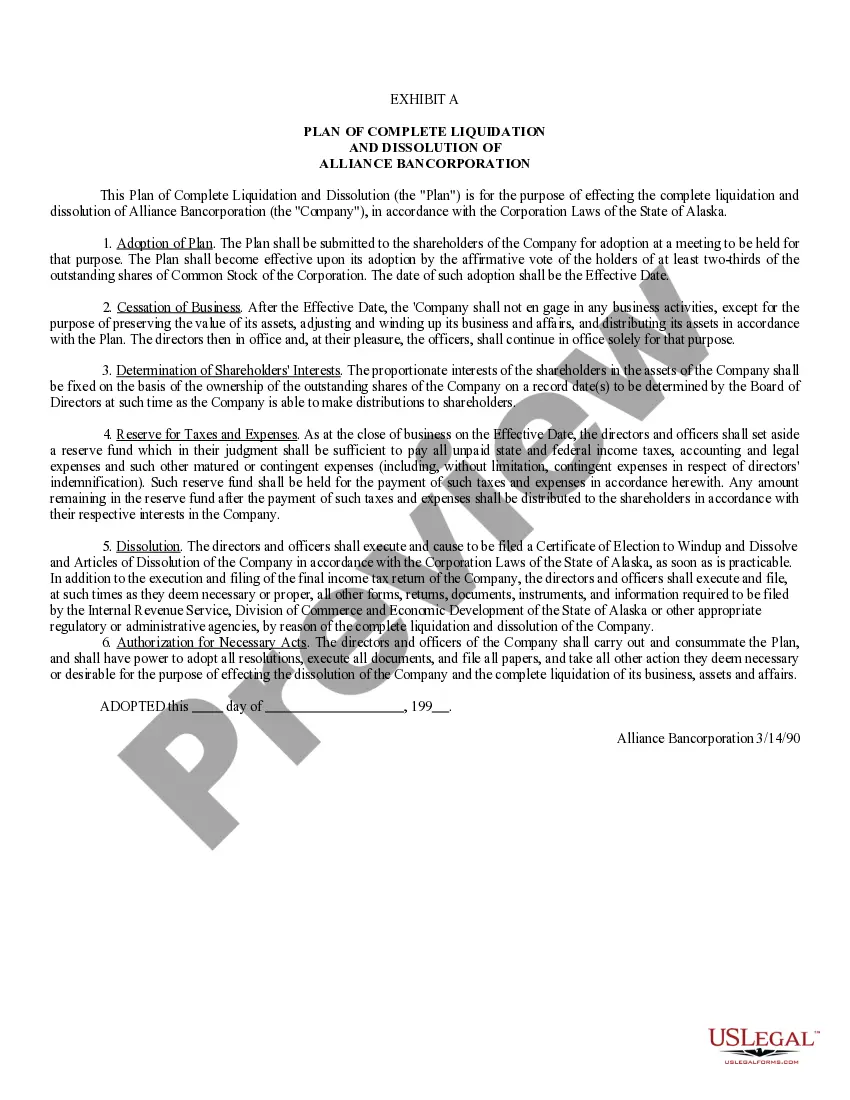

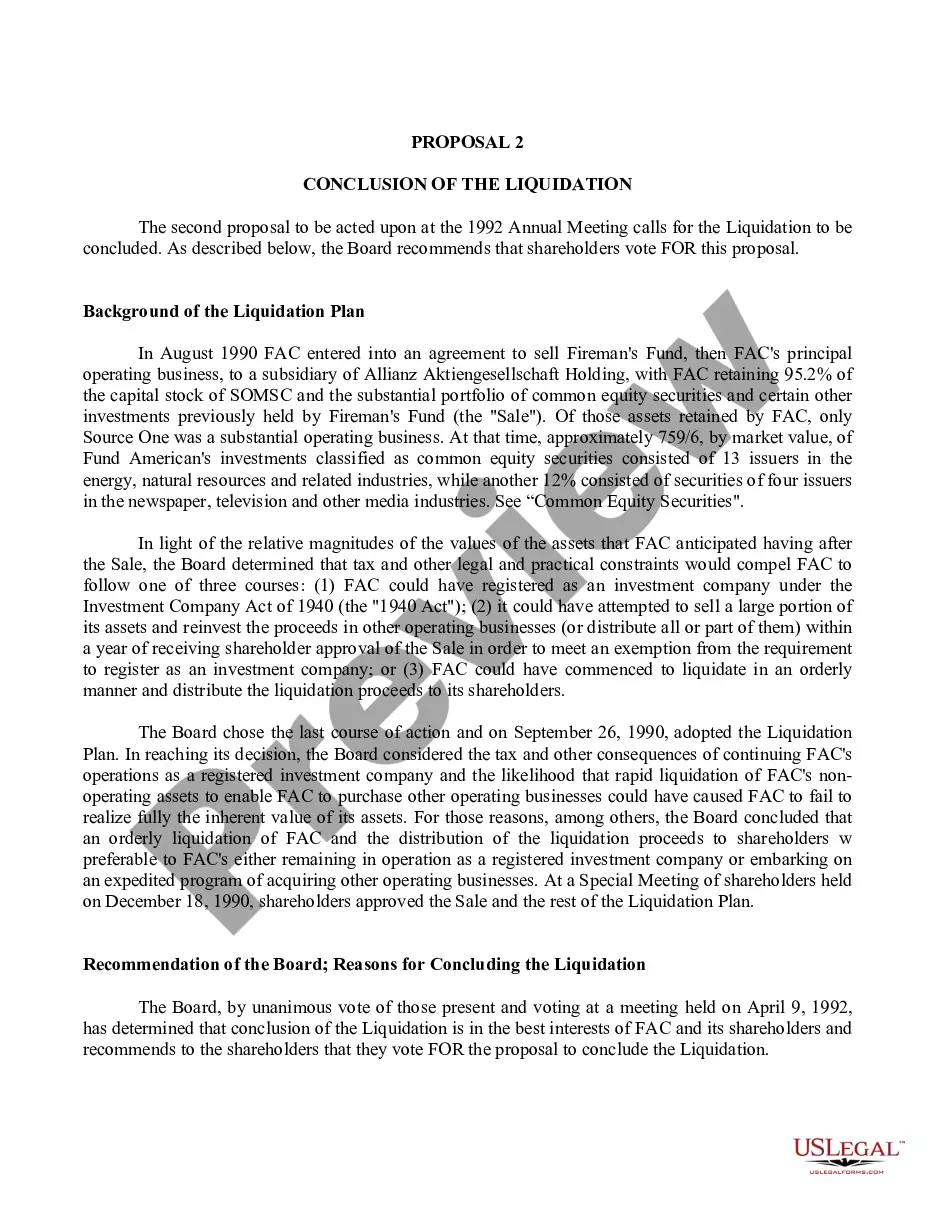

A plan of dissolution is a written description of how an entity intends to dissolve, or officially and formally close the business. A plan of dissolution will include a description of how any remaining assets and liabilities will be distributed.